9 Reasons Clients Switch to Fynlo for Accounting Services

Choosing an accounting partner is one of the most critical decisions a business owner can make. The right firm doesn’t just crunch numbers; it acts as a strategic partner, offering insights that fuel growth and provide peace of mind. A recent poll of more than 1,000 small business owners found that 86% see their accountant as a trusted advisor, showing just how much this relationship matters. Too often, however, we hear from new clients who felt their previous accountant was reactive, distant, or simply not invested in their success. Their relationship was transactional, not transformational. If you’re wondering whether your current accounting service is truly serving your business, you’re not alone. Here are nine of the most common reasons business owners make the switch to Fynlo. 1. We Don’t Just Report on the Past, We Co-author Your Future A common frustration for businesses is receiving year-end financial statements long after the fact, offering a history lesson rather than a strategy guide. At Fynlo, we believe your financials are a roadmap for the future. We move beyond reactive reporting. By leveraging real-time data, we provide forward-looking advice, helping you model different scenarios, forecast cash flow, and make proactive decisions that shape your business’s tomorrow. Our clients switch because they want a partner who looks through the windscreen, not just the rearview mirror. 2. You Get a Dedicated Team that Knows Your Business Are you tired of being passed from pillar to post, having to re-explain your business to a new face every few months? High staff turnover at traditional firms can leave you feeling like just another number. Fynlo is built on relationships. When you join us, you’re assigned a dedicated team that invests time to understand the nuances of your business, your industry, and your personal goals. This consistency means you always have a contact who knows your story inside and out, providing tailored advice without the endless repetition. 3. Clear, Upfront Pricing with No Surprise Bills One of the biggest anxieties in professional services is the mystery invoice. You hesitate to pick up the phone for a quick question, fearing a shockingly high bill for “time spent.” We’ve eliminated that fear. Fynlo operates on a fixed-fee model. You choose a monthly package that suits your needs, and that’s what you pay. All our packages include unlimited email and phone support, so you can call on us whenever a question arises without worrying about the clock. Clients switch for the certainty and transparency our pricing provides. 4. We Speak Your Language, Not Accounting Jargon EBITDA, GAAP, accruals, depreciation… while these terms are second nature to accountants, they can create a barrier for business owners. Our philosophy is simple: clarity is kindness. We pride ourselves on translating complex financial concepts into plain English and actionable advice. We ensure you understand the “what,” the “why,” and the “what’s next” behind your numbers. Clients switch to Fynlo because they want conversations, not lectures. 5. Seamless, Cloud-Based Technology In today’s fast-paced world, relying on spreadsheets, emails, and shoeboxes of receipts is inefficient and risky. If your accountant isn’t embracing modern technology, your business is being held back. Fynlo is a digital-first firm. We build your accounting ecosystem around powerful cloud platforms like Xero and QuickBooks, integrating apps that automate data entry, streamline payroll, and give you 24/7 access to your financial position from any device. New clients often tell us the efficiency gains from our tech stack alone were a revolutionary change. 6. Proactive Tax Planning All Year Round Did your last tax conversation happen a frantic few weeks before the filing deadline? Reactive tax preparation often means missed opportunities. At Fynlo, tax planning is a year-round strategy, not a last-minute scramble. We continuously monitor your performance and meet with you throughout the year to implement strategies that legally and ethically minimise your tax liability. Clients switch to us when they realise they should be saving on tax, not just filing it. 7. Dedicated Onboarding & Ongoing Training Switching accountants can be daunting if you fear a lengthy setup or a steep learning curve. At Fynlo, we guide you through a tailored onboarding process, importing past data, configuring your chart of accounts, and training your team on best practices. And we don’t stop there. We provide ongoing workshops and refreshers whenever you adopt a new tool or face a regulatory change. Clients switch to us because they know they will always have the support and training needed to use their financial systems with confidence. 8. Faster Response Times Few things are more frustrating than sending an urgent financial query into a black hole and then being met with radio silence. When you need information to close a deal or make a crucial spending decision, time is of the essence. We guarantee prompt communication. Our internal service standards ensure your questions are acknowledged quickly and answered thoroughly within a reasonable, agreed-upon timeframe. Clients switch to Fynlo because they feel seen, heard, and respected. 9. We’re Genuinely Invested in Your Growth Does your accountant celebrate your wins? Do they actively bring you ideas to improve your business? This is the Fynlo difference. We view ourselves as an extension of your team. Your growth is our growth. We take immense pride in helping our clients secure funding, expand their operations, and achieve their personal financial goals. People switch to Fynlo because they want more than an accountant; they want a champion in their corner. Ready for a different kind of accounting relationship? If these points resonate with you, it might be time for a change. Contact us today for a free consultation and discover how a proactive, strategic partnership with Fynlo can transform your business. Take charge of your numbers. Partner with Fynlo now.

