5 High-Value Service Roles Shaping the AI Economy

It feels like every time we check the news, there is a new story about AI coming for everyone’s job. While those headlines can be a bit overwhelming, the real story is actually much more positive for small business owners. AI isn’t just about robots replacing people. It is opening up entirely new ways for us to work as specialists. According to McKinsey’s report, generative AI could add up to $4.4 trillion to the global economy every year. A huge chunk of that value isn’t going to the tech giants. Instead, it is going to specialized service providers who know how to make this technology work for real-world businesses. We are seeing a shift where value is moving away from basic data entry and toward the “brains” behind the systems. For entrepreneurs and small firms, this is the perfect time to pivot into niches that didn’t even have a name a few years ago. Here are five of the fastest-growing roles emerging in this new economy. 1. The AI Workflow Automation Architect Gartner predicts that by 2026, over 80% of enterprises will be using generative AI to automate their workflows. That sounds great on paper, but in reality, there is a massive “integration gap.” Most businesses have plenty of tools, but they are often stuck in a tangle of software where nothing talks to each other correctly. Automation Architects are the people who fix this mess. They don’t just use AI; they build autonomous systems that handle the boring parts of a job. Imagine a setup where a new lead arrives and the AI automatically researches the prospect’s background, drafts a personalized intro, and updates your records. This happens in the background while the business owner is actually focused on the creative work they love. Because this work is so results-driven (you are literally giving a founder their time back), these architects can command premium fees. They usually run very lean operations and rely on the same automation they sell. For them, manual bookkeeping isn’t just a chore; it is a total contradiction to their business model. 2. The Fractional Chief AI Officer (CAIO) Every small business owner knows they should be using AI, but most are simply too busy running their daily operations to figure it out. They can’t afford a full-time executive with a massive salary, yet they are worried about falling behind. The World Economic Forum’s Future of Jobs Report 2025 actually highlights that while AI will displace some roles, it is expected to create 170 million new ones globally, leading to a net gain of 78 million jobs by 2030. Many of these are high-level, specialized roles that support business transformation. A Fractional CAIO is essentially a “part-time expert for hire.” They might jump in for a few hours a month to audit a company’s processes and provide a clear roadmap. They help the team decide which tools are worth the investment and which are just hype. It is a high-level role that lets the CEO focus on growth while the CAIO handles the tech strategy. Managing a portfolio of high-value clients like this requires extreme organization. When you are juggling five different companies, you cannot afford a messy back office. These consultants need a clear, professional view of their cash flow across all their retainers so they can stay focused on the strategy their clients are paying for. 3. The Niche Data Fine-Tuner General AI can be a bit of a “jack-of-all-trades, master of none.” A law firm doesn’t need a chatbot that knows how to write a poem; they need a system that understands specific regional real estate laws. This has created a boom for Fine-Tuners. These are consultants who take generic models and “teach” them using industry-specific data. This is meticulous, high-value work. You might spend weeks cleaning up a client’s proprietary contracts or internal logs to ensure the AI becomes an expert in that one specific field. This role bridges the gap between raw data and actually useful intelligence. Since these projects often involve heavy technical costs and irregular billing, such as a large deposit followed by a success fee, tracking project profitability is vital. If you don’t keep a close eye on your expenses as they happen, those big margins can disappear faster than you might think. 4. The “Hallucination Hunter” (AI Risk Auditor) With new regulations like the EU AI Act rolling out, companies are now legally responsible for what their AI says. If a chatbot gives bad financial advice or leaks private data, the business is on the hook. AI Auditors are the “human safety net.” They stress-test AI systems to find bias, errors, or privacy leaks before they go live. It is a role built entirely on trust and accuracy. In high-stakes worlds like healthcare or finance, these auditors are the reason companies feel safe hitting “publish” on a new tool. If your entire brand is built on being a rigorous auditor, your own internal records have to be spotless. These professionals need an audit-ready paper trail for their own finances. Using tools that automate record-keeping doesn’t just save them time; it ensures they are practicing the same level of accuracy they promise their clients. 5. The Human-Centric Experience Designer We’ve all had that frustrating experience of getting stuck in a chatbot loop where you just want to talk to a real person. Businesses are starting to realize that total automation often leads to zero customer satisfaction. Gartner found that 64% of customers still want a human touch for complex problems. Experience Designers are the bridge. They design the “hand-off,” which is the exact moment where the AI steps back and a human steps in. They ensure that automation feels like a help rather than a barrier. You could think of them as the Empathy Engineers of the tech world. These designers often work with a revolving door of creative contractors like writers, developers, and researchers. That means a lot of moving parts in their bank account. Keeping those project budgets and contractor payments organized is the only way they can stay in their “creative zone” without getting bogged down in spreadsheets. Future-Proofing Your Back Office The roles we are seeing emerge all have one thing in common: they are lean, fast-moving, and highly specialized. These entrepreneurs are

