5 Fastest Growing Ecommerce Companies in 2026

Americans now spend more on e-commerce than the GDP of Denmark and these 5 innovative companies are cashing in. Forget Amazon clones. These disruptors are creating entirely new ways to shop. 1. Whatnot – Livestream Shopping Marketplace Imagine scrolling through TikTok, but instead of just watching, you can instantly buy what you see. That is Whatnot. This platform brings the thrill of live auctions to your phone, where sellers host real-time video streams to showcase everything from rare Pokémon cards to sneakers, vintage toys, and luxury handbags. Unlike traditional marketplaces like eBay or Facebook Marketplace, Whatnot makes shopping entertaining. Sellers hype up their products like game show hosts, buyers chat and bid in real time, and rare items can sell for thousands in minutes. It is QVC meets social media and it is no longer just for collectors. Think about that for a second. The average Whatnot user spends 95 minutes per day on the app. That is more than YouTube. More than TikTok. When people stay that long, they buy things. In October 2025, Whatnot raised $225 million in a Series F round, more than doubling its valuation from $5 billion at the start of the year to $11.5 billion by the end of it. Platform GMV hit $8 billion for the full year, up from $3 billion in 2024. Revenue reached an estimated $1 billion. The company ranked as the number one Shopping app in both the U.S. and U.K. App Stores, and generated over $100 million in live sales on Black Friday 2025 alone. The platform is also expanding fast into new categories. Beauty grew 791% year-over-year. Electronics grew 444%. Women’s fashion grew 223%. This is no longer a niche collectibles site; it is becoming a mainstream shopping destination built around entertainment. Key Figures: Why it works: Live auctions create urgency that static product pages simply cannot replicate. When you can see a seller’s face, hear the excitement in the room, and watch a countdown timer, buying feels different. That psychology drives conversion rates that traditional ecommerce can only dream about. 2. ShopMy – Creator-Affiliate Commerce Platform Ever click an Instagram link to buy a product? There is a good chance ShopMy powered it. This platform helps influencers monetise their audiences by turning their posts into shoppable storefronts. Brands like Nike, Lululemon, Gucci, and Sephora use ShopMy to track which creators actually drive sales, not just likes. Meanwhile, creators get a commission on every purchase without needing a clunky Shopify store. It is a clean arrangement: brands pay for performance, creators get rewarded for taste, and shoppers discover products through people they actually trust. What makes ShopMy different from older affiliate platforms is the quality filter. This is not a platform for any influencer with a discount code. It is built around vetted tastemakers, which keeps the product recommendations credible and the conversion rates high. Brands on the premium end of the market, the ones that would run a mile from a generic influencer campaign, are lining up to use it. As affiliate revenue scales, creators must treat this income like a true business. If you are monetising your audience, our guide to tax deductions for independent professionals can help you protect those earnings. ShopMy raised $70 million in a Series C round in October 2025 at a $1.5 billion valuation, officially becoming a unicorn five years after founding. Revenue grew 200% year-over-year to $80 million, up from $27 million in 2024 and just $4 million in 2023. The platform now facilitates over $1 billion in annual sales across 185,000+ vetted creators and 1,200+ brand partners. In August 2025, ShopMy launched Circles, a consumer-facing shopping app built around curated product feeds. Within months, users had created 30,000+ Circles and wishlisted over 150,000 products. The company is no longer just a backend tool for brands; it is becoming a shopping destination in its own right. Key Figures: Why it works: Shoppers are tired of being sold to by algorithms. When a creator they follow and trust recommends a product, it feels like advice from a friend, not an ad. ShopMy has built the infrastructure that makes that trust transaction scalable, measurable, and profitable for everyone involved. 3. Little Spoon – Direct-to-Consumer Baby and Kids’ Food Parents are tired of processed baby food filled with preservatives. Little Spoon delivers fresh, organic meals for babies and toddlers, shipped cold and ready to eat. Their Babyblends line covers first foods for infants, while their Plates range for toddlers includes meals like turkey meatballs and quinoa bowls. They also offer vitamins and probiotics under their Boosters line. In March 2026, they launched organic infant formula, making them a genuine one-stop shop for children’s nutrition from birth through the big kid years. Here is what the traditional baby food industry never figured out: millennial parents do not trust what they cannot read on the label. They grew up Googling ingredients and questioning everything. Little Spoon built its entire brand around that scepticism, making transparency a feature rather than a legal requirement. Little Spoon has raised $90 million in total funding across five rounds and has delivered meals to over 300,000 families since launch. In 2025, the company became the first and only baby food maker in the U.S. to publicly set EU-aligned safety standards and share test results for heavy metals, pesticides, and plasticisers. That is an unusually bold move in a category where most brands stay quiet on ingredient testing. It paid off in brand trust. The subscription model is the engine behind the business. Parents who sign up once tend to stay for years, moving from Babyblends to Plates to the Boosters vitamin line as their children grow. That lifetime value per customer is what makes the unit economics work. Key Figures: Why it works: The subscription model creates predictable revenue and deep customer loyalty. Once a parent trusts a brand with their baby’s food, switching costs are high. Not financial switching costs, emotional ones. That is a powerful moat. 4. Market Wagon – Online Farmers Market Farmers markets are amazing, but who has time to go every weekend? Market Wagon brings local farms to your doorstep. You can order grass-fed beef, organic eggs, artisan cheese, and fresh-picked produce, all from small farmers in your area. They handle delivery, so you get farm-fresh food