The Pros and Cons of In-House vs. Outsourced Accounting

If you’re running a small business, you probably started out as your own “Chief Everything Officer.” That includes being the lead, and only, member of your accounting department. Late nights with spreadsheets and a shoebox full of receipts are a rite of passage for many entrepreneurs. But as your business grows, that system starts to break. The bookkeeping takes more and more of your time, tax questions become more complex, and you start to worry about what you might be missing. You’ve reached a financial crossroads: is it time to hire someone in-house, or should you outsource your accounting to an external firm? This is a major decision, and there’s no single right answer. It’s about understanding your needs, your budget, and what you want your role in the business to be. Let’s break down the pros and cons of each path. Table of Contents The In-House Route This typically means hiring a part-time bookkeeper or a full-time staff accountant. This person is your employee, working within your company on a daily basis. Pros of In-House Accounting: Cons of In-House Accounting: The Outsourced Path Outsourcing means partnering with an external firm (like Fynlo!) that handles your accounting needs remotely. You pay a monthly fee for their services. Pros of Outsourced Accounting: Cons of Outsourced Accounting: Finding the Right Fit: The partnership is crucial. You need to find a firm that understands your industry, communicates well, and feels like a genuine part of your team. TL;DR Comparison: In-House vs. Outsourced For a quick overview, here’s how the two options stack up against each other. Factor In-House Accounting Outsourced Accounting Cost High: Full-time salary + benefits + taxes + software (often $90,000+ total). Flexible: Predictable monthly fee, often a fraction of a salary. Pay only for what you need. Expertise Limited: Expertise is confined to the knowledge of one or two individuals. Broad: Access to a diverse team of specialists (tax, bookkeeping, strategy, etc.). Scalability Difficult: Scaling requires a lengthy and expensive hiring process. Easy: Services can be scaled up or down quickly as your business needs change. Control & Access High: Direct, daily management and immediate on-site access. Structured: Access is through scheduled calls and email. Less direct daily oversight. Response Time Immediate: on-demand support and instant adjustments. Defined: typically within agreed SLA, often same or next business day, and prioritised by urgency. Time Investment High: Requires time for hiring, training, and ongoing management. Low: The firm manages its own team and technology, freeing up your time. Continuity Risky: Operations can halt if your employee leaves or is unavailable. Reliable: Service is uninterrupted by vacations or personnel changes due to team structure. Best For Businesses valuing oversight, data security, and stable finances Businesses seeking cost savings, scalable solutions, and specialized expertise. Which Path is Right for You? The truth is, the best choice depends on your stage of growth. Ultimately, the goal is to get timely, accurate financial information that empowers you to make smart decisions, without draining your time or your bank account. The right solution shouldn’t just do your books; it should give you peace of mind and the freedom to focus on leading your business. Whether you’re considering bringing someone in-house or tapping into outsourced expertise, Fynlo’s advisors can help you weigh the options and find the best fit for your budget and growth plans. Schedule a free consultation today, and let us guide you toward the solution that frees you to focus on what you do best. You may also like these articles:

6 Must-Have Financial Reports Every Small Business Owner Needs

As a small business owner, you’ve got a “number” in mind. It may be new clients, annual revenue, or the amount you need in the bank to sleep easy. But in the daily grind of client work and projects, it’s easy to lose track of how you’re really doing. An Intuit survey found that 30% of small businesses struggle to track cash flow, leaving owners stressed and second-guessing their finances. Sound familiar? You’re not alone. Financial reports aren’t just for accountants—they’re your business dashboard, providing clear insights to keep you on track. Think of them like the gauges on your car’s dashboard: you don’t need to be a mechanic to read the speedometer or check the fuel level. Here are the six reports that make up your business dashboard. Table of Contents Profit and Loss (P&L) Statement or Income Statement Example of Income Statement (Source: principlesofaccounting.com) This is your business’s report card. In the simplest terms, it tells you if you made or lost money over a set period, like a month, a quarter, or a year. For years, I just watched my bank balance. If it went up, I figured it was a good month. But the P&L showed me the truth. I once discovered I was spending nearly 20% of my revenue on various software trials and subscriptions I’d forgotten about. Seeing it in black and white was the wake-up call I needed. Balance Sheet Example of Balance Sheet (Source: principlesofaccounting.com) Think of this as a snapshot of your business’s financial health on one specific day. It shows what your business is worth at that moment. This report is crucial for seeing your stability. However, because it’s a snapshot on a single day, it can’t show you the flow of money. It tells you that you have $10,000 in the bank today, but not how it got there or where it went last week. For that, you need the next report. Cash Flow Statement Example of Cash Flow (Source: principlesofaccounting.com) This is the story of the cash moving through your business. While the P&L can be misleading (it includes sales you haven’t collected cash for yet), this report tracks the actual hard cash that has come in and gone out. A frequently-quoted study by Jessie Hagen found that 82% of business failures are due to poor cash flow. This report is your early warning system. While the Balance Sheet shows a snapshot of your cash at one moment, the Cash Flow Statement is like a video, showing you exactly when money came in and when it went out over a period. This helps you spot dangerous trends, like if you’re consistently spending cash faster than you’re collecting it. Accounts Receivable (A/R) Aging Report Example of A/R Aging Report (Source: highradius.com) This is your “who owes me money?” list. It’s a simple but powerful report that gives you a detailed breakdown of all your unpaid invoices. This report is your action plan for getting paid. A Melio survey shows more than half of small businesses experience late payments by large companies, and while most operate on net 30 terms, 25% report waiting 20–30 days past the due date. Instead of a vague feeling that “some clients are late,” this report tells you exactly who to call first. Sales by Customer (or Client) Summary Example of Sales by Customer Summary (Source: avaza.com) This report can be a real eye-opener. It shows you exactly which clients are generating the most money for your business. I used to think my “biggest” client was the one who made the most noise and took up the most time. After running this report, I realized my most valuable client was actually a quiet, low-maintenance account that paid on time, every time. This insight is gold. It helps you understand who to focus on. Expenses by Vendor (or Category) Report Example of Sales by Customer Summary (Source: accurabooks.com) Just as you track where money comes from, it’s critical to see where it’s going. This report breaks down your spending so you can see every detail. Why it matters: This report helps you find “cost leaks.” You might discover that your shipping costs have quietly doubled or that you’re spending far more on one software tool than you realized. Seeing it laid out so clearly makes it easy to spot chances to save. TL;DR: The 6 Reports at a Glance From Information to Action Running these reports isn’t about creating more paperwork. It’s about trading anxiety for clarity. Start by picking just one or two of these to look at each month. Get familiar with the story they tell. When you understand your numbers, you stop guessing and start making strategic decisions. You gain the confidence that comes from truly knowing your business, inside and out. Ready for True Financial Clarity? Feeling more confident about these reports is a great first step. The next is putting them to work without losing hours of your time. At Fynlo, our software makes running these reports simple, and our team of experienced accountants can help you understand the story behind the numbers. Stop guessing and start knowing, schedule a free call with us today. You may also like these articles:

