When Should You Move from a Sole Proprietorship to an LLC or S-Corp?

When you first go full-time as a freelancer, your focus is naturally on delivery—landing contracts, hitting deadlines, and refining your craft. Legal paperwork often feels like a secondary chore, a task to be addressed “eventually.” However, the structure you choose today determines how much of your hard-earned profit you actually keep and how well your personal life is protected if a project ever faces a legal challenge. If you are billing significant amounts without a formal entity, you may be unintentionally risking your personal savings for the sake of administrative convenience. Choosing a business structure is a trade-off between simplicity and security. For most freelancers, the transition from a Sole Proprietorship to an LLC or S-Corp is triggered by two specific milestones: reaching $50,000 in annual profit or taking on high-stakes contracts where a professional error could result in a personal lawsuit. In this article The Real-World Cost of Legal Exposure These risks are more than theoretical; without a legal bridge between your business and your personal life, a simple mistake can become a financial catastrophe. In both cases, an LLC would have acted as a circuit breaker, likely limiting the liability to the business’s assets rather than the freelancer’s life savings. Evaluating Your Structure Options Freelance Business Structures: A Quick Comparison Guide 1. The Sole Proprietorship This is the default setting for anyone who begins working for themselves without formal filing. It is the path of least resistance, but it offers the least protection. 2. The Limited Liability Company (LLC) An LLC is a registered entity that exists separately from you as an individual. It is the standard for professional freelancers who want to safeguard their personal finances. 3. The S-Corp Election An S-Corp is not a separate entity you register with the state, but a tax status you request from the IRS. It is the primary tool high-earning freelancers use to reduce their tax burden. Identifying the Financial Turning Point While the legal protection of an LLC is valuable at any stage, the tax benefits of an S-Corp become clear once you look at the math. Let’s compare the tax liability for a freelancer earning $100,000 in annual profit. S-Corp vs. LLC: Visualizing the Tax Savings Structure Self-Employment Tax (15.3%) Total FICA Tax Bill Standard LLC Paid on the full $100,000 $15,300 S-Corp Election Paid only on $60,000 (Salary) $9,180 Annual Tax Savings $6,120 The Milestone: As a general rule, once your annual profit clears $75,000, the tax savings of an S-Corp usually outweigh the $1,500–$2,000 cost of professional accounting and payroll software. Until you reach that mark, a standard LLC provides the most efficient balance of protection and simplicity. Maintaining Your Liability Protection Registering an LLC is only the first step. If you treat your business account like a personal fund, a lawyer can argue in court that the business and the individual are one and the same. To keep your protection intact, adopt these three habits: Common Q&A 1. Does an LLC protect me if I personally make a mistake on a project? An LLC is not a “get out of jail free” card for professional negligence. If you are personally responsible for a major error—like accidentally deleting a client’s database—you can still be held liable. This is why the most professional approach is a “two-tier” strategy: use a Business Structure for debt and contract protection, and Professional Liability Insurance for your actual work-product. 2. I am just starting out—can I change my structure later? Yes, and most freelancers do exactly that. It is common to start as a Sole Proprietorship for the first few months, register an LLC once contracts grow larger, and elect S-Corp status once profits stabilize above the $75,000 mark. Your legal structure should evolve alongside your income. 3. Do I need a lawyer to set this up? For a single-member LLC, many freelancers file directly with their Secretary of State or use a registration service. However, if you have business partners or are moving toward an S-Corp, a 30-minute consultation with a CPA is a wise investment to ensure you are meeting all federal and local tax requirements. 4. How does my structure affect my ability to get a mortgage? Lenders generally view S-Corp and LLC owners similarly as self-employed individuals. They typically look at your “net income” over the last two years. The main difference is that an S-Corp provides you with W-2s, which can sometimes make the application process feel slightly more traditional to a loan officer. [Try Fynlo to see exactly how much an S-Corp could save you]