Future-Proof Your Business: Essential New Business Trends for 2026

Stepping into 2026 feels like a strategic reset. For those of us running businesses, the focus has shifted toward building systems that are resilient enough to let us lead with vision instead of just reacting to the latest fire in our inbox. We are looking for Operational Intelligence: a state of flow where the back office supports growth rather than hindering it. The numbers suggest a massive shift is underway. With US e-commerce revenue expected to climb by nearly $500 billion by 2029, the opportunities are vast, but the complexity has followed suit. While 80% of organizations agree that inadequate or outdated technology is holding back innovation, success requires looking at how these investments empower our teams and protect our mental bandwidth. This guide explores five essential shifts in technology, workplace culture, and consumer behavior that are defining the market this year. By understanding these trends, you can transition from manual labor to a model where your business is as durable as the products or services it sells. In this article 1. Synergistic AI Collaboration We have officially moved past the experimentation phase of AI. It is no longer a shiny new object to be feared or idolized; it has become a fundamental utility. By the end of 2026, most successful businesses will have moved away from basic chatbots toward true Workflow Orchestration. This involves using AI for the heavy lifting of data processing and research while a human partner provides the final 10% of nuance and accountability. Consider the common struggle of market research. A real estate agency might use a tool like Clay to scan thousands of property listings for very specific investment criteria. This technology allows them to instantly cross-reference public tax records, zoning changes, and owner locations to find distressed opportunities that basic filters often miss. In the past, a founder might have spent ten hours a week on this. Now, the AI provides a refined shortlist. An expert strategist then reviews that list to ensure the fit feels right before any outreach happens. This human-in-the-loop model is why McKinsey suggests that AI could technically automate about 57% of work hours. The goal is to move away from manual labor toward a model where humans act as the ultimate quality control for intelligent systems. 2. Modern Skills-Based Hiring The way we build our teams is undergoing its most significant transformation in decades. The old debate over office space has matured into a more sophisticated discussion about results. We are seeing the rise of the Results-Only model, where talent is measured by what they can actually produce rather than where they went to school or how long they sit at a desk. Skills-based hiring is becoming the new gold standard. 90% of companies now report that they make much better hires when they prioritize specific, verifiable competencies over traditional four-year degrees. Technology has made this easier to manage for businesses of all sizes. Platforms like Deel or Gusto allow us to handle global payroll for hybrid teams, while tools like Loom or Slack facilitate high-quality communication that does not require everyone to be in the same time zone. We are seeing law firms and tech giants move away from traditional requirements to find specialized talent that can actually move the needle on day one. 3. Strategic Circular Operations In 2026, sustainability has moved from the marketing department into the heart of operations. The Circular Economy model (where we design waste out of our systems and keep materials in use longer) is now a competitive requirement. Consumers are increasingly skeptical of greenwashing and are looking for brands that offer radical transparency. Research shows that 81% of consumers now trust brands that are open about their operations and even their challenges. Some businesses use Notion to build public-facing transparency portals, while others use Watershed to track their actual environmental impact. This transparency builds a layer of trust that traditional advertising simply cannot buy. Beyond the ethical benefits, this trend is a survival tactic. Circularity protects you against geopolitical shocks in the supply chain. When your business model includes refurbishment or reuse, you become far less dependent on the volatile global markets for raw materials. It is about building a business that is as durable as the products it sells. 4. Cultivating Gen Z Loyalty Gen Z and Alpha consumers are rewriting the rules of brand loyalty. They expect a relationship that feels helpful and human-led rather than purely algorithmic. For these generations, community is the primary currency. The financial impact of this connection is significant, as some organizations have found that active community members generate five times more revenue compared to those who are less engaged. The tools for this have become incredibly accessible. Many brands use Klaviyo for hyper-personalized, behavior-based emails that feel like a conversation rather than a broadcast. Others are moving their most loyal fans into owned communities on platforms like Circle or Substack. With attention spans now averaging just over eight seconds, the format matters as much as the message. Short-form, vertical video is now the primary way three-quarters of all video content is consumed. It is a fast-paced environment, but those who lead with authenticity and provide value quickly are seeing the highest conversion rates. 5. Scaling through Seamless Integration Moving toward these trends is rarely a straight line. It is easy to feel a sense of app fatigue when you have too many tools that do not talk to each other. This often results in technical debt, where the founder ends up spending more time managing software than leading people. The way to handle this is by adopting an integration-first policy. We should only bring in tools that have a robust way to sync with our existing systems, usually through a platform like Zapier. This keeps our data in one place and prevents the scattered feeling of having five different logins for one project. Another common friction point is the quality gap that comes with over-automation. When we rely too much on AI, our brand can start to feel cold or generic. The solution is to build a human guardrail. For any customer-facing output or high-stakes financial task, there should be a rule that an expert performs a final sanity check. Technology provides the speed, but people provide the

10 Absurdly Clever Tax Deductions That Got Approved

The IRS has seen some pretty wild tax deduction attempts over the years, and some of them actually worked! Check out our list of the 10 craziest tax deductions you have ever heard of! And if you’re a freelancer, don’t miss our other blog: “The Freelancer’s Guide to Tax Deductions.” Table of Contents 10 Wild Tax Deductions Legit Deduction or Wishful Thinking? Let’s Find Out! Now that you’ve seen some of the most surprising tax deductions that actually got approved, it’s time to test your own deduction savvy. Below are a few expenses. For each, one scenario is deductible, and the other isn’t. Can you determine which is which? Cat FoodScenario 1: Junkyard owner buys food for rat-patrolling felinesScenario 2: Snack for a pet cat Guard DogScenario 1: Business guard dog expensesScenario 2: Pet dog expenses TutorsScenario 1: Specialized tutor for a child with a diagnosed learning disability, as recommended by their doctorScenario 2: Reading tutor for general academic improvement African SafariScenario 1: Dairy business owners on a wild animal-focused tripScenario 2: Family vacation Private AirplaneScenario 1: Condo owners flying themselves to check on their rental propertyScenario 2: Vegas private jet ride Personal TrainerScenario 1: Trainer for a professional athleteScenario 2: Gym-goer getting ready for summer Clown CostumesScenario 1: Professional clown costumeScenario 2: Halloween costume Sun ProtectionScenario 1: Sunscreen for carpenters/gardenersScenario 2: Sunscreen for beach trip Absolutely right! Scenario 1 is deductible, but Scenario 2 isn’t. Many of these cases are based on real stories, proving that the same expense can be approved or denied depending on the context and whether it meets the IRS rule of ‘ordinary and necessary.’ “Ordinary” means it’s common in your line of work, and “necessary” means it’s helpful and appropriate for your business—not just something you want. Tax deductions come with rules. For example, guard dog expenses are only deductible for the time the dog is actually working, and medical deductions are subject to limitations like the 7.5% AGI rule. Because tax laws are complex, it’s always best to consult a professional when in doubt. Itemized Deduction vs. Standard Deduction These unusual (and sometimes surprisingly successful) deductions highlight the importance of understanding the rules and keeping meticulous records. Navigating the tax code can be tricky, and knowing what qualifies as a legitimate deduction is crucial for any taxpayer. This is especially crucial when deciding whether to itemize or take the standard deduction. The TCJA changed the tax landscape, making the standard deduction the better option for most taxpayers. But if you have significant deductible expenses, itemizing can still work in your favor. The good news? The old deduction limit is gone, so you can claim the full amount if eligible. That said, with fewer people itemizing, the IRS is paying closer attention to those who do. If you’re planning to itemize, make sure your records are solid. Looking to keep your records organized and ready for tax filing? Schedule a call with our experts today for bookkeeping support.