Why Our Accounting Firm Is the Best Choice for Small Businesses in 2025

Last year, 60% of small business owners said cash flow has been a problem for their company. Running a small business in 2025 is more demanding than ever. You’re not just managing your passion; you’re navigating a complex economic landscape, embracing new technologies, and making critical decisions every single day. Amidst all this, having a truly solid financial foundation is critical for survival and growth. Choosing a financial partner can make or break your year. You need a firm that doesn’t just crunch the numbers, but one that understands your ambition and the unique challenges you face. You need expertise you can trust and a team that feels like an extension of your own. At Fynlo, we’ve built our accounting practice specifically to be that partner. Here’s why we are the right choice to bring you financial clarity and confidence in the year ahead. A Foundation of Real-World Experience In accounting, experience let us anticipate issues before they become problems. It enables timely, practical advice and steady navigation through complexity. We’ve made experience the cornerstone of our team. When you work with Fynlo, you’re not handed off to a recent graduate. Our standards are intentionally high: This means the team supporting your business has spent years in the field, honing their skills and helping businesses like yours thrive. Big-Firm Expertise, Tailored for Your Business Many of our accountants began their careers at top firms like Grant Thornton, BDO, and Baker Tilly. What does that mean for you? It means we bring a level of strategic insight and best-practice knowledge typically reserved for large corporations and make it accessible for your small business. We understand sophisticated tax planning, efficient financial processes, and high-level strategy. But most importantly, we know how to scale that knowledge down and apply it in a way that is practical, relevant, and impactful for a growing business like yours. You get the best of both worlds: the discipline and insight of a top-tier firm, delivered with the personal attention and focus a small business deserves. “A design studio felt like they’d hired a mini-Grant Thornton—Fynlo’s strategic overhaul slashed their tax liability and streamlined year-end reporting.” We’re More Than Your Accountants; We’re Your Partners For many small business owners, finance can feel like a foreign language. Our primary goal is to change that. We don’t just deliver reports; we demystify the numbers and provide the financial clarity you need to make smarter decisions. We believe a true financial partner is proactive. We look ahead to help you plan for tax season, manage your cash flow, and identify opportunities for growth. We’re the team you can call with a question, knowing you’ll get a clear, thoughtful answer. We’re here to support your vision and handle the financial complexities so you can focus on what you do best: running your business. “During the last tax season, we spotted a cash-flow pinch point two months out—our advice on restructuring payment terms saved an e-commerce retailer from late fees.” What Choosing Fynlo Looks Like for Your Business in 2025 When you partner with Fynlo, you’re not just outsourcing your bookkeeping. You are investing in: “After partnering with Fynlo, a SaaS startup cut its monthly close time by 60%—reinvesting those extra hours directly into product development.” The Right Partner Makes All the Difference You pour everything you have into your business. You deserve a financial partner that is just as dedicated to your success. Ready for expert guidance and hands-on support? Let’s map out your 2025 goals and make them happen. Schedule your free consultation with the Fynlo team today.

