You’ve poured your time, energy, and sleepless nights into building something strong. You’ve overcome the initial hurdles, found product-market fit, and now you’re ready for the next big leap. That means securing the capital required to hire, expand your inventory, or move into a bigger space.

This journey, though, brings you face-to-face with a tough reality: obtaining that financing is often the single biggest hurdle for small businesses. According to 2025 research from Allica Bank, SME loan rejections have dramatically increased from just 5-10% three decades ago to 40% today.

In other words, lenders are far more selective than they used to be. The moment you submit that application, you step into a rigorous due-diligence process where lenders are looking past your gross revenue to assess two critical things: risk and repayment capacity.

If you don’t know the core metrics they care about, you can’t prepare your books effectively or present your case with confidence. Here are the five essential financial metrics your bank will scrutinize before approving your loan.

In this article

- 1. Quick Ratio (Acid-Test Ratio)

- 2. Debt-to-Equity (D/E) Ratio

- 3. Debt Service Coverage Ratio (DSCR)

- 4. Gross Profit Margin

- 5. Accounts Receivable (A/R) Aging and DSO

- Preparation as a Competitive Advantage

1. Quick Ratio (Acid-Test Ratio)

Think of the Quick Ratio as your company’s emergency financial safety net. It’s a crucial measure of short-term liquidity, answering the question every lender silently asks: “If sales hit a sudden wall, could this business instantly pay its most urgent bills?”

This metric focuses only on your most liquid assets—cash and receivables—and deliberately excludes inventory because that can be slow to sell or difficult to liquidate quickly. Lenders generally look for a Quick Ratio above 1.0. A strong Quick Ratio proves you have the immediate cash flow cushion to weather an unexpected storm, which builds confidence in your business’s foundational health.

To put it simply: if you owe $10,000 in short-term bills, lenders want to see at least $10,000 in highly liquid assets; ideally more.

Quick Ratio = (Cash + Accounts Receivable + Marketable Securities) / Current Liabilities

2. Debt-to-Equity (D/E) Ratio

The D/E Ratio measures the financial structure of your business. It answers whether you’re funding growth primarily through debt or through the owners’ investment (equity) and accumulated profits.

Lenders look for a lower ratio, typically below 1.5. A high D/E ratio (say, 3.0) signals that your business is highly leveraged and therefore vulnerable if revenues dip, as fixed debt payments remain relentless. Conversely, a low ratio proves the owners are committed and the company has strong internal stability.

Debt-to-Equity Ratio = Total Liabilities / Total Equity

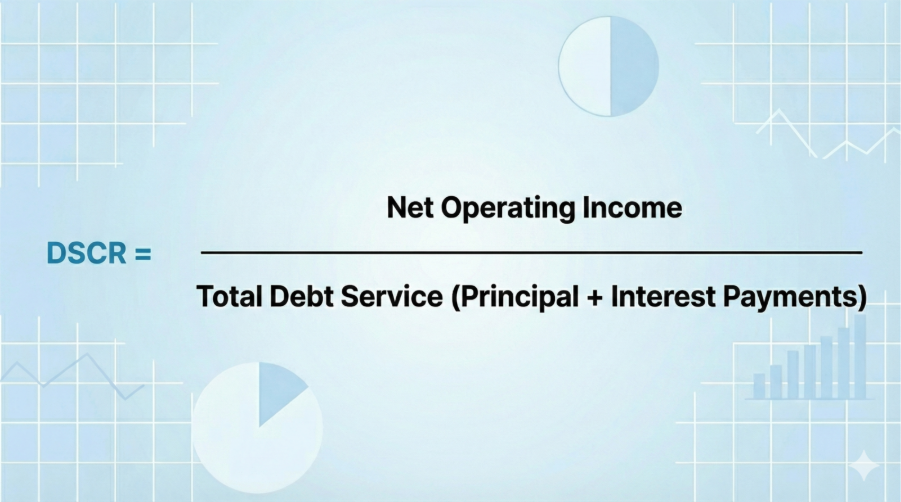

3. Debt Service Coverage Ratio (DSCR)

When a bank considers giving you a new loan, DSCR is what matters most. It is arguably the most critical metric for any new debt, measuring your company’s direct repayment capacity for all its debt obligations.

DSCR = Net Operating Income / Total Debt Service (Principal + Interest Payments)

Banks usually require a DSCR between 1.25 and 1.50. Think of this simply: a DSCR of 1.25 means your operating income is 125% of your required debt payments. This provides a safety margin. If your DSCR is below 1.0, the loan conversation stops instantly—you’re simply not generating enough income to cover your required payments.