5 Fastest Growing Ecommerce Companies in 2026

Americans now spend more on e-commerce than the GDP of Denmark – and these 5 innovative companies are cashing in. Forget Amazon clones – these disruptors are creating entirely new ways to shop. 1. Whatnot – Livestream Shopping Marketplace Imagine scrolling through TikTok, but instead of just watching, you can instantly buy what you see—that’s Whatnot. This platform brings the thrill of live auctions to your phone, where sellers host real-time video streams to showcase everything from rare Pokémon cards to sneakers, vintage toys, and even luxury handbags. Unlike traditional marketplaces (eBay, Facebook Marketplace), Whatnot makes shopping entertaining. Sellers hype up their products like game show hosts, buyers chat and bid in real time, and rare items can sell for thousands in minutes. It’s QVC meets social media, and it’s exploding. A rare Pokémon card was sold for $250,000 in a Whatnot auction last year—more than some houses! Key Takeaway: 2. ShopMy – Creator-Affiliate Commerce Platform Ever click an Instagram link to buy a product? There’s a good chance ShopMy powered it. This platform helps influencers monetize their audiences by turning their posts into shoppable storefronts. Brands like Nike, Lululemon, and Sephora use ShopMy to track which influencers actually drive sales (not just likes). Meanwhile, creators get commission on every purchase—without needing a clunky Shopify store. Key Takeaway: 3. Little Spoon – Direct-to-Consumer Baby and Kids’ Food Parents are tired of processed baby food filled with preservatives. Little Spoon delivers fresh, organic meals for babies and toddlers—shipped cold, ready to eat. Their “Plates” line (for toddlers) includes meals like turkey meatballs and quinoa bowls, while their baby blends use ingredients like avocado and kale. They even offer vitamins and probiotics—making them a one-stop shop for health-conscious parents. Key Takeaway: 4. Market Wagon – Online Farmers Market Farmers markets are amazing—but who has time to go every weekend? Market Wagon brings local farms to your doorstep. You can order grass-fed beef, organic eggs, artisan cheese, and fresh-picked produce—all from small farmers in your area. They handle delivery, so you get farm-fresh food without the hassle. Key Takeaway: 5. The Woobles – DIY Crochet Kits Crochet is having a major moment on TikTok—but most beginners quit because it’s too hard. The Woobles fixes that with foolproof kits that include pre-started yarn, step-by-step videos, and adorable patterns (like penguins, dinosaurs, and even a tiny Starbucks cup). Their secret is “Easy Peasy Yarn”—a special material that doesn’t unravel, so newbies can’t mess up. Key Takeaway: What These Companies Teach Us These companies prove that niches win. Instead of trying to be the next Amazon, they’re: As ecommerce continues to evolve, focusing on specific needs and creating engaging experiences will be key to standing out in the crowded online marketplace. Note: All data and figures are based on available information as of 2025. For the most current statistics and company details, please refer to official company reports and reputable news sources.