17 Accounting Myths You Probably Still Believe (Debunked)

Most of us dive into freelancing or small-business ownership for the work itself—designing, consulting, baking. The last thing we signed up for was bookkeeping. Yet every conversation comes with unsolicited “advice” from well-meaning friends or relatives: “Just write off everything!” or “You don’t need records—just save your bank statements.” Those myths don’t just create unnecessary stress—33% of small-business owners report they regularly lose sleep over money worries—and they can cost you real dollars if left unchecked. We didn’t get into business to become accountants, so it’s easy to fall for these misconceptions. Let’s debunk these myths and give you the clarity to manage your finances confidently. Myth 1: Accounting is only for tax season. Reality: Accounting is a year-round activity that gives you a real-time pulse on your business’s health. Why It Matters: Scrambling for records in March or April creates stress, missed deductions, and rushed decisions. Reviewing your books monthly, or even weekly, lets you spot small issues, improve cash flow, and cut costs before they spiral out of control. Myth 2: I’m too small to need formal accounting software. Reality: Spreadsheets are prone to errors and can’t scale with your business. In fact, research indicates that up to 88% of spreadsheets contain significant mistakes. Why It Matters: I’ve been there. My first year I tracked everything in a spreadsheet. A single misplaced formula almost cost me $500 in underreported income. Modern cloud software is affordable, automates data entry, and lets you connect your bank feed, so you save hours and get a clearer financial picture. Myth 3: I can write off 100% of my home-office costs. Reality: You can only deduct the portion of your home used exclusively and regularly for business. Why It Matters: Over-claiming this deduction is a classic IRS red flag. You can choose the simplified method (up to $1,500) or the actual-cost method (allocating mortgage, utilities, insurance). Use whichever yields the bigger benefit, but only for truly dedicated office space. Myth 4: A business credit card can replace a business bank account. Reality: A credit card lets you borrow money, while a bank account is where your business’s cash actually lives. You need both, but a separate business bank account is especially important to manage funds properly. Why It Matters: Mixing personal and business money in one account can strip away your LLC’s liability protection, exposing your personal assets if things go wrong. It also turns bookkeeping and tax preparation into a tangled mess. A dedicated business bank account keeps your finances clear, simplifies reconciliations, and ensures your legal and financial records stay rock solid. Myth 5: I don’t need to save receipts if I have a bank statement. Reality: The IRS requires proof of purchase, and bank statements alone don’t show what you actually bought Why It Matters: Picture an auditor asking what a $200 Amazon charge covered. A bank statement alone won’t prove it was for a printer rather than a TV. Instead, digitize and tag every expense as it happens using receipt-capture apps like Dext or QuickBooks Snap. Myth 6: Profit is the same as cash flow. Reality: Your profit on paper may look healthy, but cash flow measures the actual dollars in your account that keep your business running. It’s a crucial difference, and an Intuit study found that 61% of small-business owners struggle with cash-flow issues. Why It Matters: Your Income Statement can show a big profit, but if clients haven’t paid, you can’t pay your bills. This is the single most critical survival concept. Myth 7: I can pay myself whatever’s left in the business account. Reality: You must set aside money for taxes and business savings before paying yourself. Why It Matters: Following Mike Michalowicz’s “Profit First” principle means you allocate percentages to tax and profit accounts before paying yourself. This approach prevents the panic of facing a large tax bill with no funds set aside. Myth 8: Bartering (trading services) isn’t taxable. Reality: The fair market value of services received in a trade counts as taxable income. Why It Matters: If a web designer trades $2,000 of work for $2,000 of photography, each party must report $2,000 of income. Don’t let “free” trades cost you in unreported revenue. Myth 9: An accountant is too expensive for my small business. Reality: A good accountant saves you more money than they cost. Why It Matters: They prevent mistakes, uncover deductions, and save you hours of work. For example, a $2,000 annual fee is repaid when you reclaim just 40 hours of time—hours you can spend on billable work or growing your business. This makes an accountant an investment, not an expense. Myth 10: My bookkeeper and my tax preparer are the same thing. Reality: Bookkeeping is daily transaction recording, while tax preparation is annual return filing. Why It Matters: Clean, year-round books speed up tax season and reduce preparation costs because your accountant can work directly with accurate, organized records. Myth 11: I can deduct the cost of my commute to my office or co-working space. Reality: Commutes from home to your primary workplace are non-deductible, but you can deduct business trips beyond that, such as driving to client meetings. Why It Matters: Misclassifying personal travel as business mileage invites audit scrutiny. Only log miles driven for business purposes beyond your usual commute. Myth 12: Estimated taxes are optional. Reality: If you expect to owe more than $1,000 in tax, you must pay quarterly estimated taxes. Why It Matters: The U.S. is a “pay-as-you-go” system. Missing estimated payments triggers underpayment penalties—just like an employee missing withholding. Myth 13: Putting ‘LLC’ after my name protects me from everything. Reality: An LLC shields personal assets from business debt, but it doesn’t protect you from professional negligence or from commingling personal and business funds. Why It Matters: If a client sues over an error or omission, your LLC structure will not prevent a negligence claim and your personal assets could still be at risk. Beyond separating business and personal finances,