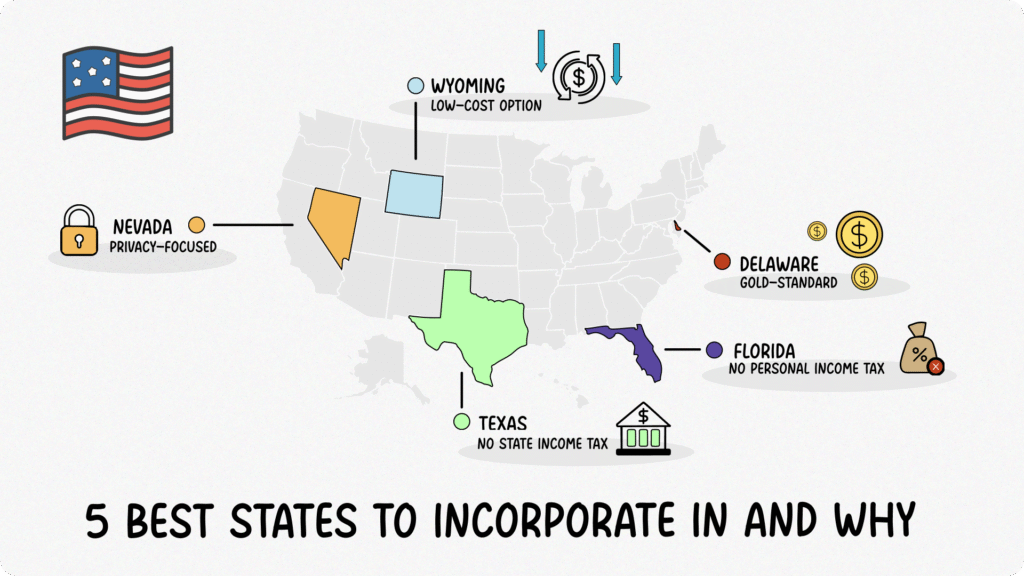

5 Best U.S. States to Incorporate In: 2026 Tax & Legal Guide

Choosing where to legally anchor your business is a major decision that impacts your tax liabilities, how easily you can manage your company, and your long-term legal protection. Many entrepreneurs default to filing in their home state, only to realize later that their funding strategies or business models would have been better served by a different jurisdiction. There is no single “best” state for every business. The right choice depends entirely on your capital structure, privacy requirements, and where you physically operate. This guide breaks down exactly how Delaware, Wyoming, Nevada, Texas, and Florida offer distinct advantages for corporate formation, looking beyond basic filing fees to examine the underlying legal and tax frameworks that impact your growth. In this Article Key Factors in Selecting a State When evaluating a state for incorporation, you need to look at four primary financial and regulatory angles. The right balance depends entirely on your specific business priorities. Comprehensive State-by-State Analysis Delaware: The Institutional and Venture Capital Standard Delaware differentiates itself not by being cost-effective, but by acting as the universally accepted legal framework for outside investors. While other states pitch low fees, Delaware focuses on corporate flexibility, maximizing options for complex equity structures, and offering unparalleled legal predictability. This is why tech giants like Alphabet (Google), Amazon, Apple, and high-growth scale-ups like Stripe and Airbnb choose Delaware. Note on Delaware LLCs vs. Corporations: If you form an LLC instead of a corporation in Delaware, you owe a flat $300 annual tax due June 1 each year instead of the franchise tax, and you do not need to file an annual report. Wyoming: Low-Cost Maintenance and Administrative Simplicity Wyoming differentiates itself by offering the leanest, most affordable corporate maintenance structure in the country. Where Delaware targets venture-backed corporations, Wyoming targets solopreneurs, digital nomads, and bootstrapped e-commerce brands looking for solid asset protection without ongoing paperwork burdens. Nevada: Premium Privacy and Robust Asset Protection Nevada differentiates itself by actively shielding corporate leadership teams from public visibility. It combines a zero-tax structure with some of the strictest operational privacy rules in the United States. Texas: Scaling Infrastructure and High-Volume Local Markets Texas differentiates itself by being an operational powerhouse rather than a passive filing haven. It is built for growing agencies, technology scale-ups, and companies that intend to establish a physical footprint, hire local talent, and capture market share within a massive domestic economy. Important Compliance Note: Even if your revenue is below the $2.65 million threshold and you owe zero franchise tax, you are still required to file a Public Information Report with the Texas Comptroller by May 15 each year. Skipping this filing triggers a $50 penalty. Florida: Balanced Taxation and Regional Ecosystem Growth Florida differentiates itself by offering an ideal tax environment for business owners who prioritize personal income retention. It strikes a highly attractive balance with a predictable low-rate corporate tax and a completely tax-free landscape for individual income. TL;DR: Summary Matrix State Primary Strategic Advantage Best Suited For Top Operational Priority Delaware Institutional credibility, VC readiness, advanced corporate courts Venture-backed startups, high-growth entities, complex boards Raising Outside Capital / IPO Roadmap Wyoming Maximum affordability, asset shielding, low paperwork Solopreneurs, e-commerce, bootstrapped digital companies Minimizing Upkeep & Protecting Solo Assets Nevada Strict leadership anonymity, asset protection, business courts Privacy-conscious owners, asset managers, mid-size firms Maximum Operational Privacy Texas Massive regional market, zero franchise tax under $2.65M revenue Agencies, regional employers, manufacturing, tech scale-ups Scaling Physical Infrastructure & Local Hiring Florida Balanced founder tax environment, high consumer market access Profitable brands, regional agencies, expanding tech hubs Founder Wealth Maximization & Distribution Critical Questions Before Filing To avoid inadvertently triggering double-compliance obligations, analyze these operational realities prior to registration: Final Thoughts Every entrepreneur starts exactly where you are right now: staring at a blank filing form, weighing numbers, and trying to predict the future layout of their company. If you find yourself stuck in analysis paralysis, simplify your decision by looking at your business model’s immediate 12-month horizon: Once you have identified the state that aligns with your current priorities, your next steps are straightforward: secure a registered agent in that jurisdiction, file your Articles of Organization or Incorporation, and obtain your federal EIN. One final reminder that applies regardless of which state you choose: incorporating in a different state from where you actually live and operate does not eliminate your home state tax obligations. You will almost certainly need to register as a foreign entity in your operating state, meaning you pay fees and meet compliance requirements in both. Factor this into your total cost comparison before making a final decision. By taking the time to match your state selection to your actual operational strategy today, you protect your personal assets and build a clean foundation for wherever your business takes you next. For a visual breakdown of how these specific legal and financial trade-offs operate side-by-side, this Wyoming LLC vs. Delaware LLC video provides a practical analysis of ongoing maintenance fees, asset protections, and exact filing pathways to help you choose the correct entity structure. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

