Congratulations! Hiring your first employee is a monumental step for any small business or freelancer. It means your business is growing, your vision is expanding, and you’re ready to take on new challenges. But with this exciting milestone comes a crucial responsibility: payroll.

For many new employers, the word “payroll” conjures images of complex forms, confusing calculations, and potential IRS penalties. It can feel like stepping into a minefield! But don’t let that overwhelm you. While it’s true that payroll compliance requires attention to detail, breaking it down into manageable steps makes it much less daunting. This guide will walk you through everything you need to know to set up payroll legally and efficiently for your very first hire in the U.S. We’ll cover federal and state requirements, common pitfalls, and smart strategies to ensure both you and your new team member start off on the right foot.

Table of Contents

- Before You Hire: Employee vs. Independent Contractor

- Setting Up Payroll in 7 Easy Steps

- Don’t Let Payroll Be a Headache!

Before You Hire: Employee vs. Independent Contractor

This is arguably the most critical decision you’ll make upfront. Mistakenly classifying an employee as an independent contractor can lead to severe penalties from the IRS and state labor departments.

- Employee: Generally, you control what the person does and how they do it. You provide tools, set hours, and offer benefits.

- Independent Contractor: The individual controls how the work is done. They typically use their own tools, set their own hours, and offer services to multiple clients.

The IRS uses several factors (behavioral, financial, and type of relationship) to determine classification. When in doubt, err on the side of caution or consult a professional. The consequences of misclassification—like back taxes, penalties, and interest for unpaid payroll taxes (Social Security, Medicare, unemployment)—can be financially devastating.

Setting Up Payroll in 7 Easy Steps

Once you’ve decided you’re hiring an employee, here’s a checklist to get your payroll system up and running:

1. Get an Employer Identification Number (EIN)

The first and most important step is getting your Employer Identification Number (EIN) from the IRS. It’s the unique ID that helps identify your business for tax reasons at both the state and federal levels. The application is free and can be completed online on the IRS website—and you’ll need it to report taxes, hire employees, and open business bank accounts. Once you have your EIN, the IRS’s Publication 15, Employer’s Tax Guide is a must-read resource to understand your ongoing payroll tax responsibilities.

2. Register with State’s Labor and Tax Agencies

This step is crucial and varies by state. At a minimum, you’ll need to register for state income tax withholding (if your state has an income tax) and state unemployment insurance (SUI). These registrations allow you to properly withhold taxes from your employee’s paycheck and pay into your state’s unemployment system.