Financial Statements: A Comprehensive Guide

Most of us who go out on our own do it for the work itself. Whether you’re a designer, a writer, or a consultant, you’re driven by the craft. But then you start your business, and you realize you’ve also become its reluctant Chief Financial Officer. I remember my first year, staring at my accounting software and feeling completely out of my depth. I was great at my actual job, but when it came to the money side, I was just guessing. I’d look at my bank account, see money in there, and figure I was doing okay. But I always had this low-level hum of uncertainty. Am I really making a profit? Am I charging enough? Where is all the money going? It turns out the answers to those questions are sitting in three financial reports. They sound intimidating, but they’re really just tools to help you trade that uncertainty for clarity. Table of Contents The Income Statement: Answering, “Did I Actually Make a Profit?” Example of Income Statement (Source: principlesofaccounting.com) This is the most basic question, and the Income Statement (often called the P&L for Profit & Loss) answers it directly. It’s a simple summary of your revenue versus your expenses over a specific period, like a month or a quarter. In my early days, I felt like I was working constantly but my savings weren’t growing. I finally sat down and looked at my P&L. The “aha!” moment wasn’t some huge, dramatic discovery. It was seeing I was spending nearly $150 a month on various software subscriptions I’d signed up for and forgotten about. It’s the small leaks that often sink the ship. The P&L helps you spot them. It shows you the real cost of doing business, beyond just the big, obvious expenses. The Balance Sheet: A Snapshot of Your Business’s Financial Health Example of Balance Sheet (Source: principlesofaccounting.com) Being profitable month-to-month is great, but you also want to know if you’re building a stable business over the long term. That’s where the Balance Sheet comes in. If the P&L is a movie of your recent performance, the Balance Sheet is a snapshot of your business’s financial health right now. It’s based on a simple formula: Assets (What you have) = Liabilities (What you owe) + Equity (What’s yours) Honestly, for a long time, I ignored my Balance Sheet. It felt too “corporate.” But it’s surprisingly practical. And critical, too: according to Intuit QuickBooks, 57% of small business owners have experienced problems with their cash flow. Business owners lose $34,000 on average by being forced to turn down work, specifically due to issues created by insufficient cash flow. That “Accounts Receivable” line shows you exactly how much money you’re waiting on from clients. Seeing that number get too big can be the nudge you need to get better about your payment terms and follow-ups. The Cash Flow Statement: Tracking Where Your Money Really Goes Example of Cash Flow (Source: principlesofaccounting.com) This is the big one. Have you ever had a profitable month on paper but felt completely broke? I’ve been there. You’ve done the work, you’ve sent the invoices, but your bank account is dangerously low and bills are due. This is a cash flow problem, and the Cash Flow Statement is the tool that explains it. It tracks the actual cash moving in and out of your business. According to SCORE, 82% of small businesses that fail do so because of poor cash flow. It’s not that they aren’t profitable, it’s that they run out of cash. A friend of mine who runs a small trade business almost learned this the hard way. His P&L looked fantastic because he was landing big jobs. But he was paying his suppliers in 30 days, while his clients were taking 60 or even 90 days to pay him. His business was profitable, but it was being starved of cash. The Cash Flow Statement made this timing gap impossible to ignore. It forced him to start collecting deposits upfront and tighten his payment deadlines. It didn’t just lower his stress; it saved his business. From Numbers to Know-How Look, nobody gets into freelancing because they have a passion for spreadsheets. But you owe it to yourself and your business to understand the basics. You don’t need to become an accountant, you just need to get curious. Start small. Ask your bookkeeper or use your accounting software to run your P&L once a month. Take 20 minutes to look at it. Where did your money come from? Where did it go? Doing this consistently replaces that vague financial anxiety with quiet confidence. You start making decisions based on real data, not just a gut feeling. And in this line of work, having fewer unpleasant surprises is one of the best assets you can have. Ready to trade that financial uncertainty for clarity? At Fynlo, we handle the accounting and bookkeeping so you can focus on what you do best. Let us help you understand the story your numbers are telling. Schedule a free call with us today. You may also like these articles:

I Thought I Was Saving Money—Then the IRS Came Knocking

A Client’s Story: How a “Cheap” Bookkeeper Nearly Cost Him Everything At Fynlo, we work with entrepreneurs every day to build and protect their businesses. Recently, a new client came to us with a story so cautionary, we felt it had to be shared. With his permission, here is the real story of how a single decision—hiring the wrong bookkeeper—led to the collapse of his company, and the powerful lessons every business owner can learn from his experience. Table of Contents How It All Started It started with a simple desire to save a few bucks. As the owner of a growing trucking service, he knew every penny counted. Fuel costs, maintenance, insurance – the overhead was already sky-high. So, when he found a bookkeeper who promised to handle all his finances for a fraction of the price of the more established firms, it felt like a savvy business move. It was a decision he would come to regret more than any other. His name was John, a friendly, soft-spoken man the client found after a quick Google search. John’s website highlighted years of bookkeeping experience, so the client trusted him. He talked a good game, promising to streamline everything, maximize deductions, and keep the IRS and state tax authorities happy. For the first year, everything seemed to be running smoothly. The paperwork was filed, the owner received reports that looked professional, and most importantly, he was saving a significant amount on bookkeeping fees. Money he ploughed back into the business, buying a new rig and taking on more drivers. The business was growing, and he felt like he was finally living the dream he’d worked so hard for. The first crack in the facade was small. A letter from the state tax office about a discrepancy in the company’s fuel tax filings under the International Fuel Tax Agreement (IFTA). John brushed it off as a minor clerical error, assuring the owner he would handle it. Busy managing a fleet that was now running 24/7, the owner took him at his word. Then came another notice—this time from the IRS—about underpaid payroll taxes. Again, John had a plausible explanation. It was the government’s bureaucracy, he said, always getting things mixed up. The Audit That Changed Everything The real trouble began when the company was selected for a random audit by the IRS. The owner wasn’t too worried at first; he believed his operation was clean. When he called John to let him know, for the first time, he heard a flicker of panic in the bookkeeper’s voice. John became evasive, promising to get all the necessary documents in order. That was the last proper conversation they ever had. As the audit date loomed, John became harder and harder to reach. Voicemails went unanswered. Emails bounced back. A visit to his small rented office found it empty, cleared out as if he had vanished into thin air. It was then, the owner described, that a cold, hard knot of dread began to form in the pit of his stomach. With the auditors waiting, he had no choice but to hire a reputable accounting firm to make sense of the mess John had left behind. What they uncovered was a nightmare. John, the “affordable” bookkeeper, had been running a sophisticated scam. He wasn’t filing the IRS or state tax returns properly at all. The professional-looking reports he’d been given were complete fabrications. John had been pocketing a portion of the money intended for tax payments, making only the minimum payments required to avoid immediate red flags. He had misclassified employees, failed to remit payroll taxes correctly, and completely ignored the company’s compliance with IFTA. The audit revealed the full, horrifying extent of the damage. The business owed a staggering amount in back taxes—and that was just the beginning. The penalties and interest were astronomical, a testament to years of neglect and deceit. The business, the dream he had poured his life’s savings and countless sleepless nights into, was insolvent. The cost of getting compliant, of paying the IRS and state penalties, was simply more than the company could bear. The Bitter Decision The choice was brutal: face a mountain of debt and potential legal action, or shut down the company he had built from the ground up. With a heavy heart, he closed the doors of his trucking service. The good people he had employed lost their jobs. The trucks were sold off. His dream had turned to dust. He is now in the process of building a new company from the ashes, this time with our team of trusted, verified professionals. The lessons he learned were paid for at a painfully high price. The Hidden Costs of a “Cheap” Bookkeeper Our client’s story is a cautionary tale for every small business owner. The allure of saving money on professional services is strong, but the risks are profound. A bad bookkeeper can do more than just make a few errors; they can systematically destroy a business from the inside out. These are the crucial red flags he now advises every business owner to recognize: Protecting Your Business Before you entrust your finances to anyone, you must do your due diligence. Here’s what our client is doing differently with his new venture—and what we advise for all business owners: Ready to Safeguard Your Finances? Don’t wait until the IRS is at your door to get serious about your bookkeeping. At Fynlo, we combine expert accountants—many with backgrounds at top firms like Grant Thornton, BDO, and Baker Tilly—with cutting-edge software to ensure your books are accurate, compliant, and stress-free. Schedule your free call today and pave the way for a confident, mistake-free financial future. You may also like these articles:

15 Highest Paying Freelance Jobs

I was chatting with an ex-FAANG engineer at a co-working space the other day. He’d left Big Tech in 2019 to freelance full-time. I assumed he’d traded a cushy salary for a bit more freedom, but I was wrong. He’s making more money now and still ducks out for a Wednesday surf session whenever the waves are good. Stories like his aren’t rare anymore. The freelance economy has matured, and companies now view top contractors as mission-critical talent, not budget line items. According to Upwork’s Study, 38% of the U.S. workforce (about 64 million Americans) freelanced in 2023, and specialized roles regularly command triple-digit hourly rates. Below are 15 freelance careers that pay exceptionally well and give you the freedom to spend afternoons with family, jet off on a moment’s notice, catch the perfect swell—whatever your version of freedom looks like. Note: Because Sales Funnel Copywriting and Voice-Over services aren’t billed by the hour, they’ve been excluded from this chart. 1. Blockchain (Web3) Developer Blockchain is no longer a buzzword; it underpins billions of dollars’ worth of transactions in finance, supply chain, and even gaming. Even though the crypto market has seen its share of volatility and downturns, demand for skilled blockchain engineers remains strong, because companies still need private ledgers, supply‐chain tracking, and secure tokenization. From writing tamper‐proof smart contracts to auditing DeFi protocols for seven‐figure exploits, top‐tier engineers sit at the crossroads of money and math, so companies happily pay to keep them on speed-dial. Typical Rate: $50 – $150/hr Key Skill: Solidity, Ethereum, Hyperledger Fabric, cryptography, distributed systems 2. AI / Machine-Learning Consultant AI is red-hot, and every investor is hunting for the next breakthrough, so the prospects for skilled ML consultants are bright. Enterprises are scrambling to move from “AI pilot” to real ROI, but pre-trained models still need custom data, guardrails, and cost controls. Freelance ML pros step in to fine-tune LLMs, build anomaly-detection pipelines, and translate geek-speak into board-room slides. When a single algorithm tweak can save or earn millions, these specialists name their price. Typical Rate: $120 – $300/hr Key Skill: Python + PyTorch, TensorFlow, prompt engineering, data modeling 3. Cloud Architect/Engineer One mis-tagged S3 bucket can leak data, and one mis-sized cluster can torch $10K in a weekend. Large companies know that poor cloud setup risks both security breaches and massive unexpected bills, so they take cloud architecture very seriously. Architects who tame AWS, Azure, or GCP keep uptime high and costs low, guiding organizations through migrations and DevOps automation. Their invoices cost far less than the cloud horror stories they prevent. Typical Rate: $80 – $180/hr Key Skill: AWS/Azure/GCP certifications, Terraform, network security, virtualization 4. Cybersecurity Specialist A single breach now averages $4.88 M (IBM 2024). High-profile incidents like the Equifax breach and Colonial Pipeline hack have shuttered operations overnight. Ethical hackers and compliance experts harden networks, run red-team drills, and navigate audits—“Pay me five figures or pay ransomware double” clients wisely choose the former. Typical Rate: $80 – $160/hr Key Skill: Pen-testing toolkits, zero-trust architecture 5. AR/VR (XR) Developer Forget metaverse hype—healthcare training sims, virtual showrooms, and mixed-reality field guides are already mainstream. Companies without in-house Unity or Unreal talent tap freelancers to prototype fast and wow investors. From virtual home staging that helps real estate agents close deals more quickly to interactive factory maintenance guides that reduce downtime, XR applications drive real-world results. As hardware becomes more affordable and headsets more comfortable, demand for skilled AR/VR developers is only set to skyrocket. Typical Rate: $60 – $150/hr Key Skill: Unity-C# or Unreal C++/Blueprints, spatial UX 6. UX/UI Designer A clunky onboarding screen can bump churn 20%, while a friction-free flow can turn trial users into loyal customers. Senior designers create intuitive, user-friendly, and aesthetically pleasing digital interfaces—whether websites or apps—that guide users seamlessly through key actions. By blending psychology, aesthetics, and A/B testing data, they optimize every step of the user journey to maximize satisfaction and conversion rates. Their work has a direct impact on product adoption and revenue, making each pixel they design worth every dollar. Typical Rate: $40 – $100/hr Key Skill: Wireframing, prototyping (Figma, Sketch), user research, usability testing 7. Digital Marketing Strategist Anyone can boost a post; few can scale ad spend from $10K to $1 M per month while maintaining a 4× return on ad spend (ROAS). These strategists oversee every aspect of performance campaigns—from high-volume A/B creative testing to sophisticated attribution modeling that tracks exactly which ad led to a sale—and they pivot on a dime when platform algorithms change. By analyzing granular metrics and optimizing audience segments, they ensure every dollar of your marketing budget translates into measurable revenue and sustainable growth. Typical Rate: $50 – $100/hr Key Skill: Google Ads & Meta Blueprint certs, analytics (GA4), audience strategy 8. Sales Funnel Copywriter Words that sell are worth their weight in gold. Conversion copywriters and funnel architects craft the headlines, email sequences, and upsell offers that transform casual browsers into loyal buyers. They begin by conducting deep customer research—interviewing your ideal audience, analyzing what genuinely resonates, and then weaving persuasive prose that addresses pain points and triggers emotional responses. By layering strategic call-to-action placements and A/B testing different messaging, these professionals can triple conversion rates. When a $50K product launch balloons to $150K because of a winning sales page, clients happily share the upside—making stellar copywriting a high-stakes investment. Typical Rate: $0.25 – $1.00/word or $3K–$10K/funnel Key Skill: Persuasive copywriting, sales psychology, CRO techniques 9. Senior Video Editor / Motion Graphics Artist Short-form video was reported as having the highest ROI of any social media marketing strategy in 2024. Senior editors and motion graphics artists take raw footage and elevate it—splicing together narrative beats, applying color grading, and layering dynamic animations. Their work keeps viewers glued to screens: a product teaser with eye-popping transitions, a brand story punctuated by kinetic typography, or a tutorial that feels more cinematic than instructional. Because social platforms serve up short attention spans, these creators blend