LLC vs. S-Corp in 2026: How to Save $10,000 in Self-Employment Tax

If you’ve successfully scaled your business past the six-figure mark, you’ve reached a significant milestone. Yet, as your revenue grows, the business structure that served you as a lean startup may no longer be the most efficient vehicle for your success. In 2026, many high-performing founders are discovering that staying in their “default” setup is a choice that costs them thousands of dollars in unnecessary tax leakage every single year. Most freelancers stay in a basic LLC because it’s easy. While simplicity has its merits in the beginning, relying on it indefinitely often leads to a massive missed opportunity for wealth building. In a six-figure business, that “simplicity” isn’t free—it represents capital that could be better spent on a strategic new hire, upgrading your technology stack, or funding your retirement. In this article Understanding the Self-Employment Tax Threshold To understand how to save money, we first have to look at how the IRS views a standard LLC. In the eyes of the tax man, you and your LLC are a “disregarded entity”—meaning you are essentially the same person. This results in 100% of your net profit being hit with a 15.3% self-employment tax to cover Social Security and Medicare. As you scale, this math becomes painful. By electing S-Corp status, you fundamentally change the relationship between you and your money. You become an employee of your own business, allowing you to pay yourself a “reasonable salary” (which is taxed) while taking the remaining profit as a distribution. These distributions are exempt from that 15.3% tax, which is exactly where the five-figure savings come from. Business Structure Comparison Between LLC vs S-Corp vs C-Corp Selecting a structure is more than just tax optimization; it is about ensuring your legal framework aligns with your long-term strategic vision. While the S-Corp is often the ideal choice for service-based founders, the C-Corp (or “Inc.”) remains the gold standard for those intending to scale globally or raise outside capital. In fact, approximately 95% of venture capital is directed toward C-Corps because they support the unlimited shareholders and complex stock classes that institutional investors demand. Feature Standard LLC S-Corp Election C-Corp (Inc.) Tax Filing Personal 1040 (Schedule C) 1120-S + K-1 Form 1120 (Corporate) Payroll Requirement None Mandatory W-2 salary Mandatory for active owners Self-Employment Tax 15.3% on 100% of profit 15.3% on salary only None (on dividends) Management Style Flexible; Member-managed; no board required Formal; Requires Board of Directors and Officers Strict; Board oversight with mandatory annual minutes Audit Risk Higher; Schedule C filings often draw IRS scrutiny Lower; Formal structure and payroll reduce “red flags” Moderate; Professional compliance is expected Primary Benefit Maximum simplicity Tax savings for $100k+ earners Scalability & VC funding Primary Drawback High tax as revenue scales Compliance & payroll costs Potential double taxation Finding the Salary Sweet Spot for Maximum Savings The biggest “catch” with an S-Corp is that you must pay yourself a “reasonable salary”. If you pay yourself $0 to avoid all taxes, the IRS will audit you; if you pay yourself your entire profit, the S-Corp becomes a useless expense. We generally look at three tiers of profit to find that “sweet spot”: Maximizing the 20% Qualified Business Income Deduction The Qualified Business Income (QBI) deduction allows many business owners to deduct up to 20% of their business income from their taxes. For S-Corp owners, this deduction is calculated on your profit after your salary is paid. While powerful, the 20% Qualified Business Income (QBI) deduction is subject to limits once your total taxable income rises above the annual thresholds (for example, around $203,000 for single filers and $406,000 for married filing jointly, indexed for inflation). Above these levels, the deduction is gradually restricted based on the type of business you operate and how much you pay in W-2 wages or own in qualified business property. For specified service businesses (such as consulting, legal, medical, and similar fields), the deduction phases out completely as income increases. For other businesses, the deduction can still apply but is capped using wage and property formulas. The key planning strategy is to set a salary that meets IRS “reasonable compensation” rules without unnecessarily reducing the pool of business profit that may qualify for the 20% QBI deduction. Protecting Your Assets by Maintaining the Corporate Veil Both LLCs and Corporations offer a layer of protection for your personal assets, shielding them from business debts and lawsuits. However, this protection depends on maintaining a clear separation between personal and business activity. Implementation Checklist & Deadlines Transitioning to an S-Corp requires discipline in your accounting and adherence to strict IRS timelines. 1. The March 15th DeadlineTo be taxed as an S-Corp for the 2026 calendar year, you must file IRS Form 2553 by March 15, 2026. If you miss this date, your election typically won’t take effect until the following tax year, though “Late Election Relief” is sometimes available for businesses with a valid reason for the delay. 2. Formalize Your BookkeepingBecause the S-Corp is a separate tax entity, “co-mingling” funds (using business money for personal groceries) is a significant compliance risk. You must maintain pristine records and clear separation between business and personal accounts. 3. Set Up Monthly PayrollYou cannot simply “take money out” as an S-Corp owner. You must use a payroll provider (like Gusto or Rippling) to withhold taxes from your salary and issue yourself a W-2 at the end of the year. Moving Toward an Optimized Structure The move from a standard LLC to an S-Corp is a sign of business maturity. It shifts your focus from simply maintaining operations to strategically optimizing for wealth. If your business is consistently netting over $100,000, continuing as a basic LLC is no longer a matter of simplicity—it’s a matter of unnecessary expense. Ready to Optimize Your 2026 Tax Strategy? Don’t let March 15th slip by without a plan. Fynlo helps six-figure founders transition to optimized structures that protect their revenue and simplify their compliance. Schedule a Strategy Audit to see if an S-Corp election is the right move for your 2026 revenue goals.

Advanced LLC Strategy: How to Structure for Growth and Asset Protection in 2026

Most founders start with a single LLC because it is the simplest path to getting a tax ID. But as your revenue grows or you begin developing your own products, a single-entity setup may no longer be the most efficient choice. In 2026, the goal is to build a structure that protects your personal assets while remaining flexible enough to scale. Here is how experienced founders structure their businesses to manage risk and optimize for long-term growth. In this article The “Parent & Child” Strategy (Holding Companies) When all your business assets—client contracts, intellectual property (IP), and equipment—live in one LLC, they are all exposed to the same risks. If a client dispute leads to a lawsuit against that LLC, every asset inside it is potentially at risk. The Solution: A Two-Tiered Structure Strategic State Selection: Where to Place Your Entities When choosing where to register your “Parent” or “Child” companies, you can take advantage of specific state rules to manage your tax burden and maximize protection. Wyoming: The Ideal “Parent” Home Wyoming is frequently chosen for the Parent company because it does not require the names of owners to be listed in public records. In 2026, this state-level anonymity provides a layer of data security. Additionally, Wyoming has strong Charging Order laws, meaning if you face a personal lawsuit, it is very difficult for a creditor to seize your business assets. Texas: Scaling the “Child” Company For an Operating Company with a physical presence, Texas offers a significant threshold for small businesses. While Texas has a “Margin Tax,” businesses with total revenue below $2,650,000 in 2026 generally owe $0 in state franchise tax. This allows you to utilize Texas’s vast talent pool and infrastructure without a state-level tax bill until you reach a significant scale. Nevada: High-Level Liability Protection If your business operates in a high-liability field, Nevada is a strong choice for your Operating Company. Nevada law provides an “Exclusive Remedy” protection. This means that a charging order is the only way a creditor can pursue a member’s interest, preventing them from ever seizing business assets or forcing the company to shut down to pay a debt. Tennessee: The “Asset-Light” Advantage Tennessee recently overhauled its tax code, which is highly beneficial for remote agencies and freelancers. In the past, the state taxed businesses based on the value of the physical property they owned (the “property measure”). As of 2026, that rule has been eliminated. Now, the franchise tax is calculated at 0.25% of your apportioned net worth. For example, if your business has a net worth of $200,000 and 50% of your activity is in Tennessee, you are taxed on $100,000 ($250 per year). Additionally, a $50,000 standard deduction now applies to the excise tax, which exempts many small businesses with modest profits from paying that portion of the tax entirely. Planning for an Institutional Exit Even if you do not plan to sell your business immediately, keeping your entity “exit-ready” ensures you don’t lose value during a future sale or funding round. The “Delaware Flip”Most startups begin in Wyoming or their home state to save on costs. Institutional investors, though, almost exclusively require a Delaware entity because of its sophisticated court system. “Flipping” to Delaware involves a legal process called a Statutory Conversion. In this process, you file “Articles of Conversion” in both your current state and Delaware. This legally transforms your existing LLC into a Delaware Corporation while maintaining your business’s history, EIN, and contracts. Doing this 12 months before a planned sale ensures that your legal foundation is already in the format buyers expect, preventing delays in the deal. The Financial Impact of Professional Record-KeepingDuring a sale, buyers perform “due diligence” to verify your business’s health. If your financial records are unorganized or personal and business expenses are blurred, it increases the buyer’s risk. Professionally maintained books signal a mature, low-risk operation, which often results in a higher final valuation for the founder. How Fynlo Simplifies Multi-State Management Managing multiple entities and state-specific tax rules can be a complex administrative task. Fynlo is designed to handle the financial details of these advanced structures so you can stay focused on your core work. Is your business structure ready for the next level? Sign up for Fynlo today and let us manage the financial details while you build your enterprise.