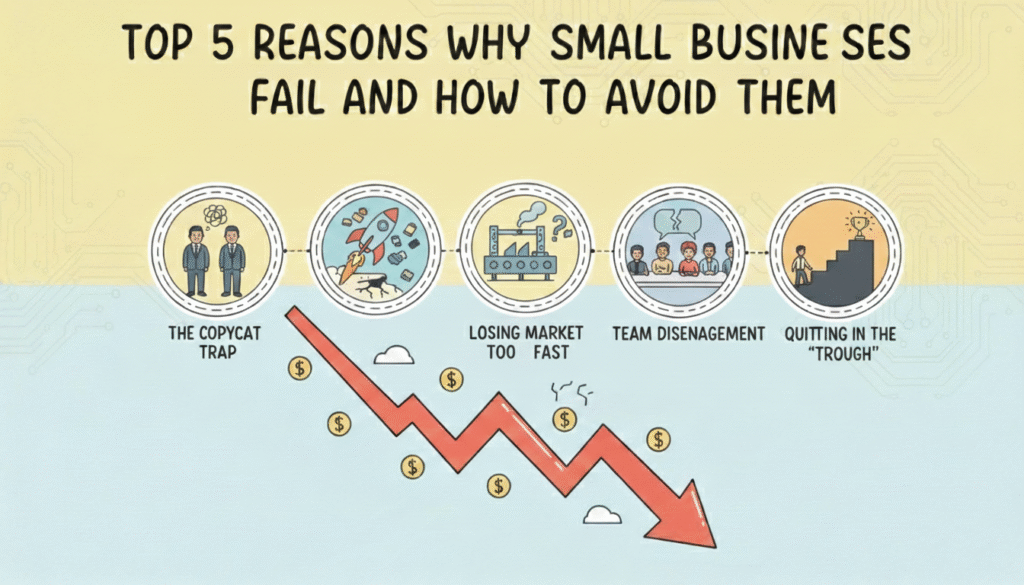

Top 5 Reasons Why Small Businesses Fail and How to Avoid Them

Starting a business is easily one of the most rewarding journeys you’ll ever embark on. There’s nothing quite like the rush of that first sale or the pride of seeing your logo on a real office door. Yet, for all the excitement, it’s also incredibly lonely and, at times, brutal. As we look toward 2026, the entrepreneurial spirit is louder than ever, yet the quiet reality remains: many small businesses struggle to stay afloat. According to 2024 data from the U.S. Bureau of Labor Statistics, nearly 50% of businesses fail within their first five years. We don’t believe failure is a foregone conclusion. Usually, it isn’t one giant catastrophe that sinks the ship; it’s a series of small, quiet cracks in the hull that no one noticed or wanted to see. In our experience watching what separates the survivors from the statistics, success often comes down to navigating a few specific, hidden hurdles. Here are the five real reasons businesses stall, and how you can navigate around them to build something that lasts. In this article 1. The Copycat Trap It starts with a seductive, familiar thought: “They’re making a killing, and I know I can do it better at a lower price.” It’s a common mindset that feels like a shortcut to success. You see a local leader or a big industry player and try to mirror their every move while undercutting their costs. This is the “Copycat Model,” and while it feels like a safe bet, it’s actually a trap. When you copy, you’re competing against someone who has more history, deeper pockets, and an established reputation. If your only way to win is to be “slightly cheaper,” you aren’t building a business; you’re operating on razor-thin margins that leave no room for error or future growth. When your only edge is price, any increase in your costs or a counter-move from a larger competitor can instantly wipe out your remaining profit. As Peter Thiel famously wrote in Zero to One: “The next Bill Gates will not build an operating system. The next Larry Page or Sergey Brin won’t make a search engine.” If you aren’t bringing something uniquely you to the table, you’re just holding a spot until someone with more capital decides to take it. You don’t need to reinvent the wheel, but you do need to give people a reason to choose yours. How to stay ahead: 2. Scaling Too Fast We’ve all felt that “first milestone” adrenaline. You’ve got your first big clients, you’ve hired a Virtual Assistant, and for the first time, the dream feels real. This can be the danger zone. It’s when founders get impatient and start pouring money into massive hiring sprees or new markets before their core engine is actually stable. The numbers are staggering: 74% of high-growth startups fail because they scaled prematurely, according to the Startup Genome Report. Take the story of Bench, the bookkeeping giant. They raised over $100 million, had a massive team, and were the darlings of the tech world. But despite the funding and the hype, the company eventually had to shut down its core operations. They scaled their burn rate before they mastered their efficiency. Scaling a broken process doesn’t make you bigger; it just makes your mistakes louder and much more expensive. How to stay ahead: 3. Losing Market Flexibility There is a thin, blurry line between being “persistent” and being “stubborn.” We often fall in love with our original vision, treating it like a sacred text rather than a living document. Take Kodak as a prime example. In 1975, one of their own engineers invented the first digital camera. But the leadership was so protective of their film business that they buried the tech. They clung to the past while the world moved on. This reluctance eventually led the once-dominant giant to file for bankruptcy in 2012, which serves as a powerful lesson that past success is no guarantee of future survival. Today, failing to pivot is just as risky. According to a report by CB Insights, 42% of startups fail because there is simply no market need, often because the founders were so busy building a “perfect” product that they forgot to check if anyone actually wanted it. If you stop listening to your customers because you’re too busy “staying true to your vision,” it’s easy for the path forward to get a bit blurry. How to stay ahead: 4. Team Disengagement A business isn’t a machine; it’s a collection of people. If the people lose their spark, the engine stalls. Most of us recognize the signs: the “silent office” where everyone is just going through the motions. Gallup’s research shows that engaged teams are 21% more profitable, yet so many founders treat culture as an afterthought. High turnover isn’t just an HR headache; it’s a massive financial leak. It costs an average of $6,000 to replace a single employee, but the loss of trust and institutional knowledge is even higher. When your team feels like they are just “clocking in,” they won’t have your back when things get difficult. How to stay ahead: 5. Quitting in the “Trough” Every entrepreneur eventually finds themselves in the “Trough of Sorrow.” It’s that long, quiet stretch after the initial excitement has worn off, but the big results haven’t arrived yet. It’s the 2 AM nights spent wondering if you’ve made a huge mistake. 53% of founders reported feeling burned out. That exhaustion often leads to “Premature Capitulation”—closing a perfectly healthy business simply because the founder is spent. There’s a nuance here: you should be flexible with your method (as we saw in Point 3), but you must be relentless with your mission. Success usually happens right after you’ve considered walking away. Thomas Edison said it best: “Many of life’s failures are people who did not realize how close they were to success when they gave up.” How to stay ahead: Building for the Long Haul Professionalism doesn’t have to cost money, but looking amateur will cost you opportunities. As your workload grows, tools that automate invoicing, reminders, and tracking can make a noticeable difference. Exploring a dedicated invoicing platform like Fynlo is a simple next step if you want fewer follow-ups and more predictable payments. Book a free demo to see how Fynlo might fit into your day-to-day.