15 Highest Paying Freelance Jobs in 2026 (With Real Rates, Growth Stats, and Exactly Where to Start)

I was chatting with an ex-FAANG engineer at a co-working space the other day. He had left Big Tech in 2019 to freelance full-time. I assumed he had traded a cushy salary for a bit more freedom, but I was wrong. He is actually out-earning his old salary now, and the real win is that he can trade his standing desk for a surfboard on a Wednesday morning without checking a calendar or asking for permission. Stories like his are not rare anymore. The freelance economy has matured, and companies now view top contractors as mission-critical talent, not budget line items. According to industry research from April 2026, an estimated 70 to 73 million workers, approximately one third of the labour force, engage in independent or gig work in some capacity. At the upper end of the market, highly specialized roles regularly command triple-digit hourly rates. Below are 15 freelance careers that pay exceptionally well and give you the freedom to spend afternoons with family, jet off on a moment’s notice, catch the perfect swell, or whatever your version of freedom looks like. In this Article Is 2026 Actually a Good Time to Go Freelance? The short answer: it depends entirely on what you do. AI is the elephant in the room, and it cuts both ways. On the threat side, entry-level creative and writing work has been hit hard. If you were charging $30/hr for basic blog posts or simple graphic design, that pipeline has thinned considerably. Junior roles that once served as stepping stones into freelance careers are disappearing faster than anyone expected, and that is a genuine problem worth acknowledging. But here is where it gets interesting. The same AI wave that is eroding entry-level work is creating an acute shortage of senior specialists who can work with it. Enterprises can now prototype faster and cheaper than ever before, but someone still needs to validate the output, fix what the model gets wrong, and translate technical results into business decisions. That someone is increasingly a senior freelance specialist brought in on contract. The people building AI pipelines, auditing AI security vulnerabilities, and advising boards on AI strategy are in higher demand today than they were two years ago. There is also a structural tailwind that has nothing to do with AI. Companies are leaner than ever. Hiring a full-time specialist with salary, benefits, equity, and office space is expensive and slow. A freelance expert who parachutes in, solves the problem, and invoices cleanly is increasingly the preferred model for project-based work. The honest summary: if you are early in your career or working in commoditised skills, 2026 is a challenging market. If you are a senior specialist with a track record in a high-demand field, the conditions have rarely been better. The roles on this list belong firmly in the second category. The 15 High-Paying Roles Each role on this list meets three criteria: it commands a meaningful hourly rate (above $40/hr at entry), it has documented demand growth, and it is genuinely accessible to a freelancer without needing to be on-site five days a week. Annual earning estimates are based on 20 billable hours per week, applied consistently across every role in this article. Pressed for time? [Click here to skip to the full rate comparison table.] 1. Blockchain (Web3) Developer Blockchain is no longer a buzzword; it underpins billions of dollars worth of transactions in finance, supply chain, and even gaming. Even though the crypto market has seen its share of volatility, demand for skilled blockchain engineers remains strong because companies still need private ledgers, supply-chain tracking, and secure tokenisation. From writing tamper-proof smart contracts to auditing DeFi protocols for seven-figure exploits, top-tier engineers sit at the crossroads of money and math, and companies happily pay to keep them on speed-dial. Why demand is surging: The global blockchain technology market is projected to grow from $47.96 billion in 2026 to $577.36 billion by 2034, at a compound annual growth rate of 36.5% (Fortune Business Insights, 2025). Enterprises across finance, healthcare, and logistics are actively hiring, and there simply are not enough qualified developers to go around. Typical Rate: $50 – $150/hr Annual Earning Potential: $52,000 – $156,000 2. AI / Machine-Learning Consultant AI is red-hot, and every investor is hunting for the next breakthrough. Enterprises are scrambling to move from “AI pilot” to real ROI, but pre-trained models still need custom data, guardrails, and cost controls. Freelance ML pros step in to fine-tune LLMs, build anomaly-detection pipelines, and translate geek-speak into boardroom slides. When a single algorithm tweak can save or earn millions, these specialists name their price. Why demand is surging: LinkedIn’s 2025 Jobs on the Rise report showed AI Engineer roles growing at 59% year-over-year, the fastest of any role tracked. The median annual salary for full-time AI/ML engineers sits at $145,000 (US Bureau of Labor, 2024), which gives you a sense of what companies are willing to pay for this expertise on a permanent basis, let alone contract. Typical Rate: $120 – $160/hr Annual Earning Potential: $124,800 – $166,400 3. Cloud Architect/Engineer One mis-tagged S3 bucket can leak data, and unoptimized infrastructure wastes over 80% of a company’s container budget on idle resources. Large companies know that poor cloud setup risks both security breaches and massive unexpected bills, so they take cloud architecture very seriously. Architects who tame AWS, Azure, or GCP keep uptime high and costs low, guiding organisations through migrations and DevOps automation. Their invoices cost far less than the cloud horror stories they prevent. If cloud architecture is about building the fortress, the next role on this list is about defending it. The two skills frequently appear on the same enterprise contract. Why demand is surging: (BLS) projects cloud architect roles to grow 13% through 2033, well above the national average of 4%. The average annual salary for a full-time cloud architect sits at $150,000 (Glassdoor), making freelance contracts in this space extremely well-compensated. Typical Rate: $80 – $180/hr Annual Earning Potential: $83,200 – $187,200 4. Cybersecurity Specialist A single breach now averages $4.4M (IBM 2025). High-profile incidents like the Equifax breach and Colonial Pipeline hack have shuttered operations overnight. Ethical hackers and compliance experts harden networks, run red-team drills, and navigate audits. The pitch to clients essentially writes itself: pay me five figures now, or pay ransomware double