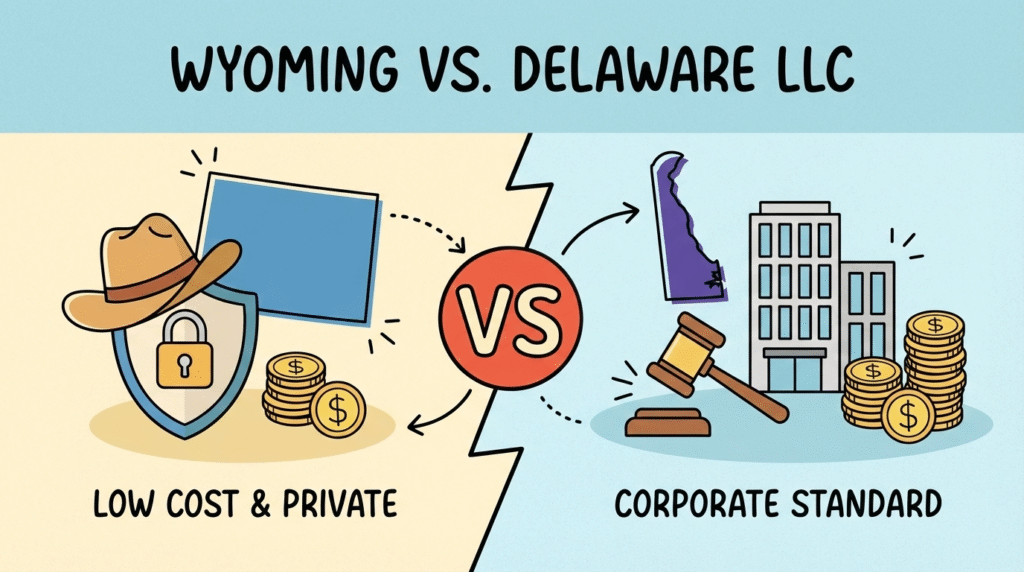

Wyoming vs. Delaware LLC: A Strategic Look at Your Business Home in 2026

I recently caught up with a founder who was set on registering her digital agency in Delaware. When I asked why, her answer was simple: “It’s what everyone does.” After we walked through her three-year plan, it turned out she was about to take on administrative costs and legal layers that her current model didn’t actually need. Picking a state for your LLC isn’t a one-size-fits-all choice anymore. In 2026, with state filing systems going digital and federal reporting—like the Corporate Transparency Act—getting more specific, the right choice depends on your funding path, your need for privacy, and where you actually sit at your desk. Let’s look at the actual numbers and the logic behind both states so you can make a call based on what fits your business today. In this article 2026 Maintenance and Compliance Overview To see the long-term impact on your bank account, you need to look at the recurring costs. While starting an LLC costs roughly the same in both states, the yearly bills look quite different. Category Wyoming LLC Delaware LLC Yearly Maintenance Fee $60 (Annual Report) $300 (Franchise Tax) Late Filing Penalty No late fee; but non-filing = dissolution. $200 Flat Fee + 1.5% Interest State Income Tax 0% 0% (unless the LLC has Delaware-source income) Setup Cost (State Fee) $100 $110 Privacy Rank (2026) Top Tier Mid Tier 1. Why Delaware is the “Legal Standard” Delaware’s biggest selling point isn’t its tax rate; it’s the legal system. The state is home to the Court of Chancery, a specialized court that only hears business disputes. Because judges (not juries) decide these cases, the outcomes are incredibly predictable. This predictability is exactly why over 65% of Fortune 500 companies are incorporated in Delaware. If you plan to raise venture capital or offer stock options to employees, most investors will expect a Delaware entity. It’s the “legal language” they already speak, which can save you a lot of time during a fundraising round. 2. The Annual Cost of Doing Business in Delaware While the legal benefits are a major draw, they come with a fixed price tag. Every Delaware LLC pays a $300 Annual Franchise Tax. Think of this as a mandatory subscription fee to keep your company active. In 2026, the state remains very strict about its June 1st deadline. If you’re even a day late, a $200 penalty hits your account. Over a five-year stretch, you’re looking at a minimum of $1,500 in state taxes just to exist in Delaware. For a bootstrapped startup, that is capital that could have been spent on your first marketing campaign or hardware. 3. The Wyoming Advantage: Privacy and Lower Overhead If you aren’t chasing Wall Street investors, Wyoming is often the smarter move for lean operations. They don’t have a franchise tax; they just have a $60 Annual Report Fee. Beyond the savings, Wyoming is famous for its privacy. In 2026, data security is a top concern for founders. Wyoming allows you to keep the names of your LLC’s members and managers off the public record. In a world where your personal info is often just a Google search away, this “anonymity by default” is a huge plus for many business owners. 4. Asset Protection: The “Charging Order” Shield One technical detail you’ll appreciate is Wyoming’s Charging Order Protection. This is a legal shield that prevents a personal creditor from seizing your business assets or forcing you to sell the company to pay a personal debt. Wyoming was the first state to give this protection to single-member LLCs, and their laws are still among the strongest in the country. Delaware offers great protection too, but Wyoming’s statutes are often preferred by legal experts for smaller, closely-held businesses that want to keep their professional and personal lives strictly separate. 5. Registering “Away from Home”: The Foreign Qualification Rule This is the part where many founders accidentally double their workload. If you live in a state like California or New York but register your LLC in Wyoming to save on taxes, you usually have to register as a “Foreign LLC” in your home state anyway. This process often involves: Industry data suggests that roughly 30% of founders who incorporate out-of-state eventually pay significantly more in multi-state compliance fees than they would have by simply incorporating in their home state. Unless you have a specific legal or privacy reason to be in Wyoming or Delaware, incorporating where you live is often the path of least resistance. Which State Fits Your Business? Deciding on a state usually comes down to your “exit strategy” and where you actually spend your time. How Fynlo Makes State Compliance Easier Starting the business is the fun part, but keeping the books clean is what keeps the business alive. Whether you choose Delaware or Wyoming, you still need to prove your business is a separate legal entity from your personal life. Fynlo is built to help you handle that without the headache: Starting a business is a marathon. Picking the right state just sets the pace. If you’re ready to get your finances organized from day one, Sign up for Fynlo today. We’ll handle the books while you build the business.