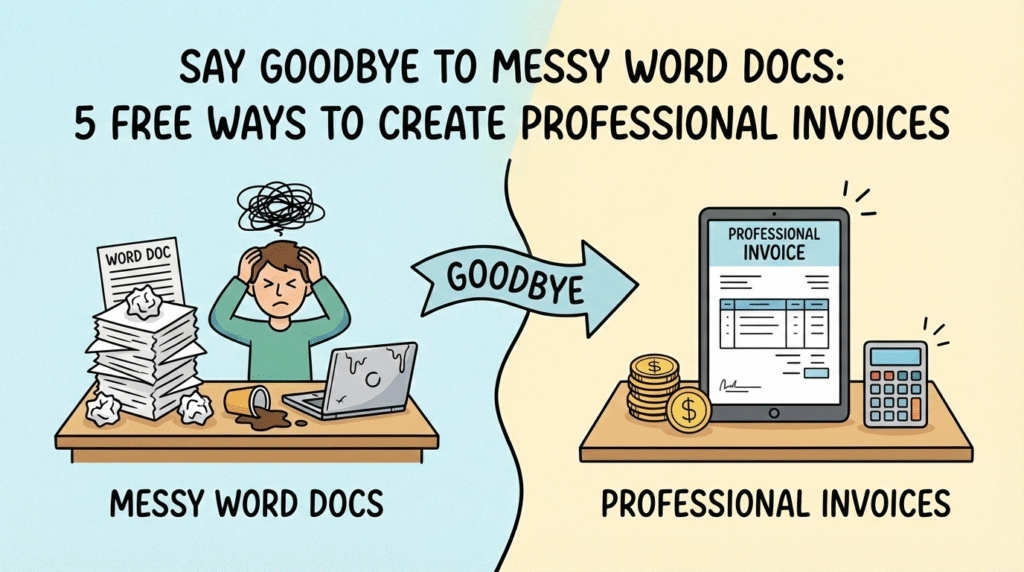

Say Goodbye to Messy Word Docs: 5 Free Ways to Create Professional Invoices

You’ve just exported the final file, closed the 17 browser tabs you’ve had open for a week, and hit “Send” on the final deliverable. You lean back in your chair, take a deep breath, and feel the weight of the project lift off your shoulders. But before you can fully celebrate, there is one last administrative hurdle: asking for the money. For many of us, this part feels awkward. We rush through it, typing a few lines into a document and hoping it looks “official enough.” But the reality is, your invoice is the final handshake of your project. It’s the last impression you leave. Sending a polished, branded invoice does more than just look good—it changes the power dynamic. Data suggests that you are 3x more likely to get paid simply by adding a company logo to your invoice. Psychologically, a sharp invoice signals, “I take my business seriously, and I expect you to do the same.” Here are 5 completely free ways to upgrade your invoicing today, ranked from the simplest quick-fix to fully automated systems. In this article 1. Free Online Invoice Generators Sometimes you just need to send one invoice, right now. You don’t want to sign up for a new platform or remember another password; you just need a PDF that doesn’t look like it was made in 1999. Quick Tip: Look for generators that allow you to change the currency symbol if you are working with international clients. Sites like Invoice Generator or Shopify are great places to start. 2. Google Docs & Sheets Templates If you are just starting out and want total control over every pixel, the Google Workspace gallery is likely your best friend. It is accessible, cloud-based, and you likely already use it for your actual work. Quick Tip: Always export as a PDF before sending. Sending an editable Google Doc looks unprofessional and allows clients to accidentally (or intentionally) change the figures. 3. Canva Templates Who says invoices have to be boring spreadsheets? If you are in a creative field—graphic design, social media management, or photography—your invoice is another piece of your portfolio. It should look as good as your work. Quick Tip: Create a “Master Template” in Canva so you don’t have to re-design it every time. Just duplicate the page and update the line items. 4. Stripe or PayPal Invoicing If your priority is getting money into your bank account fast, you might want to skip the PDF attachment entirely and send a digital invoice directly through your payment processor. Quick Tip: Enable “recurring invoices” if you have clients on a monthly retainer. The system will bill them automatically without you lifting a finger. 5. Dedicated Invoicing Software (Wave, Zoho, Fynlo) Eventually, manual templates and fees become a bottleneck. If you are sending more than 5 invoices a month, you need a system that automates your entire billing workflow—remembering your clients, numbering your invoices, and chasing payments for you. Quick Tip: With Fynlo’s Forever Free plan, you get a professional dashboard that tracks invoice views. This means a client can never use the excuse “I didn’t get the email” again, because you’ll know exactly when they opened it. Make Getting Paid the Easy Part Professionalism doesn’t have to cost money, but looking amateur will cost you opportunities. As your workload grows, tools that automate invoicing, reminders, and tracking can make a noticeable difference. Exploring a dedicated invoicing platform like Fynlo is a simple next step if you want fewer follow-ups and more predictable payments. Book a free demo to see how Fynlo might fit into your day-to-day.