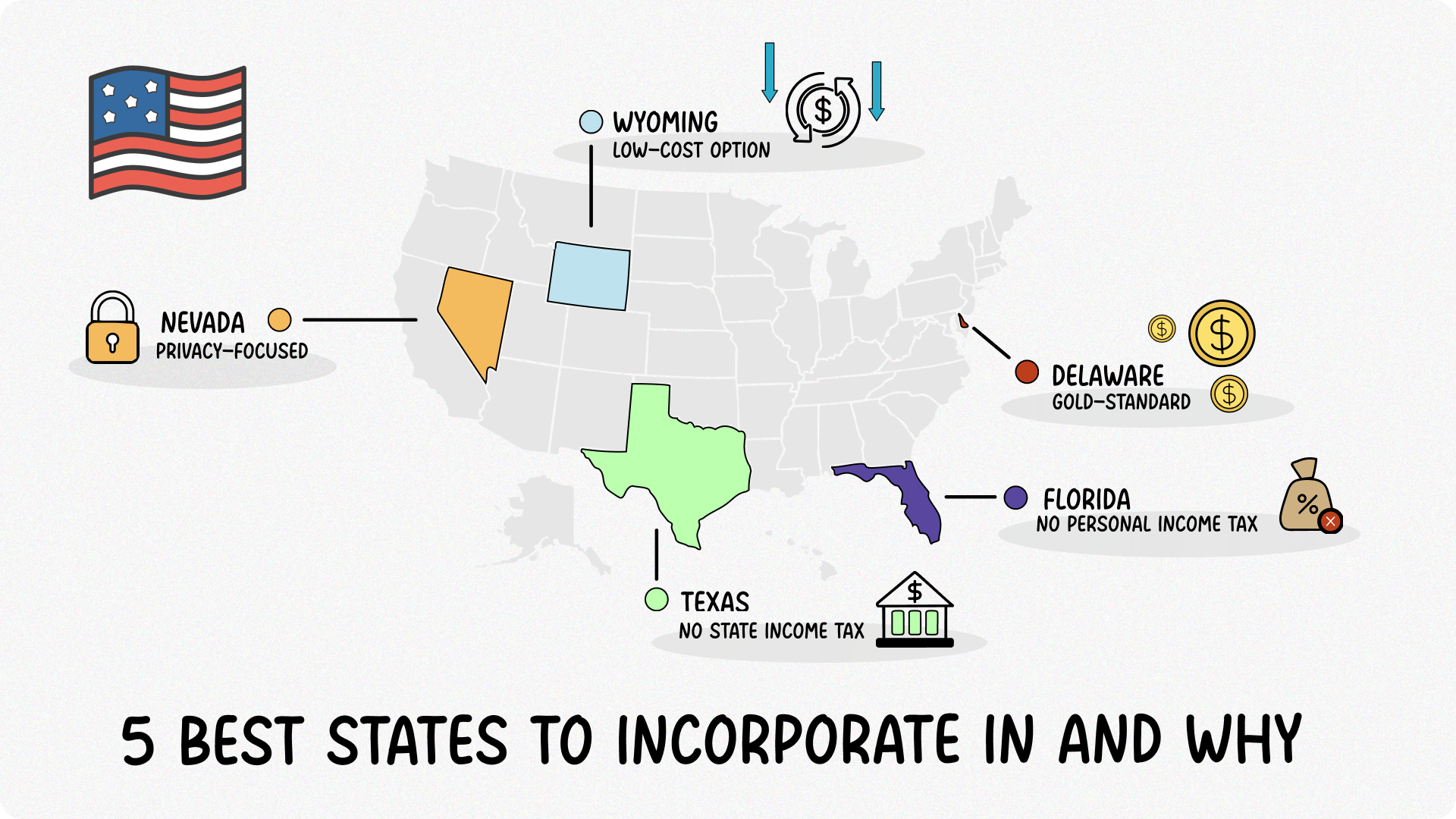

Many states also require you to secure workers’ compensation insurance, often starting with your very first employee. A quick search for “new employer registration” plus your state name will usually point you to the correct agency. For example, in California you’d register with the Employment Development Department (EDD), while in Texas you’d register with the Texas Workforce Commission (TWC) for state unemployment insurance (since Texas has no state income tax).

3. Gather Employee Paperwork

Before your first employee starts, they’ll need to complete several essential forms:

- Form I-9, Employment Eligibility Verification: This form verifies that your employee is legally authorized to work in the U.S. You must review original documents (like a passport or driver’s license + Social Security card) and retain the form.

- Form W-4, Employee’s Withholding Certificate: This form tells you how much federal income tax to withhold from their paycheck. Employees fill this out, indicating their filing status, dependents, and any additional withholding.

- State Withholding Forms: While the Form W-4 handles federal income tax, many states have their own forms to determine state income tax withholding. For example, your employee in California would fill out Form DE-4, while an employee in Arizona would use Form A-4. Your state’s Department of Revenue or a quick search for “employee withholding form” for your state will point you to the correct document. It’s also important to remember that if your business is in a state with no state income tax—such as Texas, Florida, Nevada, or Washington—you won’t need to have your employee complete a separate state form for income tax withholding.

- Direct Deposit Authorization: If you plan to offer direct deposit, you’ll need their bank account and routing number.

4. Choose Your Payroll Schedule

Will you pay weekly, bi-weekly, semi-monthly, or monthly? Bi-weekly (every two weeks) is common for many small businesses, resulting in 26 paychecks per year. Whatever you choose, be consistent and communicate it clearly to your employee. State laws often dictate minimum pay frequency.

5. Understand Federal Payroll Taxes

The next critical step is understanding the federal taxes you’re responsible for. As an employer, you have a legal obligation to withhold and pay several taxes on behalf of your employees. These include:

- Federal Income Tax: Withheld from employee’s pay based on their W-4.

- Social Security Tax: 6.2% withheld from employee’s gross wages (up to the annual limit, which is $176,100 for 2025). You, as the employer, also pay a matching 6.2%.

- Medicare Tax: 1.45% withheld from employee’s gross wages (no wage limit). You, as the employer, also pay a matching 1.45%.

- Fun Fact: For high earners, employees may owe an additional 0.9% Additional Medicare Tax on wages above $200,000 (single) or $250,000 (married filing jointly).

- Federal Unemployment Tax (FUTA): You pay this entirely as the employer. The rate is 6.0% on the first $7,000 of each employee’s wages, though you can usually get a credit of up to 5.4% for timely state unemployment tax payments, effectively reducing the FUTA rate to 0.6%.

Note: Each year, some states (called “credit reduction states”) may not qualify for the full credit if they’ve borrowed federal funds to cover unemployment benefits. Employers in those states could pay a slightly higher effective FUTA rate.

Since tax rates are updated regularly, always confirm with IRS publications or online calculators to verify your withholdings.

6. Understand State and Local Payroll Taxes

Beyond federal taxes, you’ll also deal with:

- State Income Tax Withholding: Required in most states, but not all (e.g., Texas, Florida, Washington have no state income tax).

- State Unemployment Insurance (SUI): You, as the employer, pay this. Rates vary significantly by state and can change based on your business’s unemployment claims history.

- Local Taxes: Some cities or counties have their own income taxes or other local payroll taxes.

7. Choose a Payroll Method

Now for the big question: how will you actually run payroll?

- Manual Payroll: You calculate everything yourself, file all forms, and make all payments. This is highly risky for new employers due to the complexity and potential for errors leading to penalties.

- Payroll Software: You use a dedicated software (like a standalone payroll system or integrated accounting software) to automate calculations, withholdings, and tax filings. This significantly reduces errors and ensures compliance.

- Full-Service Payroll Provider: You outsource your entire payroll process to a company that handles everything from calculations to tax filings and direct deposits. This is the most hands-off approach but comes with a higher cost.

Estimates from the American Payroll Association (APA) show that automated payroll solutions can reduce processing costs by as much as 80% compared to manual methods. This isn’t just about saving money; it’s about avoiding costly mistakes and the substantial fines that can come with them.

Don’t Let Payroll Be a Headache!

Hiring your first employee should be an exciting journey, not a source of stress over tax liabilities and complex regulations. Getting your small business payroll right from the start protects your business, builds trust with your new team, and ensures you remain compliant with the IRS and state agencies. Remember, penalties for late or incorrect filings can quickly add up, turning a small oversight into a big problem for your small business finances.

This is where a tool like Fynlo comes in. Our easy-to-use software is designed for small business owners and freelancers, providing the real-time financial insights you need to manage your business effectively. By streamlining your core accounting and bookkeeping tasks, Fynlo gives you a clear picture of your income and expenses, empowering you to confidently manage payroll costs and stay on top of your financial obligations.

Ready to make your first hire confidently? Start a free trial to see how Fynlo can help simplify your financial management.