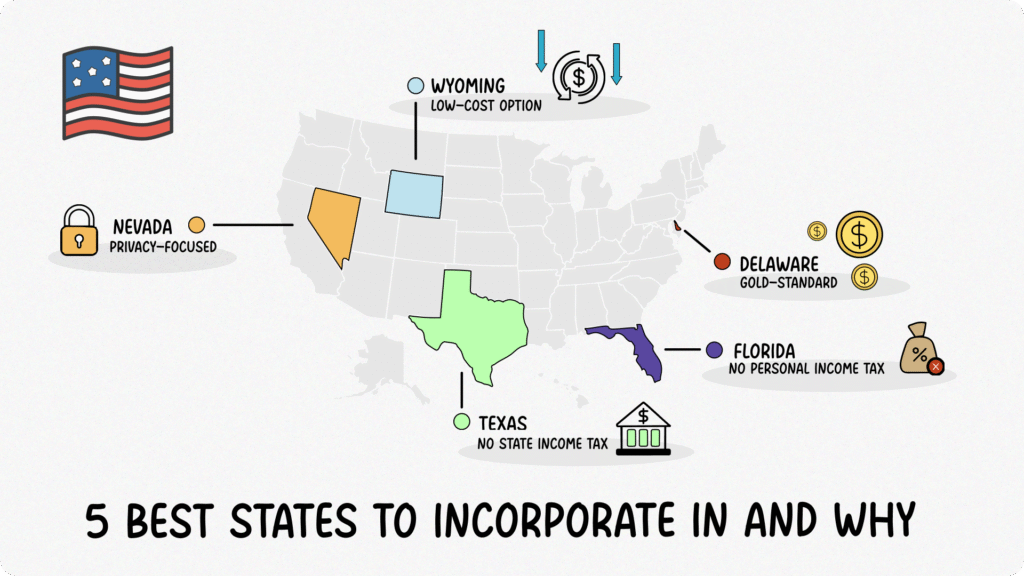

5 Best U.S. States to Incorporate In: 2026 Tax & Legal Guide

When I started my first small business, I remember staring at a blank screen, Googling “where should I incorporate?” I found conflicting advice, fees that seemed to change overnight, and legal jargon that made my head spin. Over time—after a few “oops” moments and some late-night research—I narrowed it down to five states that consistently offer the best mix of low costs, solid legal protections, and friendly environments for entrepreneurs. Here’s what I’ve learned, updated with the correct figures as of January 2026. Table of Contents Delaware: The Gold Standard for Big (and Small) Businesses “People joke that Delaware exists just so corporations can incorporate there, and it almost feels that way when you see how slick their system is.” Why Delaware? Fees (2026): Most small business owners should budget at least $225 to $450 per year depending on which method they use. For very large companies, the tax is generally capped at $200,000, though “Large Corporate Filers” (those with over $750M in assets or revenue) are subject to a higher $250,000 cap. Personal note: My first LLC wasn’t in Delaware—it was in my home state. But after attending a startup accelerator and hearing investors talk about “Delaware C-Corp, please,” I re-formed there. I still recall breathing a sigh of relief when I realized investors are so comfortable with Delaware entities that legal due diligence becomes that much smoother. Wyoming: The Friendly, Low-Cost Option for Small Businesses “Think of Wyoming as the underdog—no one talks about it as much as Delaware, but it quietly checks all the right boxes for a lean, mean small-business machine.” Why Wyoming? Personal note: When I was a freelancer, I formed a single-member Wyoming LLC just because the yearly cost was so low. It felt thrilling to pay only $160 total each year and know my personal assets had a legal buffer. Nevada: Privacy-Focused with No Corporate Income Tax “Nevada is like Wyoming’s more opulent cousin—privacy protections, no state income tax, and a reputation as the ‘Florida of the West’ for tax benefits.” Why Nevada? Fees (2026): In total, expect around $875 in year one (incorporation + list + license). Subsequent years are $650 (license $500 + annual list of officers $150). I know that sounds steeper than Wyoming, but if privacy and zero state tax on profits matter, many entrepreneurs find Nevada worth the up-front costs. Personal note: A colleague once told me, “If you live in California but want to keep your taxes honest, move to Nevada for your mental health.” He wasn’t wrong—no state income tax means one fewer headache at tax time. Texas: No State Income Tax + Seller’s Market for Services “Texas is booming—no state income tax, a thriving entrepreneurial scene, and a sense of ‘everything’s bigger in Texas,’ including opportunities.” Why Texas? Personal note: I once thought I’d set up shop in California, but I cringed at that 13.3% top-bracket personal rate on top of corporate taxes. Texas felt like a breath of fresh air—zero state income tax, and Austin’s startup vibe makes you feel like anything’s possible. Florida: No Personal Income Tax + Moderate Corporate Tax “Florida is that friend who loves to chill in flip-flops but still knows how to hustle—no personal income tax, solid consumer market, and a growing tech ecosystem.” Why Florida? Personal note: I spent a summer in Miami Beach brainstorming a business plan on the sand. The idea of paying zero state income tax gave me the energy to work late nights—and if you’ve ever tried running spreadsheets in 90-degree heat, trust me, you’ll appreciate anything that saves you a percentage point of tax. Things to Consider When Choosing a State TL;DR A quick overview of the five best states to incorporate in, plus why they might be a fit for you: State Formation Fee Annual Cost Corporate Tax Personal Tax Key Benefits Delaware $89 (C-Corp) $225 or $450 franchise tax + $50 report 8.7% (only if doing business in DE) None – Chancery Court– Flexible corporate laws– Investor-friendly Wyoming $100 (LLC) $60 annual report None None – Lowest fees– Strong privacy & asset protection– No state income tax Nevada $75 (C-Corp) $650 (license + list) None (under $4M revenue) None – Robust privacy– No corporate/personal income tax– Specialized Business Court Texas $300 (Corp) $0 (if under $2.65M revenue) 0.375%–0.75% (Margin Tax) None – No personal income tax– Large business ecosystem– Franchise tax exemption under $2.65M Florida $70 (C-Corp) $150 (Corp) or $138.75 (LLC) 5.5% None – No personal income tax– Growing tech hubs– Moderate corporate tax Final Thoughts There’s no one-size-fits-all “best state”—it really depends on your budget, growth plans, and tolerance for paperwork. When I first started, the difference between $60/year (Wyoming) and $540/year (Delaware) felt huge. But as my business matured and I talked to investors, it became clear that Delaware could save me weeks of legal back-and-forth. Meanwhile, friends who run lean e-commerce stores from home still swear by their $160/year Wyoming LLCs. In the end, pick the state that aligns with your current priorities: cost, privacy, investor confidence, or community. And remember, you can always form in one state and later register as a foreign entity in another (it’s called “qualifying” to do business in your home state). That’s exactly what many growth-stage startups do: incorporate in Delaware, then register in their home state so they can open a bank account, hire W-2 employees, and sign leases without legal headaches. I hope this guide helps you sleep a little easier as you choose your business’s “home.” Wherever you decide to incorporate, know that every entrepreneur—myself included— started exactly where you are right now: staring at a blank filing form, hoping they made the right choice. Need Help with Your Accounting? At Fynlo, we know every state has its own quirks—whether it’s Delaware’s Chancery Court, Wyoming’s low fees, Nevada’s privacy rules, Texas’s franchise tax, or Florida’s corporate rate. Our expert team can handle your bookkeeping, annual filings, and state-specific tax planning no matter where you incorporate. Schedule a call

The S-Corp Secret: How to Pay Yourself a “Reasonable Salary” and Avoid an IRS Audit