7 Tips to Build a Seven-Figure Business for Freelancers and Small Business Owners

Growing a business beyond the early stages is a constant evolution. In the beginning, success comes from sheer hustle, saying yes to every opportunity, learning on the fly, and doing whatever it takes to get paid. But at some point, the same approach that helped you grow becomes the very thing that holds you back. The truth is, the jump from six to seven figures is not about working more hours. It is about shifting how you think, how you operate, and how you structure your business so it can grow without depending on you for every task. This is the moment when you stop being the person who does the work and start becoming a builder of a business that can scale. Here are seven practical, human, and sometimes uncomfortable tips to guide you toward the one million dollar milestone. Tip 1: Treat Adaptability as a Daily Habit If there’s one thing guaranteed in business, it’s change. The strategy that helped you thrive two years ago might barely move the needle today. AI has transformed how service businesses operate, client expectations are evolving, and new competitors appear overnight. A seven-figure business isn’t built by clinging to what used to work. It grows because the owner stays curious, open, and willing to adjust. Adaptability doesn’t mean chasing every trend; it means evolving your offers, systems, and approach before the market forces you to. Tip 2: Be Honest With Yourself (Even When It’s Uncomfortable) A powerful trait shared by successful founders is intellectual honesty. It’s the ability to look at your business with clear eyes, even when the truth stings a little. Review your numbers and ask the hard questions: • Which clients are truly profitable? • Where are we losing time, money, or energy? • Is this offer still relevant? Honest evaluation doesn’t make you pessimistic. It makes you intentional, and that precision fuels smarter decisions as your business scales. Tip 3: Make Clients Feel Seen, Not Sold To You don’t need the flashiest sales pitch to grow; you need empathy that makes clients feel genuinely understood. Before a meeting, don’t just rehearse your offer. Learn about the client, their industry, their recent wins or challenges, and what truly matters to them. Ask thoughtful questions. Listen more than you talk. Tailor your solution like it was built just for them. Clients stay longer, spend more, and refer better when they feel seen and supported, not pushed. Tip 4: Write Things Down (Your Future Team Will Thank You) A freelancer sells time. A business sells a repeatable experience that doesn’t depend on one person. The moment you find yourself repeating a task, it’s ready to be documented. Create simple Standard Operating Procedures (SOPs) so anyone can deliver the same level of client experience. SOPs reduce errors, speed up onboarding, and turn your know-how into real business value. Someday, these processes might be what makes your company sellable or scalable. Tip 5: Start Delegating Before You Feel Ready If you’re doing everything yourself, growth will always hit a ceiling. Delegation isn’t about handing off tasks; it’s about handing off ownership. Instead of hiring someone to “help with admin” or “post on social media,” look for people who can manage an entire function. Free up your time for what only you can do: strategy, relationships, product innovation, and growth. That’s where seven-figure leaps are made. Tip 6: Say What You Mean and Follow Through High-trust communication is one of the most underrated growth engines. In a world where many over-promise and under-deliver, doing what you said you would do instantly sets you apart. Clients remember how you make them feel. Teams stay when they feel respected. Partners refer you when they trust you. Marketing gets attention, but relationships build momentum. Tip 7: Treat Failure as Feedback, Not a Full Stop Not every offer will sell. Not every hire will work out. Not every idea will land. That’s normal for any business growing to seven figures. The difference is how you respond. Instead of letting a setback derail you, ask: • What did this teach me about timing, audience, offer, or pricing? • What would I adjust next time? Resilience isn’t avoiding mistakes; it’s refusing to repeat them. Your Next Move: Get Clarity Behind the Scenes Many founders stay stuck not because of lack of ambition, but because their financial picture feels overwhelming or unclear. The moment you understand your numbers, everything becomes easier: pricing, hiring, investments, and planning for growth. You don’t need to untangle it alone. Schedule a Fynlo demo and get a clear view of your finances so you can scale with confidence and less stress.

9 Fastest Growing Industries for Freelancers & Small Businesses in the U.S. Right Now

Freelancing is no longer just a side gig — it’s become a full-time career path for millions of Americans. As businesses increasingly prefer flexible, specialized talent, demand is surging in certain fields. If you’re a freelancer or small business owner trying to figure out your next move, this article is for you. We’ll cover 9 of the fastest-growing industries in 2025, detailing the exact high-paying roles in demand and the market data that proves these niches are where you should focus your expertise. Table of Contents Quick-View: The Top 9 High-Growth Freelance Industries (2025) Here’s a snapshot of the fastest-growing freelance industries in 2025, plus the top roles and what’s driving demand in each. Use this list to spot where your skills fit best. Industry Focus Top In-Demand Roles Growth Driver 1. AI, Automation & Emerging Tech AI Engineer, Prompt Designer, Automation Specialist Businesses are racing to integrate AI into customer support and data processing. 2. Digital Marketing, Content & Creative Design SEO Strategist, Video Editor, Brand Content Producer, Graphic Designer Explosive growth of the “Creator Economy” and need for cost-effective, specialized marketing. 3. Web Design, No-Code Tools & UX/UI Webflow Designer, UX/UI Consultant, E-commerce Specialist Businesses need fast, customer-friendly, and scalable digital experiences. 4. FinTech & Blockchain FinTech Compliance Consultant, Blockchain Developer, Financial Content Writer Massive innovation and funding in digital banking and payments require regulatory and technical experts. 5. Consulting, Operations & Project Management Remote Project Manager, Process Consultant, Workflow Specialist Companies are replacing full-time operations staff with specialized, part-time remote experts. 6. Online Education & E-Learning Course Creator, Instructional Designer, Specialized Tutor Global e-learning market projected to reach $475B by 2030 as companies invest in upskilling. 7. Sustainability & ESG Consulting Carbon Accounting Expert, ESG Reporting Specialist, Environmental Storyteller New regulations and soaring consumer/investor expectations drive mandatory reporting. 8. Cybersecurity & Data Protection Penetration Tester, Privacy Consultant, Compliance Auditor Persistent shortage of qualified professionals amid a massive, growing global threat landscape. 9. Telemedicine & Virtual Health Services Telehealth UX Designer, Patient Education Writer, Virtual Health Coach Robust market expansion driven by patient demand and technological adoption in healthcare. See details below for each industry. 1. AI, Automation & Emerging Tech AI is reshaping how freelancers work — and it’s also creating brand-new opportunities. Independent market analyses consistently show that highly skilled freelancers in specialized technical areas are commanding premium rates. For instance, experts in Artificial Intelligence and Machine Learning frequently earn $150 per hour or more globally, positioning this sector among the highest-earning freelance fields. Businesses are racing to integrate AI into customer support, marketing, and data processing, creating openings for AI engineers, prompt designers, chatbot builders, automation specialists, and even creative AI consultants. This can be seen with freelancers building workflow automations with tools like Zapier, or AI-powered chatbots for small businesses. High-profile examples include 2. Digital Marketing, Content & Creative Design Even as AI grows, marketing remains a deeply human field, and the digital creator economy has exploded. Businesses constantly need fresh visuals, compelling brand storytelling, SEO strategies, and ad campaigns — and most turn to freelancers to fill the talent gap. According to a 2025 report from the Interactive Advertising Bureau (IAB), digital creator jobs in the U.S. jumped from roughly 200,000 in 2020 to 1.5 million in 2024—a 7.5x increase. The U.S. freelance market continues to expand as companies seek specialized expertise that is also cost-effective. In fact, 63% of small businesses report saving up to 30% on marketing costs by outsourcing compared to building an in-house team. This high demand means video editors, copywriters, SEO strategists, and graphic designers remain top-requested roles. Case in Point: Independent professionals find success running niche agencies, mastering platforms like Fiverr and 99designs, or scaling one-person media operations (like MKBHD or Ali Abdaal) using freelance editors and scriptwriters. 3. Web Design, No-Code Tools & UX/UI In 2025, if your business isn’t online, it simply won’t survive. The Freelance Platforms Market is forecast to grow from $1.3 billion in 2023 to $5.2 billion by 2032, driven largely by businesses seeking freelance web and UX designers to build customer-friendly digital experiences. No-code platforms like Webflow, Bubble, and Framer make it possible for designers to deliver fast, scalable websites without large teams — ideal for freelancers. For instance, small studios like HJ Web Studio or solo designers specializing in Shopify stores. Freelancers on Dribbble or Behance who master both design and conversion optimization are particularly in demand. 4. FinTech & Blockchain The financial technology sector is one of the most innovative and heavily funded areas in the U.S., driving massive demand for specialized, flexible talent. This market is exploding because traditional banks are rapidly digitizing, and startups are constantly creating new payment rails, lending apps, and investment tools. The pace of innovation means businesses critically need expertise in two key areas: regulatory compliance and secure development. The scale of this opportunity is massive: the North American FinTech market is projected to grow fourfold to $520 billion in 2030, fueling continuous, high-value project work. This environment is ripe for freelancers who specialize in areas where finance and technology merge. Top roles include the FinTech Compliance Consultant (advising on evolving regulations like KYC/AML), the Blockchain Developer (building secure, decentralized applications), and the Financial Content Writer (creating clear, authoritative content for investment and banking platforms). Companies often hire these independent experts to bypass the time and cost of an in-house team. Freelancers are brought in specifically to navigate complex regulatory landscapes or accelerate the launch of platform features like cross-border payments, making this a stable and high-value niche. 5. Consulting, Operations & Project Management Remote work has created a growing need for freelance project managers, process consultants, and operations specialists. Many small companies now hire part-time experts instead of full-time employees to streamline their systems. The FlexJobs 2025 State of Remote Freelance Jobs report highlights consulting and operations among the most in-demand freelance sectors, particularly for remote-first teams. Examples of this trend include freelancers assisting startups with managing product