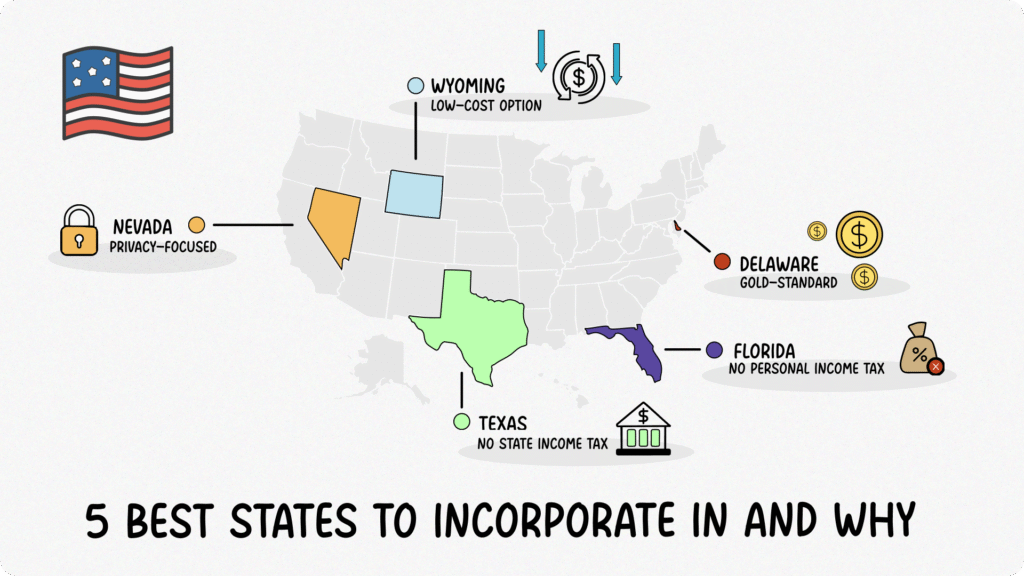

5 Best States to Incorporate In and Why

When I started my first small business, I remember staring at a blank screen, Googling “where should I incorporate?” I found conflicting advice, fees that seemed to change overnight, and legal jargon that made my head spin. Over time—after a few “oops” moments and some late-night research—I narrowed it down to five states that consistently offer the best mix of low costs, solid legal protections, and friendly environments for entrepreneurs. Here’s what I’ve learned, with real numbers (as of 2025) and a few personal notes about why these states stand out. Table of Contents Delaware: The Gold Standard for Big (and Small) Businesses “People joke that Delaware exists just so corporations can incorporate there—and it almost feels that way when you see how slick their system is.” Why Delaware? Fees (2025): If you budget about $540/year (minimum franchise tax + report), you’re covered. And if your business grows—say, you issue more shares or have a high par-value capital structure—you might pay more, but startups typically stay at the minimum. Personal note: My first LLC wasn’t in Delaware—it was in my home state. But after attending a startup accelerator and hearing investors talk about “Delaware C-Corp, please,” I re-formed there. I still recall breathing a sigh of relief when I realized investors are so comfortable with Delaware entities that legal due diligence becomes that much smoother. Wyoming: The Friendly, Low-Cost Option for Small Businesses “Think of Wyoming as the underdog—no one talks about it as much as Delaware, but it quietly checks all the right boxes for a lean, mean small-business machine.” Why Wyoming? Personal note: When I was a freelancer, I formed a single-member Wyoming LLC just because the yearly cost was so low. It felt thrilling to pay only $160 total each year and know my personal assets had a legal buffer. Nevada: Privacy-Focused with No Corporate Income Tax “Nevada is like Wyoming’s more opulent cousin—privacy protections, no state income tax, and a reputation as the ‘Florida of the West’ for tax benefits.” Why Nevada? Fees (2025): In total, expect around $875 in year one (incorporation + list + license). Subsequent years are $650 (license $500 + list $150). I know that sounds steeper than Wyoming, but if privacy and zero state tax on profits matter, many entrepreneurs find Nevada worth the up-front costs. Personal note: A colleague once told me, “If you live in California but want to keep your taxes honest, move to Nevada for your mental health.” He wasn’t wrong—no state income tax means one fewer headache at tax time. Texas: No State Income Tax + Seller’s Market for Services “Texas is booming—no state income tax, a thriving entrepreneurial scene, and a sense of ‘everything’s bigger in Texas,’ including opportunities.” Why Texas? Personal note: I once thought I’d set up shop in California, but I cringed at that 13.3% top-bracket personal rate on top of corporate taxes. Texas felt like a breath of fresh air—zero state income tax, and Austin’s startup vibe makes you feel like anything’s possible. Florida: No Personal Income Tax + Moderate Corporate Tax “Florida is that friend who loves to chill in flip-flops but still knows how to hustle—no personal income tax, solid consumer market, and a growing tech ecosystem.” Why Florida? Personal note: I spent a summer in Miami Beach brainstorming a business plan on the sand. The idea of paying zero state income tax gave me the energy to work late nights—and if you’ve ever tried running spreadsheets in 90-degree heat, trust me, you’ll appreciate anything that saves you a percentage point of tax. Things to Consider When Choosing a State TL;DR A quick overview of the five best states to incorporate in, plus why they might be a fit for you: State Formation Fee Annual