Deciding to become an S-Corp is a smart move for many freelancers and small business owners. It’s a way to save on self-employment taxes, allowing you to keep more of your hard-earned money. But here’s the catch: you can’t just pay yourself a token salary and take the rest as tax-free distributions. The IRS is watching, and underpaying yourself is one of the fastest ways to land on their audit list. With great tax savings comes great responsibility. The IRS has a strict rule you can’t afford to ignore: you must pay yourself a “reasonable salary.” Paying yourself fairly isn’t just a good idea—it’s an IRS requirement. The agency is actively cracking down on S-Corps that pay owners a nominal salary just to avoid payroll taxes. Getting this wrong can lead to serious penalties and a lot of unnecessary stress. This guide will walk you through exactly what a reasonable salary means for your business, providing the facts and advice you need to stay on the right side of the law. Table of Contents Understanding Your Tax Advantage To grasp the importance of a reasonable salary, you first need to understand the S-Corp tax advantage. As a sole proprietor, your entire business profit is subject to a 15.3% self-employment tax. An S-Corporation is a “pass-through” entity, meaning it does not pay federal income tax on its profits. Instead, the profits are passed through to you, the owner, to be taxed on your personal return. You can legally split your income into two categories: This powerful tax strategy hinges entirely on your ability to prove that the salary you pay yourself is “reasonable” in the eyes of the IRS. How the IRS Defines “Reasonable” The IRS doesn’t provide a magic number or a fixed formula. You may have heard advice about splitting your income using a simple ratio, like 50/50 or 60/40. The IRS does not approve of these simple formulas, as they don’t reflect the true market value of the work you do. Instead, they require your salary to be what you would pay an unrelated person to perform your job. In fact, IRS guidance and case law point to nine factors they often weigh: your training and experience, duties and responsibilities, time devoted to the business, dividend history, payments to non-shareholder employees, timing and manner of bonuses, comparable industry salaries, use of a formula for determining pay, and your business’s overall performance. In practice, these boil down to a few key areas: Illustrating the Impact: A Tax Comparison To see the real-world difference, let’s look at two freelance photographers who both operate as S-Corps and net $90,000 in profit. Photographer A (Reasonable Salary) Photographer B (Unreasonably Low Salary) Net Business Profit $90,000 $90,000 Salary Paid $55,000 $25,000 Owner’s Distribution $35,000 $65,000 FICA Tax on Salary (15.3%) $8,415 $3,825 FICA Tax on Distribution $0 $0 Total FICA Tax Bill $8,415 $3,825 Photographer B’s total FICA tax bill is much lower, but by paying an unreasonably low salary, they expose themselves to an IRS audit. If an audit occurs, the IRS can reclassify the distributions as wages and require them to pay the back taxes, plus penalties and interest. This proves that a defensible salary is the safest and smartest long-term strategy. The High Cost of Non-Compliance Ignoring the reasonable salary rule is a serious risk. If the IRS audits your business and finds your salary to be unreasonably low, they can reclassify your distributions as wages. This will lead to: There are plenty of cautionary tales. In Barron v. Commissioner, an Arkansas accountant paid himself no salary at all, taking all earnings as distributions. The IRS determined a reasonable salary should have been around $45K–$49K, and he was hit with back taxes. Similarly, in David E. Watson, P.C. v. United States, an Iowa CPA set his salary at just $24,000 while taking over $200,000 in distributions. The court sided with the IRS, which reclassified $175,000 as wages, resulting in nearly $27,000 in payroll taxes owed. The IRS has publicly stated that S-Corp owner compensation remains a “compliance priority” in 2025. They continue to flag unusually low salaries as an audit trigger — a reminder that this issue is very much alive today. Frequently Asked Questions (FAQ) 1. Can I pay myself only distributions in an S-Corp? No. The IRS requires shareholder-employees to take a reasonable salary before distributions. Skipping salary is one of the fastest ways to trigger an audit. 2. What if my business isn’t making much profit yet? If profits are low, your salary can be modest, as long as it reflects your role and time spent in the business. The key is to keep documentation. 3. How do I prove my salary is reasonable? Use market data (BLS, Glassdoor, Salary.com), document your duties and hours, and keep board minutes or memos showing how you set compensation. 4. What happens if the IRS reclassifies my distributions? You’ll owe back payroll taxes, plus penalties and interest. In rare cases, the IRS can revoke your S-Corp election altogether. Ready to Simplify Your S-Corp? Navigating the rules of an S-Corp can feel complex, but it doesn’t have to be a source of anxiety. Building smart financial habits and having the right tools can help you confidently run your business and enjoy the tax savings you’ve worked hard for. This is where a tool like Fynlo comes in. Our easy-to-use software is built for freelancers and small business owners, making it simple to run payroll for your S-Corp, track your income and expenses, and maintain the clean, audit-ready records you need to protect your business. We take the guesswork out of bookkeeping, so you can focus on what you do best. Ready to take control of your S-Corp finances? Schedule a call with us to see how Fynlo can help your business thrive.