7 Financial Red Flags U.S. Small Businesses & Freelancers Can’t Afford to Miss

Running your own business comes with freedom and flexibility — but it also comes with paperwork, deadlines, and financial risks. While invoices and expense spreadsheets may not feel as urgent as closing the next client or shipping the next order, they’re often where trouble starts. In fact, 82% of small business failures are linked to cash flow problems. In fiscal year 2024, the IRS assessed $84.1 billion in civil penalties overall, much of it hitting small businesses who missed deadlines or mismanaged cash. Here’s the bright side: Your financial reports can act like a smoke alarm — they’ll tell you when something’s wrong long before the fire spreads. The trick is knowing what to look for. We’ve compiled 7 critical financial red flags that U.S. small businesses and freelancers often overlook. By learning how to read financial statements and spot these warnings in your financial data, you can take corrective action today and secure your future growth. We’ll also share simple benchmarks so you can see how your numbers stack up. Table of Contents 1. Profit is Up, But Cash Flow is Down (Slow Collections) This is the most important warning sign. Your Cash Flow Statement tracks the actual money moving in and out of your business, while your Income Statement tracks profit on paper. If your income statement shows a profit, but your cash flow statement is consistently negative, it means you’re failing to convert sales into usable cash. This is usually due to clients taking too long to pay (Days Sales Outstanding, or DSO), which traps your capital. The Warning Sign: You frequently need to rely on loans or personal savings to cover routine bills, even though you have a high volume of pending invoices. Benchmark to Watch: A healthy DSO is usually under 45 days. If it’s much higher, you may be heading into small business cash flow problems. How to Address It: 2. Your Profit Margin is Falling Your Gross Profit Margin (found on your Profit & Loss Statement) is the percentage of revenue left after paying the direct costs of your product or service (Cost of Goods Sold). If this margin shrinks, it means you’re making less money on every sale, even if your total sales volume is high. The Warning Sign: Your overall revenue is up, but the percentage of profit you keep per project or item is falling steadily. Benchmark to Watch: For many service-based freelancers, a gross margin of 50% or higher is considered healthy, while product businesses often target 30–40%. How to Address It: 3. Excessive Debt-to-Equity Ratio Found on the Balance Sheet, the Debt-to-Equity (D/E) ratio compares your total debt to your owner’s equity. A high D/E ratio signals that your business is heavily financed by loans and credit cards, making it vulnerable to interest rate hikes and economic downturns. The Warning Sign: Your debt is growing rapidly without a corresponding increase in retained profit. Benchmark to Watch: A D/E ratio above 2:1 is considered risky for most small businesses, though some industries (like construction) can sustain higher leverage. How to Address It: 4. Inventory Is Sitting Too Long (Low Inventory Turnover) If your business sells physical products, your Inventory Turnover rate is key. A low rate means products are taking a long time to sell. This ties up working capital and increases the risk that your stock will become outdated. The Warning Sign: You frequently have too much product in storage, leading to high holding costs and frequent markdowns. Benchmark to Watch: Most retailers aim for an inventory turnover of 4–6 times per year. If you’re under that, capital is likely tied up in slow-moving goods. How to Address It: 5. Discrepancies in Account Reconciliation Account reconciliation is the process of matching every transaction in your bank statements with your accounting software entries. Skipping this is a critical operational failure that masks mistakes, unrecorded fees, and, worst of all, potential fraudulent activity. The Warning Sign: You haven’t compared your bank statement to your accounting software records in over 30 days. How to Address It: 6. Owner Draws Exceeding Net Income For freelancers and sole proprietors, the “Owner’s Draw” is the cash you pull out of the business for personal use. If your draws are consistently higher than your actual Net Income, you are dangerously liquidating the business’s capital reserves and emergency cash. The Warning Sign: You find yourself taking larger, erratic draws that leave the business with insufficient cash to cover upcoming tax payments or slow client periods. Benchmark to Watch: Aim to keep owner draws below net income and ideally not more than 30–40% of profits, depending on your reinvestment needs. How to Address It: 7. Operating Expenses Are Growing Faster Than Revenue This is a subtle but dangerous red flag often found on the Profit & Loss Statement. If your operating expenses (e.g., software subscriptions, rent, marketing costs, administrative salaries) are increasing at a faster percentage rate than your total revenue, your business is losing efficiency. You are investing more money to generate less relative income. The Warning Sign: You see revenue growth of 10% year-over-year, but your total operating expenses have increased by 20% or more. This means your operational efficiency is dropping. Benchmark to Watch: Track your Operating Expense Ratio = Operating Expenses ÷ Revenue. For many small businesses, keeping this under 30–35% is a healthy target. How to Address It: Final Takeaway: Red Flags Are Early Warnings Red flags don’t necessarily mean your business is failing — but ignoring them is risky. Spotting issues early gives you time to correct course before small cracks turn into financial sinkholes. And you don’t have to track all this alone. Fynlo makes staying on top of your bookkeeping, expenses, and financial reports easy. Our platform gives you a clear, real-time view of your business’s financial health, helping you spot these red flags before they become a crisis. Ready to catch red flags before they cost you? Book a quick demo with Fynlo today.