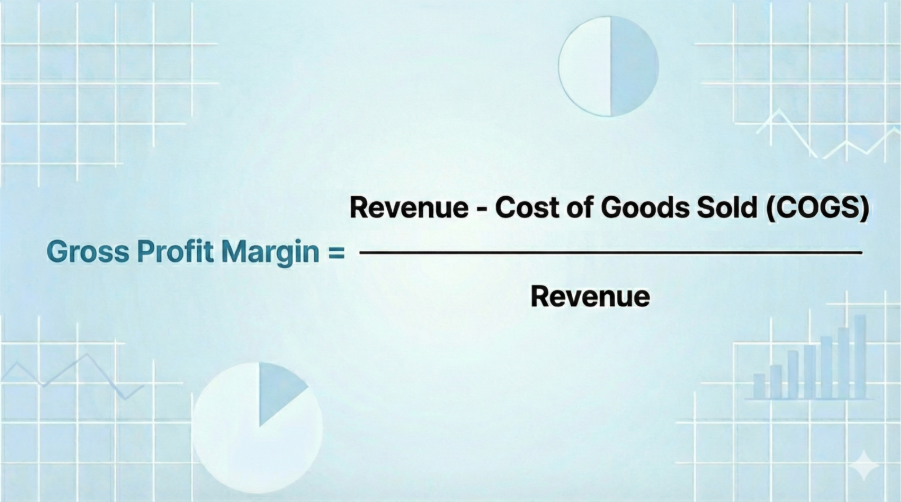

4. Gross Profit Margin

While the initial metrics focus on risk, the Gross Profit Margin proves the viability of your core business model. It answers: “How profitable is your product or service itself, before the lights are even turned on?”

Lenders look for a high and consistent margin. A strong Gross Profit Margin proves that your core service is priced correctly and that you are efficient at managing your direct production costs (COGS). This shows the inherent earning power of your product, assuring the lender that even if overhead expenses rise, the core offering is financially sound.

Gross Profit Margin = (Revenue – Cost of Goods Sold) / Revenue

To see why your total sales are different from the money you actually keep, read our guide on the difference between revenue and profit to make sure your business stays healthy.

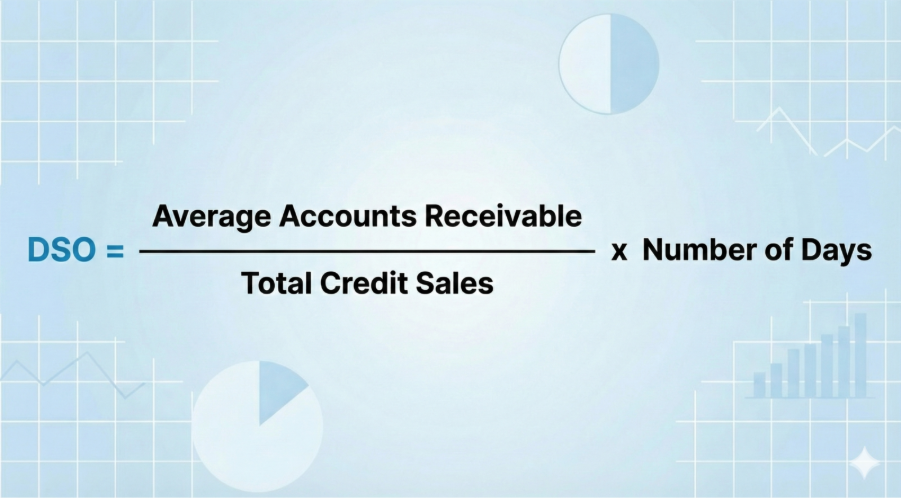

5. Accounts Receivable (A/R) Aging and DSO

This metric focuses on cash flow quality and the efficiency of your collections process. A healthy balance sheet is useless if you can’t actually get the money in the door.

Lenders pay close attention to your A/R aging report to see how many outstanding invoices are over 90 days due. If a large percentage of your revenue is perpetually uncollected, that’s a massive red flag.

Days Sales Outstanding (DSO) measures the average number of days it takes for you to collect revenue after making a sale.

DSO = (Average Accounts Receivable / Total Credit Sales) x Number of Days

Lenders want to see a low DSO, indicating fast and efficient collection (ideally under 45 days). A high DSO suggests your credit control is weak or your clients are unreliable, significantly raising the lender’s risk profile.

Preparation as a Competitive Advantage

Securing a loan starts long before you submit the application. It begins with shifting your mindset from “keeping the books” to “strategic reporting.” Lenders aren’t just looking at your bank balance; they are looking for a narrative of stability and foresight.

When you can present these five metrics clearly and instantly, you demonstrate that you aren’t just a business owner—you are a sophisticated operator who understands risk and repayment capacity. In the competitive 2026 lending environment, that level of clarity is often the difference between a rejection and an approval at the best possible rates.

About the Author

Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity.

With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.