LLC Tax Filing Checklist: Your Guide to Staying Compliant

Navigating tax season for a Limited Liability Company (LLC) can feel like a maze. While an LLC provides legal liability protection, when it comes to taxes, its structure is incredibly flexible, offering different paths you can take. This flexibility is a huge advantage but also means you need to know exactly which route is right for you. This checklist is designed to help freelancers and small business owners in the USA understand their LLC tax filing requirements. We’ll break down the forms you need, the documents you must gather, and the critical deadlines to keep you on the right side of the IRS. Table of Contents LLC Taxation Explained This is where things get interesting. Unlike an S-Corp, an LLC doesn’t have its own tax classification. Instead, the IRS sees an LLC as a “disregarded entity” by default. This means the IRS “disregards” the LLC and taxes its owner(s) based on the business structure they’d otherwise be. This gives you a few different options: This flexibility is a huge benefit, but the first step is knowing which classification your LLC falls under. The Most Important Deadline to Know Your tax deadline depends entirely on how your LLC is taxed. These deadlines apply to LLCs with a calendar-year fiscal year. LLCs with a fiscal year ending on a different date have deadlines based on their tax year-end (e.g., the 15th day of the third month after the fiscal year for Partnerships and S-Corps, or the fourth month for C-Corps). Consult a tax professional to confirm your specific deadlines. No matter your classification, if you need more time, you can file for an extension using the appropriate form (e.g., Form 4868 for a Sole Proprietorship or Form 7004 for a Partnership or Corporation). This gives you an additional six months to file, but remember, an extension to file is not an extension to pay. The LLC Tax Filing Checklist Let’s get down to business. Here are the items you’ll need to prepare for your LLC tax filing, based on your classification. 1. Essential Financial Records Start by getting your financial house in order. Make sure invoices and receipts are organized and complete. This is the foundation of every tax return. 2. Key IRS Forms Feeling a bit overwhelmed by the list of forms? Don’t worry—you don’t have to be a tax expert to understand the essentials. Here’s a breakdown of the most important forms you’ll encounter and a heads-up on what to watch out for. Form 1040 & Schedule CFor single-member LLCs, this is the main event. You will file Schedule C, Profit or Loss from Business, as part of your personal Form 1040. This form reports all your business income and expenses. A common mistake here is mixing personal and business expenses, which can lead to messy audits. Form 1065 & Schedule K-1For multi-member LLCs, this is the main informational return. Your LLC will file Form 1065, U.S. Return of Partnership Income. This form reports the business’s overall financial activity. You’ll then use Schedule K-1 to report each partner’s individual share of the profits and losses, which they then use to file their personal returns. A frequent error is miscalculating each member’s ownership percentage, which can lead to incorrect allocations. Form 1099-NEC: Nonemployee CompensationThis form is for reporting payments to freelancers or independent contractors who are not employees. You must file a 1099-NEC for each person you paid $600 or more during the year. The most common mistake with this form is missing the filing deadline, which is January 31, 2026. Since that date falls on a weekend, the due date is the next business day, which is Monday, February 2, 2026. The penalties for late filing of returns due in 2025 are tiered. The penalty is $60 per form if filed within 30 days after the due date, $120 if more than 30 days late but filed by August 1, 2025, and $310 if filed after August 1, 2025, or not filed at all. Penalties for 2026 returns due in 2027 may increase due to inflation adjustments; check IRS updates for exact amounts. Note that businesses filing 10 or more returns in 2026 must e-file and obtain a Transmitter Control Code (TCC) by November 1, 2025. Another frequent error is using the wrong form (e.g., using a 1099-MISC instead of a 1099-NEC for non-employee compensation) or entering an incorrect Taxpayer Identification Number (TIN), so be sure to double-check that information. 3. Don’t Forget These Details! A few small mistakes can lead to big problems. Double-check these items before filing. The Cost of Missing a Deadline The penalties for filing late depend on your LLC’s tax classification. Get Ready for a Smoother Tax Season Preparing for an LLC’s tax filing can feel like a big responsibility. But with a clear plan and the right tools, it’s entirely manageable. By proactively gathering your documents and paying close attention to deadlines, you can minimize stress and avoid costly penalties. Disclaimer: The information provided in this guide is for informational purposes only and does not constitute legal or tax advice. For specific tax situations, always consult with a professional accountant or tax advisor. This is where having a reliable accounting system can make all the difference. When all your financials—from income and expenses to payroll—are organized and synced in one place, generating the reports you need for your tax professional (or for filing yourself) becomes a streamlined process. Fynlo is designed to simplify these tasks, so you can focus on what you do best: running your business. Ready to see how Fynlo can transform your tax prep? Schedule a call with our experts to find out more!