The 5 Biggest Accounting Trends That Will Define Business Survival in 2026

If you feel like the rules of doing business are changing faster than you can keep up, you aren’t alone. For freelancers and small business owners, 2026 is shaping up to be a turning point. We are finally moving away from the era of “I’ll get to that paperwork later” and into a world where automation is the standard and compliance is non-negotiable. We have dug into the latest government budgets and global industry reports to bring you the five biggest shifts hitting the accounting world in 2026. Here is what you need to know to stay ahead. In this article 1. Mandatory E-Invoicing Is Going Global First, let’s clear up a common misconception: E-invoicing is not just emailing a PDF. When you send a PDF, it is essentially a digital piece of paper—a human still has to open it, read it, and type the numbers into their system. True e-invoicing is data, not a document. It involves sending structured files (like XML) directly from your software to your client’s software (or the government’s), where it is read and processed instantly without human hands touching it. Governments love this because it closes tax gaps, and now they are making it the law across the globe. If you work with clients in these regions, your current method of invoicing might become obsolete. You will likely need software that generates these specific machine-readable formats automatically to ensure you can still get paid. 2. AI Will Supercharge Your Financial Productivity Ignore the doom-and-gloom headlines about robots taking jobs. In 2026, AI is less about replacing you and more about giving you your weekends back. The technology has matured from a “cool experiment” to a daily essential for cutting down busy work. 3. Late Filing Penalties Are Increasing Governments are getting smarter. They are using better data to spot mistakes faster, and the leniency we saw in previous years is disappearing. 4. The Rise of Deepfakes is Creating New Cybersecurity Risks Small businesses often think they are too small to be targeted by hackers. Unfortunately, as large corporations tighten their security, attackers are pivoting to smaller, easier targets using terrifyingly realistic tech. 5. Remote Work is the New Standard (But It’s Hybrid) The concept of having your accountant “down the street” is fading. Business owners are increasingly prioritizing talent and tech-savviness over physical proximity. Future-Proof Your Business with Fynlo The common thread across all these trends is technology. Whether it is meeting new e-invoicing mandates, staying on top of deadlines to avoid steeper penalties, or leveraging AI to save time, you need tools that evolve as fast as the world does. That is why we are excited to introduce the recently launched Fynlo AI. We built Fynlo AI to directly address the productivity and accuracy challenges mentioned above. It allows you to simply upload receipts or bank statements, and our engine takes over from there. Fynlo AI extracts the data, categorizes every entry, and updates your financial reports in real-time with 100% accuracy. No more manual data entry errors, no more late nights classifying expenses, and no more guessing where your business stands. Ready to get ahead of the 2026 trends? Schedule a demo today and experience the future of automated accounting.

5 Financial Metrics Your Bank or Lender Will Check Before Giving You a Loan

You’ve poured your time, energy, and sleepless nights into building something strong. You’ve overcome the initial hurdles, found product-market fit, and now you’re ready for the next big leap. That means securing the capital required to hire, expand your inventory, or move into a bigger space. This journey, though, brings you face-to-face with a tough reality: obtaining that financing is often the single biggest hurdle for small businesses. According to 2025 research from Allica Bank, SME loan rejections have dramatically increased from just 5-10% three decades ago to 40% today. In other words, lenders are far more selective than they used to be. The moment you submit that application, you step into a rigorous due-diligence process where lenders are looking past your gross revenue to assess two critical things: risk and repayment capacity. If you don’t know the core metrics they care about, you can’t prepare your books effectively or present your case with confidence. Here are the five essential financial metrics your bank will scrutinize before approving your loan. In this article 1. Quick Ratio (Acid-Test Ratio) Think of the Quick Ratio as your company’s emergency financial safety net. It’s a crucial measure of short-term liquidity, answering the question every lender silently asks: “If sales hit a sudden wall, could this business instantly pay its most urgent bills?” This metric focuses only on your most liquid assets—cash and receivables—and deliberately excludes inventory because that can be slow to sell or difficult to liquidate quickly. Lenders generally look for a Quick Ratio above 1.0. A strong Quick Ratio proves you have the immediate cash flow cushion to weather an unexpected storm, which builds confidence in your business’s foundational health. To put it simply: if you owe $10,000 in short-term bills, lenders want to see at least $10,000 in highly liquid assets; ideally more. Quick Ratio = (Cash + Accounts Receivable + Marketable Securities) / Current Liabilities 2. Debt-to-Equity (D/E) Ratio The D/E Ratio measures the financial structure of your business. It answers whether you’re funding growth primarily through debt or through the owners’ investment (equity) and accumulated profits. Lenders look for a lower ratio, typically below 1.5. A high D/E ratio (say, 3.0) signals that your business is highly leveraged and therefore vulnerable if revenues dip, as fixed debt payments remain relentless. Conversely, a low ratio proves the owners are committed and the company has strong internal stability. Debt-to-Equity Ratio = Total Liabilities / Total Equity 3. Debt Service Coverage Ratio (DSCR) When a bank considers giving you a new loan, DSCR is what matters most. It is arguably the most critical metric for any new debt, measuring your company’s direct repayment capacity for all its debt obligations. DSCR = Net Operating Income / Total Debt Service (Principal + Interest Payments) Banks usually require a DSCR between 1.25 and 1.50. Think of this simply: a DSCR of 1.25 means your operating income is 125% of your required debt payments. This provides a safety margin. If your DSCR is below 1.0, the loan conversation stops instantly—you’re simply not generating enough income to cover your required payments. 4. Gross Profit Margin While the initial metrics focus on risk, the Gross Profit Margin proves the viability of your core business model. It answers: “How profitable is your product or service itself, before the lights are even turned on?” Lenders look for a high and consistent margin. A strong Gross Profit Margin proves that your core service is priced correctly and that you are efficient at managing your direct production costs (COGS). This shows the inherent earning power of your product, assuring the lender that even if overhead expenses rise, the core offering is financially sound. Gross Profit Margin = (Revenue – Cost of Goods Sold) / Revenue 5. Accounts Receivable (A/R) Aging and DSO This metric focuses on cash flow quality and the efficiency of your collections process. A healthy balance sheet is useless if you can’t actually get the money in the door. Lenders pay close attention to your A/R aging report to see how many outstanding invoices are over 90 days due. If a large percentage of your revenue is perpetually uncollected, that’s a massive red flag. Days Sales Outstanding (DSO) measures the average number of days it takes for you to collect revenue after making a sale. DSO = (Average Accounts Receivable / Total Credit Sales) x Number of Days Lenders want to see a low DSO, indicating fast and efficient collection (ideally under 45 days). A high DSO suggests your credit control is weak or your clients are unreliable, significantly raising the lender’s risk profile. Your Strategic Decision Securing a loan starts long before you submit the application. It begins with accurate, organized financial reporting. These five metrics are calculated directly from your Balance Sheet and Profit & Loss Statement. Trying to compile this data manually using spreadsheets is tedious and prone to error, which immediately hurts your credibility during a loan review. The businesses that secure the best rates are the ones that can provide clean, real-time reports instantly and confidently. Fynlo provides the clear, real-time financial reports you need to confidently demonstrate your stability and repayment capacity to any lender. Stop worrying about compiling data; start focusing on growth. Schedule a quick demo today to ensure your books are audit-ready and lender-approved.