Cost Corporate Tax Personal Tax Key Benefits Delaware $89 (C-Corp) $400 franchise tax + $50 report None on C-Corp profits None on pass-through – Chancery Court– Flexible corporate laws– Investor-friendly Wyoming $100 (LLC) $60 annual report None None – Lowest fees– Strong privacy & asset protection– No state income tax Nevada $75 (C-Corp) $500 business license + $150 list None None – Robust privacy– No corporate/personal income tax– Business court by 2026 Texas $300 (Corp) Exempt under $1.23M revenue; otherwise 0.375%–0.75% margin tax 0.375%–0.75% (varies) None – No personal income tax– Large business ecosystem– Franchise tax exemption under $1.23M Florida $70 (C-Corp) $150 annual report 5.5% None – No personal income tax– Growing tech hubs– Moderate corporate tax Final Thoughts There’s no one-size-fits-all “best state”—it really depends on your budget, growth plans, and tolerance for paperwork. When I first started, the difference between $60/year (Wyoming) and $540/year (Delaware) felt huge. But as my business matured and I talked to investors, it became clear that Delaware could save me weeks of legal back-and-forth. Meanwhile, friends who run lean e-commerce stores from home still swear by their $160/year Wyoming LLCs. In the end, pick the state that aligns with your current priorities: cost, privacy, investor confidence, or community. And remember, you can always form in one state and later register as a foreign entity in another (it’s called “qualifying” to do business in your home state). That’s exactly what many growth-stage startups do: incorporate in Delaware, then register in their home state so they can open a bank account, hire W-2 employees, and sign leases without legal headaches. I hope this guide helps you sleep a little easier as you choose your business’s “home.” Wherever you decide to incorporate, know that every entrepreneur—myself included— started exactly where you are right now: staring at a blank filing form, hoping they made the right choice. Need Help with Your Accounting? At Fynlo, we know every state has its own quirks—whether it’s Delaware’s Chancery Court, Wyoming’s low fees, Nevada’s privacy rules, Texas’s franchise tax, or Florida’s corporate rate. Our expert team can handle your bookkeeping, annual filings, and state-specific tax planning no matter where you incorporate. Schedule a call today, and let us make sure your business stays

The Fynlo Guarantee: Accurate, On-Time, and Stress-Free Accounting

Running a freelance gig or small business means juggling dozens of responsibilities, from marketing and client work to operations and finances. At Fynlo, we take accounting off your plate with our Fynlo Guarantee: every client receives bookkeeping and tax services that are Accurate, delivered On-Time, and completely Stress-Free. 1. Accurate Records—Every Time Even minor mistakes can lead to penalties or missed deductions. Accuracy is non-negotiable: Result: Financial statements you can trust, helping you maximize deductions and maintain compliance. 2. On-Time Delivery—And Smarter Decisions Through Clarity Late reports can derail cash-flow plans, loan applications, or investor pitches. With Fynlo: Result: You receive up-to-date financials exactly when expected, plus the strategic clarity to guide your next move. 3. Stress-Free Experience—Focus on What Matters Worrying about bookkeeping drains time and energy. Fynlo makes accounting seamless: Result: Zero late-night “where did that charge go?” moments. Instead, you stay focused on clients and growth. Meet the Team Behind the Guarantee Our combined expertise, backed by best-in-class technology, ensures your accounting is both personalized and scalable. How to Get Started Unlock peace of mind and a clear financial roadmap. Experience Accurate, On-Time, and Stress-Free accounting with Fynlo. Book your free discovery call today.