C-Corp Tax Filing Checklist: The Definitive Guide to Corporate Filing

Navigating tax season for a C-Corporation can feel like a significant responsibility. Unlike a pass-through entity, a C-Corp is a separate legal and taxable entity, making its tax filings more involved. But with a clear checklist and a solid understanding of the deadlines, you can get through it with confidence. This guide is designed for business owners in the USA who have chosen to incorporate as a C-Corporation, helping you understand the necessary forms, documents, and key dates to stay compliant with the IRS. Table of Contents C-Corp Taxation Explained First, a quick refresher. A C-Corporation is a legal entity entirely separate from its owners. A key distinction is that the C-Corp itself pays corporate income taxes on its profits. Then, when it distributes dividends to its shareholders, those individuals are taxed on that income as well—a process commonly referred to as double taxation. Despite this, C-Corps offer significant advantages for certain businesses, such as unlimited growth potential, the ability to raise capital by selling stock, and robust legal liability protection for shareholders. This structure is often favored by startups with plans for venture capital funding or eventual public offerings. The Most Important Deadline to Know For a calendar-year C-Corp, the main deadline for filing your federal return is April 15, 2026 (for the 2025 tax year). This is also the due date for your first quarterly estimated tax payment. For the 2026 tax year, the deadline will be April 15, 2027. If you need more time, you can file for an extension using Form 7004, which gives you an additional six months to file, pushing your deadline to October 15, 2026. However, remember that an extension to file is not an extension to pay. If you expect to owe any tax, you must pay it by the April 15 deadline to avoid penalties and interest. The C-Corp Tax Filing Checklist Let’s get down to business. Here are the items you’ll need to prepare for your C-Corp tax filing. 1. Essential Financial Records Start by getting your financial house in order. Make sure invoices and receipts are organized and complete. 2. Key IRS Forms Feeling a bit overwhelmed by the list of forms? Don’t worry—you don’t have to be a tax expert to understand the essentials. Here’s a breakdown of the most important forms you’ll encounter and a heads-up on what to watch out for. 3. Don’t Forget These Details! A few small mistakes can lead to big problems. Double-check these items before filing. The Cost of Missing a Deadline Filing a C-Corp’s tax return late can be costly, and the IRS imposes two main types of penalties: If both penalties apply in the same month, the late filing penalty is reduced to 4.5%, so the combined monthly penalty is 5%. If a return is more than 60 days late, the minimum penalty is the lesser of $510 or 100% of the unpaid tax. This is an increase from the $485 penalty that applied for the 2024 tax year. Remember, interest is also charged on all unpaid amounts, which can add up quickly. It’s always best to file on time even if you can’t pay the full amount due. Get Ready for a Smoother Tax Season Preparing for a C-Corp’s tax filing can feel like a big responsibility. But with a clear plan and the right tools, it’s entirely manageable. By proactively gathering your documents and paying close attention to deadlines, you can minimize stress and avoid costly penalties. Disclaimer: The information provided in this guide is for informational purposes only and does not constitute legal or tax advice. Tax rules are subject to change, so always check IRS.gov or consult with a professional accountant or tax advisor for your specific situation. This is where having a reliable accounting system can make all the difference. When all your financials—from income and expenses to payroll—are organized and synced in one place, generating the reports you need for your tax professional (or for filing yourself) becomes a streamlined process. Fynlo is designed to simplify these tasks, so you can focus on what you do best: running your business. Ready to see how Fynlo can transform your tax prep? Schedule a call with our experts to find out more!