12 Costly Mistakes U.S. Small Businesses & Freelancers Make (And How to Easily Avoid Them)

Running your own business comes with freedom, creativity, and pride. But it also comes with rules — thousands of them. And if you break those rules, even by accident, you can get slapped with fines that derail your finances. The numbers show how high the stakes can be. In fiscal year 2022, the IRS assessed $73.6 billion in civil penalties, and compliance missteps remain one of the biggest obstacles for entrepreneurs. According to the MetLife & U.S. Chamber of Commerce Small Business Index (Q4 2024), 51% of small businesses reported that regulatory requirements are actively hindering their growth. And when you’re already juggling sales, clients, and payroll, the last thing you need is a surprise bill from the government. The good news? Most of these fines are avoidable once you know where the landmines are. Here’s a breakdown of 12 common small business fines, what they cost, and how to protect your business from these costly mistakes. Table of Contents 1. Late-Filing Penalty (Income Tax) This is one of the most common pitfalls for new entrepreneurs. Missing the deadline to file your business or personal tax return can trigger a significant penalty from the IRS. The penalty is typically 5% of the unpaid taxes for each month or part of a month that the return is late, with a maximum cap of 25%. How to Avoid It: 2. Underpayment Penalty (Estimated Taxes) As a freelancer or sole proprietor, you are required to pay income and self-employment taxes in four quarterly installments throughout the year. If you don’t pay enough by the due date for each quarter, the IRS can impose an underpayment penalty. This often catches new business owners by surprise, as they may assume they can simply pay their entire tax bill in April. How to Avoid It: For a detailed breakdown of deadlines and calculations, read our blog: The Freelancer’s Guide to the 2025 Self-Employed Quarterly Tax Schedule. 3. Misclassification Fine Misclassifying a worker as an independent contractor when they should be an employee is a major red flag for both the IRS and the Department of Labor (DOL). While using contractors can be more flexible for your business, the government has strict rules. If they determine you’ve misclassified a worker, you could face severe fines and be required to pay back taxes, interest, and other penalties. Some states impose fines of tens of thousands of dollars per misclassified worker. How to Avoid It: 4. Forgotten 1099-NEC Penalty If you pay a contractor $600 or more in a single tax year, you are required to file a Form 1099-NEC with the IRS and provide a copy to the contractor. Many small business owners overlook this crucial step. The fines for late or incorrect filing can be steep, ranging from $60 to $330 per form, with a penalty of $660 per form for intentional disregard. The deadline is typically January 31st. How to Avoid It: 5. OSHA Workplace Safety Fine Even if you run a small office or a creative studio, you are legally required to provide a safe working environment for your employees. The Occupational Safety and Health Administration (OSHA) can inspect your premises and issue fines for violations. For 2024, the penalty for a “serious” violation can be up to $16,550 per violation, while a “willful” or “repeated” violation can reach a maximum of $165,514. Don’t think you’re too small to be noticed; many businesses are fined for common oversights like failing to have a clear exit path or not providing basic safety equipment. How to Avoid It: 6. ADA Website Accessibility Fine In today’s digital world, your website is considered a “public accommodation” under the Americans with Disabilities Act (ADA). This means it should be accessible to people with disabilities who rely on screen readers, keyboard navigation, or other assistive technologies. The ADA doesn’t publish a fixed fine schedule for websites. Instead, enforcement usually happens through lawsuits or settlements. These cases can be costly—legal fees and settlements often run into the tens of thousands of dollars, and in some cases much higher. The Department of Justice can also impose civil penalties, which currently range up to $75,000 for a first violation and $150,000 for subsequent violations—but in practice, the real financial impact often comes from litigation costs. How to Avoid It: 7. Data Privacy Violation Fine If your business collects any customer data—even just names and email addresses—you have a legal responsibility to protect it. With new laws like California’s CCPA, fines for data breaches or mishandling can be astronomical. Violations can range from tens of thousands of dollars to much more, depending on the severity and number of people affected. How to Avoid It: 8. Unpaid Sales Tax Fine For businesses that sell physical goods (or certain taxable services), collecting and remitting sales tax is legally required. Many small businesses run into trouble because they’re unaware of their state’s nexus laws—the thresholds or connections (sales volume, number of transactions, physical presence) that trigger sales tax obligations. Penalties and interest for late or unpaid sales tax vary widely by state and situation. In typical cases, fines might be 10–30% of the tax owed, plus interest. But in more serious cases—such as fraud, willful evasion, or repeat violations—some states may impose penalties ranging up to 50% or more of the unpaid tax. How to Avoid It: 9. Trademark/Copyright Infringement Fine Using a protected logo, image, song, or slogan without permission can quickly turn into a legal nightmare. Many small business owners run into this problem by pulling images or music from the internet, assuming they’re “free to use.” In reality, infringement lawsuits are often far more expensive than simply licensing the material. How to Avoid It: 10. Unlicensed Business Fine Depending on your industry and location, you may need a specific business license to operate legally. This can be anything from a home-based business license to a professional license for a service provider. Operating without the necessary license can result in fines from city, county, or

Payroll for Your First Employee: Everything U.S. Small Businesses Need to Know Before Making Their First Hire