Should You Lease or Buy Equipment? A Financial Breakdown

Every small business owner hits a wall where their old equipment just won’t cut it anymore. Maybe it’s time for a faster work truck, a major new piece of machinery, or simply upgrading every laptop in the office. This decision isn’t just about whether you have the cash today; it’s one of the most important financial choices you’ll make all year. The question of whether to lease (rent) or buy (own) directly impacts your immediate cash flow, your tax bill, and the overall look of your company’s financial health. Understanding the difference is the first step toward making a profitable move. In this article The Case for Buying (Financing or Ownership) When a business buys equipment, it usually means taking out a loan to cover the cost. You own the asset outright, and it immediately goes onto your Balance Sheet. The Tax Advantage: Depreciation The biggest financial benefit of buying is that you get to claim the entire purchase price as an expense over the asset’s useful life. This is called depreciation. It’s a wonderful non-cash deduction that essentially gives you a massive tax break. For example, in the United States, rules like Section 179 allow you to deduct the full purchase price of some assets immediately. No one wants a surprise bill from the tax authorities, and claiming depreciation is a straightforward way to reduce your taxable income. Cash Flow and Final Cost While the upfront cost might be higher or require a significant down payment, the long-term benefit is that you build equity. Once the loan is fully paid off, the asset is yours free and clear. If you use the equipment for ten years, your total cost of ownership (after taxes) can often be lower than renting it for the same period. The Case for Leasing (Renting or Operating) Leasing is essentially renting the equipment for a set period, typically three to five years. This option is popular because it minimizes risk and keeps things simple. Flexibility and Low Upfront Cost The primary appeal of leasing is the minimal initial expense. You usually don’t need a large down payment, making it ideal if your business needs to preserve cash liquidity for other operating expenses, like marketing or inventory. Because you don’t own the asset, when the lease is up, you simply hand the old equipment back and upgrade to the newest model, which is perfect for rapidly changing technology like computers or software licenses. Accounting Simplicity From an accounting perspective, leasing is straightforward. Your monthly lease payment is treated as a simple operating expense, similar to paying rent. It goes directly onto your Profit and Loss (P&L) Statement, reducing your gross profit immediately. This process is far less complicated to track than the depreciation schedules required when you buy. Decision Matrix: Choosing the Right Path The ideal choice depends entirely on your company’s needs and long-term outlook. When to Buy (Stability is Key): When to Lease (Flexibility is Key): Accounting Impact: How Each Choice Affects Your Statements Regardless of which path you choose, you need an organized system to track the financial consequences correctly. Buying is more complex to track. When you buy, you must record the full asset value and the corresponding liability (the loan) on your Balance Sheet. Then, your accounting system needs to correctly calculate and post the depreciation entries monthly or annually, following local tax rules. This meticulous tracking is essential if you ever need to apply for a loan, as banks will heavily scrutinize your Debt-to-Equity ratio. Example 1: Buying (The Balance Sheet Impact) When you buy a $10,000 piece of equipment with a loan, your books change immediately and permanently: Account Effect Statement Value Equipment Asset Increases Balance Sheet + $10,000 Loan Payable Liability Increases Balance Sheet + $10,000 Annual Depreciation Expense Increases P&L Statement + $1,000 Accumulated Depreciation Asset Value Decreases Balance Sheet + $1,000 The Takeaway: Buying creates a complex tracking relationship between the Balance Sheet (Asset/Loan) and the P&L (Depreciation). Leasing keeps your Balance Sheet clean. Since leasing is treated as an operating expense, the monthly payment only touches your P&L statement. It avoids adding large debt obligations to your books, which can sometimes be advantageous if your company is trying to stay lean to secure a future loan or meet specific financial covenants required by lenders. Example 2: Leasing (The P&L Simplicity) When you pay a $300 monthly lease payment, the transaction is simple and only affects two things: Account Effect Statement Value Lease Expense Expense Increases P&L Statement + $300 Cash Asset Decreases Balance Sheet – $300 The Takeaway: The cost is immediate, transparent, and easy to track, requiring no complex depreciation schedules. Your Strategic Decision The decision to lease or buy equipment is a strategic one, balancing immediate cash needs against long-term tax and ownership benefits. It requires careful tracking of depreciation schedules, loan balances, and expense categories. Don’t let these complex entries be a source of error or confusion. You need a system that ensures your fixed assets are tracked accurately, your depreciation is automatically calculated, and your financial reports are audit-ready, whether you are owning an asset or simply renting its use. Ready to gain control over your assets and deductions? Schedule a quick demo today to see how Fynlo simplifies fixed asset management, expense tracking, and financial reporting for growing businesses.