S-Corp Tax Filing Checklist: Simplify Your Tax Season

Tax season for a small business owner is a bit like a marathon—you know the finish line is coming, but getting there requires preparation, stamina, and a good plan. For S-Corporations, the process has its own unique rules and deadlines. Missing a step or a key date can lead to a lot of headaches (and penalties!). This checklist is designed to help freelancers and small business owners in the USA navigate their S-Corp tax filing with confidence. We’ll break down the forms you need, the documents you must gather, and the critical deadlines to keep you on the right side of the IRS. Table of Contents S-Corp Taxation Explained First, a quick refresher. S-Corps are known as “pass-through” entities. This means the business itself typically doesn’t pay federal income tax. Instead, the profits, losses, deductions, and credits “pass through” to the shareholders (that’s you!) who then report them on their own personal tax returns. This is a huge benefit because it avoids the “double taxation” that C-Corporations face. However, just because the business doesn’t pay income tax doesn’t mean it gets a free pass. You still need to file an informational return with the IRS, which is where this checklist comes in. The Most Important Deadline to Know For a calendar-year S-Corp, the main deadline for filing your federal return is March 17, 2025 (for the 2024 tax year), because March 15, 2025 falls on a Saturday and the due date moves to the next business day. For the 2025 tax year, the deadline will be March 16, 2026 (since March 15, 2026 falls on a Sunday). Mark your calendar and don’t miss it! If you need more time, you can file for an extension using Form 7004, which will give you an additional six months to file. But remember, this only extends the time to file, not the time to pay. If you expect to owe any tax (for things like built-in gains or excess passive income), you must pay it by the filing deadline (March 17, 2025; March 16, 2026) to avoid penalties and interest. The S-Corp Tax Filing Checklist Let’s get down to business. Here are the items you’ll need to prepare for your S-Corp tax filing. 1. Essential Financial Records Start by getting your financial house in order. Make sure invoices and receipts are organized and complete. 2. Key IRS Forms As a business owner, you become an expert in many things—and tax forms are no exception. Here’s a breakdown of the most important forms you’ll encounter and a heads-up on what to watch out for. 3. Don’t Forget These Details! A few small mistakes can lead to big problems. Double-check these items before filing. The Cost of Missing a Deadline Filing late can be expensive. For the 2024 tax year, the penalty for a late S-Corp filing is $245 per month (or part of a month) the return is late. This penalty is multiplied by the number of shareholders. For example, if your S-Corp has two shareholders, the penalty is $490 per month. This can add up quickly! Get Ready for a Smoother Tax Season Filing taxes for an S-Corp can feel daunting, but with a clear plan and the right tools, it’s entirely manageable. By proactively gathering your documents and paying close attention to deadlines, you can minimize stress and avoid costly penalties. This is where having a reliable accounting system can make all the difference. When all your financials—from income and expenses to payroll—are organized and synced in one place, generating the reports you need for your tax professional (or for filing yourself) becomes a streamlined process. Fynlo is designed to simplify these tasks, so you can focus on what you do best: running your business. Ready to see how Fynlo can transform your tax prep? Schedule a call with our experts to find out more!

What is the Delaware Franchise Tax? Tax Calculation and Payment Process Explained

If you’re a freelancer or small business owner with a registered entity in Delaware, you’ve likely heard of the Delaware Franchise Tax. Don’t let the name intimidate you. It’s not a tax on your income or profits, but rather a fee you pay to the state of Delaware for the privilege of having your business registered there. Think of it as an annual maintenance fee for your business entity. This guide will break down everything you need to know about the Delaware Franchise Tax in simple, easy-to-understand terms. Table of Contents Who Needs to Pay the Delaware Franchise Tax? Any business entity registered in Delaware is required to pay this tax. This includes: Note: Exempt domestic corporations (e.g., non-profits) are not required to pay the tax but must still file an annual report (and pay the $50 report fee). Fast Facts & Data (Sources: Delaware Division of Corporations, 2023 Annual Report) Due Dates: Mark Your Calendar! Entity Type Tax Due Report Due Penalty for Late Filing C-Corporations $175–$200K March 1 $200 + 1.5% interest/month on unpaid LLCs, LPs, GPs $300 June 1 $200 + 1.5% interest/month on unpaid How to Calculate the Delaware Franchise Tax Delaware offers two ways to calculate your corporate franchise tax—Authorized Shares or Assumed Par Value Capital—and you’ll pay the lower amount. When you file on the official Delaware Division of Corporations website, it defaults to Authorized Shares, so run the Assumed Par Value Capital calculation yourself to compare. For LLCs and Partnerships: A Simple Flat Fee For LLCs, LPs, and GPs, the calculation is straightforward. It’s a flat annual fee of $300. For Corporations: Two Calculation Methods For corporations, the calculation is more complex. Delaware provides two methods to calculate your franchise tax. You are permitted to pay the lower of the two amounts. When you go to pay your tax online, the state’s system will default to the Authorized Shares Method, so it’s worth taking the time to calculate your tax using both methods. Here is a step-by-step breakdown of the calculation: Step 1 – Calculate the “Assumed Par”: Divide your Total Gross Assets by your Total Issued Shares. Carry the result to six decimal places. This gives you the “assumed par.” Step 2 – Calculate the “Assumed Par Value Capital”: Multiply the “assumed par” you just calculated by the Total Number of Authorized Shares. Step 3 – Calculate the Tax: The tax rate is $400 for every $1,000,000 of Assumed Par Value Capital. If your Assumed Par Value Capital is less than $1,000,000, you will divide it by 1,000,000 and then multiply by $400. If it’s over $1,000,000, you round up to the next million. Since the minimum tax for this method is $400, your final tax due using the Assumed Par Value Capital Method would be $400. By using the Assumed Par Value Capital Method and paying the minimum of $400 (plus the $50 annual report fee), a corporation in this example would save a significant amount compared to the Authorized Shares Method, which would have resulted in a much higher tax bill. How to Pay Your Delaware Franchise Tax The state of Delaware requires online payment for the franchise tax and annual report filing. Here’s how to do it: By understanding these simple blocks—and knowing where to look on the official Delaware Division of Corporations website—you’ll stay in good standing and keep your focus on growing your business. Take the Next Step Ready to take the hassle out of your business finances? At Fynlo, we specialize in helping freelancers and small business owners—just like you—stay compliant, organized, and focused on growth. From managing your Delaware Franchise Tax filings to crafting custom financial dashboards, our team acts as your in-house finance department—without the overhead. Schedule your free discovery call