Congratulations! Hiring your first employee is a monumental step for any small business or freelancer. It means your business is growing, your vision is expanding, and you’re ready to take on new challenges. But with this exciting milestone comes a crucial responsibility: payroll. For many new employers, the word “payroll” conjures images of complex forms, confusing calculations, and potential IRS penalties. It can feel like stepping into a minefield! But don’t let that overwhelm you. While it’s true that payroll compliance requires attention to detail, breaking it down into manageable steps makes it much less daunting. This guide will walk you through everything you need to know to set up payroll legally and efficiently for your very first hire in the U.S. We’ll cover federal and state requirements, common pitfalls, and smart strategies to ensure both you and your new team member start off on the right foot. Table of Contents Before You Hire: Employee vs. Independent Contractor This is arguably the most critical decision you’ll make upfront. Mistakenly classifying an employee as an independent contractor can lead to severe penalties from the IRS and state labor departments. The IRS uses several factors (behavioral, financial, and type of relationship) to determine classification. When in doubt, err on the side of caution or consult a professional. The consequences of misclassification—like back taxes, penalties, and interest for unpaid payroll taxes (Social Security, Medicare, unemployment)—can be financially devastating. Setting Up Payroll in 7 Easy Steps Once you’ve decided you’re hiring an employee, here’s a checklist to get your payroll system up and running: 1. Get an Employer Identification Number (EIN) The first and most important step is getting your Employer Identification Number (EIN) from the IRS. It’s the unique ID that helps identify your business for tax reasons at both the state and federal levels. The application is free and can be completed online on the IRS website—and you’ll need it to report taxes, hire employees, and open business bank accounts. Once you have your EIN, the IRS’s Publication 15, Employer’s Tax Guide is a must-read resource to understand your ongoing payroll tax responsibilities. 2. Register with State’s Labor and Tax Agencies This step is crucial and varies by state. At a minimum, you’ll need to register for state income tax withholding (if your state has an income tax) and state unemployment insurance (SUI). These registrations allow you to properly withhold taxes from your employee’s paycheck and pay into your state’s unemployment system. Many states also require you to secure workers’ compensation insurance, often starting with your very first employee. A quick search for “new employer registration” plus your state name will usually point you to the correct agency. For example, in California you’d register with the Employment Development Department (EDD), while in Texas you’d register with the Texas Workforce Commission (TWC) for state unemployment insurance (since Texas has no state income tax). 3. Gather Employee Paperwork Before your first employee starts, they’ll need to complete several essential forms: 4. Choose Your Payroll Schedule Will you pay weekly, bi-weekly, semi-monthly, or monthly? Bi-weekly (every two weeks) is common for many small businesses, resulting in 26 paychecks per year. Whatever you choose, be consistent and communicate it clearly to your employee. State laws often dictate minimum pay frequency. 5. Understand Federal Payroll Taxes The next critical step is understanding the federal taxes you’re responsible for. As an employer, you have a legal obligation to withhold and pay several taxes on behalf of your employees. These include: Since tax rates are updated regularly, always confirm with IRS publications or online calculators to verify your withholdings. 6. Understand State and Local Payroll Taxes Beyond federal taxes, you’ll also deal with: 7. Choose a Payroll Method Now for the big question: how will you actually run payroll? Estimates from the American Payroll Association (APA) show that automated payroll solutions can reduce processing costs by as much as 80% compared to manual methods. This isn’t just about saving money; it’s about avoiding costly mistakes and the substantial fines that can come with them. Don’t Let Payroll Be a Headache! Hiring your first employee should be an exciting journey, not a source of stress over tax liabilities and complex regulations. Getting your small business payroll right from the start protects your business, builds trust with your new team, and ensures you remain compliant with the IRS and state agencies. Remember, penalties for late or incorrect filings can quickly add up, turning a small oversight into a big problem for your small business finances. This is where a tool like Fynlo comes in. Our easy-to-use software is designed for small business owners and freelancers, providing the real-time financial insights you need to manage your business effectively. By streamlining your core accounting and bookkeeping tasks, Fynlo gives you a clear picture of your income and expenses, empowering you to confidently manage payroll costs and stay on top of your financial obligations. Ready to make your first hire confidently? Start a free trial to see how Fynlo can help simplify your financial management.

Mastering Cash Flow Management: The #1 Reason Small Businesses Thrive

Ever wonder what truly separates a thriving small business from one that struggles? It’s not just a brilliant idea or massive profits; it’s the art of cash flow management. While profit is certainly vital, having enough cash in the bank to cover your expenses, invest in growth, and seize opportunities is the real game-changer. It’s a skill that’s more critical than ever, with a staggering 88% of U.S. small businesses facing cash flow disruptions. The good news is, by mastering cash flow, you gain immense power to protect your business, reduce stress, and set yourself on a path to lasting financial stability. Let’s explore the essentials of cash flow management, from what it is to how you can take control of it today. Table of Contents What Is Cash Flow? It’s easy to mistake cash flow for profit, but they’re distinct concepts crucial to your business’s health. Your profit is what remains after you subtract all your expenses from your total revenue over a period—it’s a measure of your business’s overall financial performance. Cash flow, on the other hand, is the actual movement of money in and out of your business accounts. Think of your business’s bank account as a reservoir. You want a steady, predictable inflow of water (cash) to keep it comfortably full, ready for any needs or opportunities that arise. Common Challenges to Healthy Cash Flow Even the most profitable businesses can face cash flow challenges. Here are some of the most common hurdles freelancers and small businesses encounter, along with a quick solution for each: Practical Steps for Better Cash Flow Taking command of your cash flow might seem like a huge undertaking, but it’s really about implementing a few smart, consistent habits. 1. Forecast Your Cash Flow You can’t effectively manage what you don’t anticipate. Start by creating a simple cash flow forecast. Project your expected income and expenses for the next 3-6 months. This forward-looking view is like a financial weather forecast, allowing you to spot potential shortfalls before they happen. If you see a dip coming in two months, you have time to adjust spending or chase new sales. 2. Accelerate Your Income Inflow The faster cash comes in, the healthier your business. 3. Optimize Your Outflow Be strategic about how and when you pay your own bills. 4. Conquer Your Tax Obligations Don’t let tax season be a source of anxiety. Implement a system to consistently set aside funds for your tax obligations. A simple method is to automatically transfer a percentage (e.g., 20-30% for federal and state taxes) of every payment you receive into a separate, earmarked bank account. This ensures the cash is available when those quarterly estimated tax payments are due, preventing a major headache and costly penalties. Empower Your Business with the Right Tools Managing cash flow doesn’t have to be a source of stress or endless spreadsheets. The key to financial well-being for any small business or freelancer is having simple, effective tools that automate the tedious parts and give you clear insights. This is where a tool like Fynlo truly shines. Our easy-to-use software is specifically designed for freelancers and small business owners. It simplifies tracking your income and expenses, makes sending professional invoices effortless, and helps you stay on top of your estimated tax payments – all crucial elements of strong cash flow management. We take the guesswork out of bookkeeping, so you can focus your energy on growing your business and serving your clients. Ready to transform your business’s financial future? We’re here to help. You can explore how Fynlo works by starting a free trial, or schedule a call to speak with our team directly.