Free Alternatives to QuickBooks/Xero: The Best Free Accounting Tool for Micro-Businesses

Running a micro-business or a growing freelance operation means constantly balancing costs against value. You know you need professional accounting software—you need reports, tax compliance, and clean books. Yet, paying a monthly subscription for QuickBooks or Xero when your income is still irregular can feel like an unnecessary burden. You’re looking for a free alternative, but the search can be overwhelming. There are dozens of tools out there, and finding one that is truly free and powerful enough for a real micro-business is a challenge. The right tool is a strategic investment; it saves you time and ensures you build the solid financial foundation you need for future growth. Here, we review the top genuinely free alternatives available today. We look at their core features, limitations, and help you find the best starting point for your micro-business. Table of Contents Top 5 Truly Free Accounting Alternatives These platforms all offer a permanently free tier, making them excellent starting points for sole traders and service-based freelancers. Tool Primary Free Plan Name Best For Key Free Limitations Wave Starter Plan Purely Free & Simple (US/CA Focus) Bank feeds, receipt scanning, and some invoice customization require paid plan. Zoho Books Free Plan Scalability & Feature Depth Annual revenue limit applies; bank feeds, receipt scanning, and invoice customisation require paid plan. QuickFile XS, S and M UK-Based Low-Volume Transactions Limited to 1,000 nominal transactions per year. Pandle Pandle Free Unlimited Core Functionality Automated bank feeds and receipt uploads are reserved for the paid plan. Fynlo Forever Free Global Freelancers & Multi-Currency Limited to 20 monthly invoices; budget management and online payments require paid plan. Note: Platform features and pricing may change. Before starting a free trial, check the provider’s website for the latest service details and fees. 1. Wave Wave offers its accounting tools under the Starter Plan and is widely considered the best truly free option for freelancers and small businesses in the US and Canada. It has helped more than 5.9 million small business owners in the US and Canada manage their money since 2010. This plan includes unlimited invoicing, expense tracking, and basic financial reports. Bank feed automation and receipt scanning are not included in the free plan and require upgrading to Wave’s paid tier. Wave generates revenue through payment processing fees when clients pay invoices via credit card or ACH. https://www.waveapps.com 2. Zoho Books Zoho Books is part of a much larger ecosystem of business software, giving it a powerful advantage in scalability. It has 4.6/5 rating on G2 CROWD and 4.7/5 rating on SoftwareSuggest. The Free Plan is generous but comes with a clear cap: it is limited to a single user, a single accountant, 1,000 invoices per year, and you cannot exceed an annual revenue threshold limit which is set specifically for each region (e.g., $50,000 in the USA and £35,000 in the UK). If you are starting small and plan to stay small, this plan is excellent, offering features like a client portal and multi-lingual invoicing. Multi-currency handling, bill management, and automated bank feeds are typically locked into their paid tiers. https://www.zoho.com/books/free-accounting-software 3. QuickFile While primarily focused on the UK market, QuickFile is noteworthy for its feature-rich free plan. It receives 4.8/5 rating on TrustPilot, based on 2,940 reviews. The software is completely free as long as your 12-month nominal ledger transaction volume stays under 1,000. For a sole trader with low transaction volume, the free plan is exceptionally powerful, offering full multi-currency support and VAT/ITSA compliance tools (which are crucial for UK users). If you exceed 1,000 transactions, an annual fee of £60 plus VAT will apply. https://www.quickfile.co.uk 4. Pandle Pandle has more than 100,000 active users and has 4.6/5 rating on Trustpilot based on 1,290 reviews. Pandle offers its Free Plan with a strong focus on simplicity and unlimited core usage, meaning there are no limits on revenue or the number of invoices you can issue. The free tier includes invoicing, basic financial reports, and multi-currency support. As with many platforms, key automation features such as bank feeds (automatic transaction imports) and receipt uploads are reserved for the paid Pandle Pro version, which costs £5 per month plus VAT. This is an excellent choice for businesses prioritizing unlimited core functionality. https://www.pandle.com (Note: This is a UK-focused product.) 5. Fynlo Fynlo has a growing user base in the USA and Asia region. Thousands of businesses find that it makes invoicing and expense tracking simple and the service reliable. Fynlo is designed specifically for global freelancers and micro-businesses, meeting the need for robust multi-currency tracking without complexity. Its Forever Free plan provides up to 20 monthly invoices, expense tracking, Core Multi-Currency reporting, and access for 1 user plus 1 accountant. This makes it one of the best free options for entrepreneurs who receive or pay in different currencies. Certain advanced features, like accepting online payments and budget management, are reserved for our paid tiers to ensure high-level compliance as your business scales. https://www.fynloapps.com The Functional Limitations of Free Accounting Software Free” is a perfect place to start, allowing you to experiment and see which platform’s features and interface suit your working style. As you grow, you would need to be aware of the limitations that make the paid versions of accounting tools a worthwhile investment. Some common paid features include Bank Feed Automation, Multi-Currency Tracking and FX Gains/Losses, and Hard Limits on Revenue, Users, or Transactions. Bank Feed Automation The primary feature restricted in most free plans is Bank Feed Automation. This means the platform will not automatically import and categorize your transactions from your bank. While manual entry works for very low volume, spending hours every month manually entering or uploading transactions can be a major drain on your time—time that is better spent earning revenue. Multi-Currency Tracking and FX Gains/Losses This is the single biggest failure point for most free accounting software. If you deal with international clients, free platforms often do not automatically calculate Foreign Exchange (FX) Gains and Losses needed for accurate reporting. This complex calculation must then be done manually (often in a messy spreadsheet), significantly increasing your risk of tax mistakes. Hard Limits on Revenue, Users, or Transactions As tools like Zoho Books show, many platforms impose a hard revenue limit. If you