What is California AB 5? Complete Contractor Classification Guide for Small Businesses

Running a small business in California is like navigating a maze of regulations. One wrong turn, like misclassifying a worker, can lead to costly penalties or legal trouble. California AB 5, enacted in 2019, reshapes how businesses classify workers as employees or independent contractors, impacting your payroll, taxes, and compliance. This guide simplifies contractor classification for small business owners, offering a clear path to compliance. We’ll break down AB 5, who it affects, and the small business compliance steps you need—plus answer common questions to keep you ahead. Table of Contents What is California AB 5? California AB 5, signed into law in September 2019 and effective January 1, 2020, is a landmark labor law aimed at reducing worker misclassification. It codifies the “ABC test” from the 2018 California Supreme Court case Dynamex Operations West, Inc. v. Superior Court, making it harder to classify workers as independent contractors. AB 5 applies to California’s Labor Code, Unemployment Insurance Code, and Industrial Welfare Commission wage orders, ensuring workers receive protections like minimum wage, overtime, and benefits. In 2020, AB 2257 amended AB 5, adding exemptions and clarifications, now codified in Labor Code sections 2775–2787. The ABC test presumes workers are employees unless the hiring business proves all three criteria: A UC Berkeley study estimated 64% of workers doing independent contracting as their main job would be reclassified as employees under the ABC test. This shift increased employee protections but reduced self-employment by 10.5% and overall employment by 4.4% in non-exempt occupations, with no significant rise in W-2 employment. AB 5 protects workers and levels the playing field for businesses that properly classify employees, but it’s complex. Small businesses must understand its rules to avoid fines, which range from $5,000–$25,000 per violation for misclassification. Who is Affected by AB 5? AB 5 impacts small businesses across industries, especially those relying on freelancers or gig workers, like retail, hospitality, construction, and trucking. If you hire contractors in California or work with California-based freelancers, you’re affected, even if your business is elsewhere. Key Impacts: Exemptions: AB 2257 expanded exemptions to 109 professions, but exempt workers must still pass the Borello test, which considers factors like control, tools provided, and work duration. A U.S. Department of Labor study found 10–30% of employers misclassify workers, a persistent issue AB 5 aims to address. Implications for Small Businesses California AB 5 reshapes how small businesses operate, presenting challenges that can feel like dead ends in the compliance maze. Understanding its implications helps you navigate these hurdles and stay on track. To avoid these pitfalls, assess your current contractor classification practices now. Review worker roles, check for exemptions, and consult legal experts to ensure compliance. Taking these steps protects your business and keeps you competitive. Key Compliance Needs for AB 5 Complying with California AB 5 means understanding the ABC test, exemptions, and your workers’ roles. Small businesses face legal and financial risks if they misclassify workers, so proactive small business compliance is critical. Core Compliance Needs: Why It Matters: California loses over $7 billion annually to misclassified workers, missing out on taxes and benefits contributions. Proper classification ensures compliance and fair competition. 5 Steps to Comply with AB 5 Follow these five steps to ensure your small business complies with California AB 5 and avoids costly mistakes. Each step is designed for small business compliance with practical examples. Step 1: Audit Your Workers Review all contractors to determine if they pass the ABC test. For example, if your café hires a freelancer to redesign your website, they likely pass “B” (outside your core business of serving food). A barista, however, fails “B” and must be an employee. Use a checklist for A, B, and C criteria. Step 2: Check for Exemptions Identify if your contractors fall under exemptions (e.g., B2B, freelance writers). For B2B, ensure the contractor has a separate business entity, sets their own rates, and doesn’t work directly for your customers. For exempt workers, classification is assessed using the Borello test, a multi-factor standard; consult an attorney to verify eligibility. Step 3: Update Contracts Draft AB 5-compliant contracts emphasizing contractor independence. Specify they control their work, use their own tools, and serve other clients. For example, a photographer’s contract should note they set their schedule and provide their camera. Keep invoices and agreements for audits. Step 4: Reclassify if Needed If a contractor fails the ABC test and isn’t exempt, reclassify them as an employee. Register them with California’s Employment Development Department for taxes and workers’ compensation. Provide benefits like 10-minute rest breaks per four hours and 30-minute meal breaks per five hours. Step 5: Monitor and Consult Regularly review worker classifications as your business or laws change (e.g., AB 2257 updates). Engage an employment attorney to stay compliant, especially for complex cases like trucking or healthcare. Schedule annual audits to catch errors early. Common Questions About AB 5 Compliance Small business owners often have questions about navigating California AB 5. Below, we answer common concerns to help you understand contractor classification and stay compliant. How Can I Use B2B Exemptions? Many small businesses hire contractors for tasks like marketing or IT and wonder if they qualify for the B2B exemption. To use it, your contractor must meet 12 criteria, such as operating as a corporation or LLC, having a separate business location, and signing a written contract. These rules allow flexibility while ensuring compliance. What Documentation Protects Me During Audits? You might worry about proving contractor status if audited. Clear contracts that specify a worker’s independence—such as setting their own hours and serving other clients—are essential. Keep invoices, work agreements, and proof of their independent business (e.g., business license). These records can prevent costly misclassification claims. How Does Proposition 22 Affect My Business? Proposition 22, passed in 2020 and upheld in 2023, classifies app-based transportation and delivery drivers as independent contractors, exempting them from AB 5. However, it mandates certain benefits, such as minimum earnings guarantees and health insurance stipends for qualifying drivers. How Can I Avoid