Financial Statements: A Comprehensive Guide

Most of us who go out on our own do it for the work itself. Whether you’re a designer, a writer, or a consultant, you’re driven by the craft. But then you start your business, and you realize you’ve also become its reluctant Chief Financial Officer. I remember my first year, staring at my accounting software and feeling completely out of my depth. I was great at my actual job, but when it came to the money side, I was just guessing. I’d look at my bank account, see money in there, and figure I was doing okay. But I always had this low-level hum of uncertainty. Am I really making a profit? Am I charging enough? Where is all the money going? It turns out the answers to those questions are sitting in three financial reports. They sound intimidating, but they’re really just tools to help you trade that uncertainty for clarity. Table of Contents The Income Statement: Answering, “Did I Actually Make a Profit?” Sample Income Statement (Source: principlesofaccounting.com) This is the most basic question, and the Income Statement (often called the P&L for Profit & Loss) answers it directly. It’s a simple summary of your revenue versus your expenses over a specific period, like a month or a quarter. In my early days, I felt like I was working constantly but my savings weren’t growing. I finally sat down and looked at my P&L. The “aha!” moment wasn’t some huge, dramatic discovery. It was seeing I was spending nearly $150 a month on various software subscriptions I’d signed up for and forgotten about. It’s the small leaks that often sink the ship. The P&L helps you spot them. It shows you the real cost of doing business, beyond just the big, obvious expenses. The Balance Sheet: A Snapshot of Your Business’s Financial Health Balance Sheet (Source: principlesofaccounting.com) Being profitable month-to-month is great, but you also want to know if you’re building a stable business over the long term. That’s where the Balance Sheet comes in. If the P&L is a movie of your recent performance, the Balance Sheet is a snapshot of your business’s financial health right now. It’s based on a simple formula: Assets (What you have) = Liabilities (What you owe) + Equity (What’s yours) Honestly, for a long time, I ignored my Balance Sheet. It felt too “corporate.” But it’s surprisingly practical. And critical, too: according to Intuit QuickBooks, 57% of small business owners have experienced problems with their cash flow. Business owners lose $34,000 on average by being forced to turn down work, specifically due to issues created by insufficient cash flow. That “Accounts Receivable” line shows you exactly how much money you’re waiting on from clients. Seeing that number get too big can be the nudge you need to get better about your payment terms and follow-ups. The Cash Flow Statement: Tracking Where Your Money Really Goes Cash Flow (Source: principlesofaccounting.com) This is the big one. Have you ever had a profitable month on paper but felt completely broke? I’ve been there. You’ve done the work, you’ve sent the invoices, but your bank account is dangerously low and bills are due. This is a cash flow problem, and the Cash Flow Statement is the tool that explains it. It tracks the actual cash moving in and out of your business. According to SCORE, 82% of small businesses that fail do so because of poor cash flow. It’s not that they aren’t profitable, it’s that they run out of cash. A friend of mine who runs a small trade business almost learned this the hard way. His P&L looked fantastic because he was landing big jobs. But he was paying his suppliers in 30 days, while his clients were taking 60 or even 90 days to pay him. His business was profitable, but it was being starved of cash. The Cash Flow Statement made this timing gap impossible to ignore. It forced him to start collecting deposits upfront and tighten his payment deadlines. It didn’t just lower his stress; it saved his business. From Numbers to Know-How Look, nobody gets into freelancing because they have a passion for spreadsheets. But you owe it to yourself and your business to understand the basics. You don’t need to become an accountant, you just need to get curious. Start small. Ask your bookkeeper or use your accounting software to run your P&L once a month. Take 20 minutes to look at it. Where did your money come from? Where did it go? Doing this consistently replaces that vague financial anxiety with quiet confidence. You start making decisions based on real data, not just a gut feeling. And in this line of work, having fewer unpleasant surprises is one of the best assets you can have. Ready to trade that financial uncertainty for clarity? At Fynlo, we handle the accounting and bookkeeping so you can focus on what you do best. Let us help you understand the story your numbers are telling. Schedule a free call with us today. You may also like these articles:

I Thought I Was Saving Money—Then the IRS Came Knocking

A Client’s Story: How a “Cheap” Bookkeeper Nearly Cost Him Everything At Fynlo, we work with entrepreneurs every day to build and protect their businesses. Recently, a new client came to us with a story so cautionary, we felt it had to be shared. With his permission, here is the real story of how a single decision—hiring the wrong bookkeeper—led to the collapse of his company, and the powerful lessons every business owner can learn from his experience. Table of Contents How It All Started It started with a simple desire to save a few bucks. As the owner of a growing trucking service, he knew every penny counted. Fuel costs, maintenance, insurance – the overhead was already sky-high. So, when he found a bookkeeper who promised to handle all his finances for a fraction of the price of the more established firms, it felt like a savvy business move. It was a decision he would come to regret more than any other. His name was John, a friendly, soft-spoken man the client found after a quick Google search. John’s website highlighted years of bookkeeping experience, so the client trusted him. He talked a good game, promising to streamline everything, maximize deductions, and keep the IRS and state tax authorities happy. For the first year, everything seemed to be running smoothly. The paperwork was filed, the owner received reports that looked professional, and most importantly, he was saving a significant amount on bookkeeping fees. Money he ploughed back into the business, buying a new rig and taking on more drivers. The business was growing, and he felt like he was finally living the dream he’d worked so hard for. The first crack in the facade was small. A letter from the state tax office about a discrepancy in the company’s fuel tax filings under the International Fuel Tax Agreement (IFTA). John brushed it off as a minor clerical error, assuring the owner he would handle it. Busy managing a fleet that was now running 24/7, the owner took him at his word. Then came another notice—this time from the IRS—about underpaid payroll taxes. Again, John had a plausible explanation. It was the government’s bureaucracy, he said, always getting things mixed up. The Audit That Changed Everything The real trouble began when the company was selected for a random audit by the IRS. The owner wasn’t too worried at first; he believed his operation was clean. When he called John to let him know, for the first time, he heard a flicker of panic in the bookkeeper’s voice. John became evasive, promising to get all the necessary documents in order. That was the last proper conversation they ever had. As the audit date loomed, John became harder and harder to reach. Voicemails went unanswered. Emails bounced back. A visit to his small rented office found it empty, cleared out as if he had vanished into thin air. It was then, the owner described, that a cold, hard knot of dread began to form in the pit of his stomach. With the auditors waiting, he had no choice but to hire a reputable accounting firm to make sense of the mess John had left behind. What they uncovered was a nightmare. John, the “affordable” bookkeeper, had been running a sophisticated scam. He wasn’t filing the IRS or state tax returns properly at all. The professional-looking reports he’d been given were complete fabrications. John had been pocketing a portion of the money intended for tax payments, making only the minimum payments required to avoid immediate red flags. He had misclassified employees, failed to remit payroll taxes correctly, and completely ignored the company’s compliance with IFTA. The audit revealed the full, horrifying extent of the damage. The business owed a staggering amount in back taxes—and that was just the beginning. The penalties and interest were astronomical, a testament to years of neglect and deceit. The business, the dream he had poured his life’s savings and countless sleepless nights into, was insolvent. The cost of getting compliant, of paying the IRS and state penalties, was simply more than the company could bear. The Bitter Decision The choice was brutal: face a mountain of debt and potential legal action, or shut down the company he had built from the ground up. With a heavy heart, he closed the doors of his trucking service. The good people he had employed lost their jobs. The trucks were sold off. His dream had turned to dust. He is now in the process of building a new company from the ashes, this time with our team of trusted, verified professionals. The lessons he learned were paid for at a painfully high price. The Hidden Costs of a “Cheap” Bookkeeper Our client’s story is a cautionary tale for every small business owner. The allure of saving money on professional services is strong, but the risks are profound. A bad bookkeeper can do more than just make a few errors; they can systematically destroy a business from the inside out. These are the crucial red flags he now advises every business owner to recognize: Protecting Your Business Before you entrust your finances to anyone, you must do your due diligence. Here’s what our client is doing differently with his new venture—and what we advise for all business owners: Ready to Safeguard Your Finances? Don’t wait until the IRS is at your door to get serious about your bookkeeping. At Fynlo, we combine expert accountants—many with backgrounds at top firms like Grant Thornton, BDO, and Baker Tilly—with cutting-edge software to ensure your books are accurate, compliant, and stress-free. Schedule your free call today and pave the way for a confident, mistake-free financial future. You may also like these articles:

15 Highest Paying Freelance Jobs

I was chatting with an ex-FAANG engineer at a co-working space the other day. He’d left Big Tech in 2019 to freelance full-time. I assumed he’d traded a cushy salary for a bit more freedom, but I was wrong. He’s making more money now and still ducks out for a Wednesday surf session whenever the waves are good. Stories like his aren’t rare anymore. The freelance economy has matured, and companies now view top contractors as mission-critical talent, not budget line items. According to Upwork’s Study, 38% of the U.S. workforce (about 64 million Americans) freelanced in 2023, and specialized roles regularly command triple-digit hourly rates. Below are 15 freelance careers that pay exceptionally well and give you the freedom to spend afternoons with family, jet off on a moment’s notice, catch the perfect swell—whatever your version of freedom looks like. Note: Because Sales Funnel Copywriting and Voice-Over services aren’t billed by the hour, they’ve been excluded from this chart. 1. Blockchain (Web3) Developer Blockchain is no longer a buzzword; it underpins billions of dollars’ worth of transactions in finance, supply chain, and even gaming. Even though the crypto market has seen its share of volatility and downturns, demand for skilled blockchain engineers remains strong, because companies still need private ledgers, supply‐chain tracking, and secure tokenization. From writing tamper‐proof smart contracts to auditing DeFi protocols for seven‐figure exploits, top‐tier engineers sit at the crossroads of money and math, so companies happily pay to keep them on speed-dial. Typical Rate: $50 – $150/hr Key Skill: Solidity, Ethereum, Hyperledger Fabric, cryptography, distributed systems 2. AI / Machine-Learning Consultant AI is red-hot, and every investor is hunting for the next breakthrough, so the prospects for skilled ML consultants are bright. Enterprises are scrambling to move from “AI pilot” to real ROI, but pre-trained models still need custom data, guardrails, and cost controls. Freelance ML pros step in to fine-tune LLMs, build anomaly-detection pipelines, and translate geek-speak into board-room slides. When a single algorithm tweak can save or earn millions, these specialists name their price. Typical Rate: $120 – $300/hr Key Skill: Python + PyTorch, TensorFlow, prompt engineering, data modeling 3. Cloud Architect/Engineer One mis-tagged S3 bucket can leak data, and one mis-sized cluster can torch $10K in a weekend. Large companies know that poor cloud setup risks both security breaches and massive unexpected bills, so they take cloud architecture very seriously. Architects who tame AWS, Azure, or GCP keep uptime high and costs low, guiding organizations through migrations and DevOps automation. Their invoices cost far less than the cloud horror stories they prevent. Typical Rate: $80 – $180/hr Key Skill: AWS/Azure/GCP certifications, Terraform, network security, virtualization 4. Cybersecurity Specialist A single breach now averages $4.88 M (IBM 2024). High-profile incidents like the Equifax breach and Colonial Pipeline hack have shuttered operations overnight. Ethical hackers and compliance experts harden networks, run red-team drills, and navigate audits—“Pay me five figures or pay ransomware double” clients wisely choose the former. Typical Rate: $80 – $160/hr Key Skill: Pen-testing toolkits, zero-trust architecture 5. AR/VR (XR) Developer Forget metaverse hype—healthcare training sims, virtual showrooms, and mixed-reality field guides are already mainstream. Companies without in-house Unity or Unreal talent tap freelancers to prototype fast and wow investors. From virtual home staging that helps real estate agents close deals more quickly to interactive factory maintenance guides that reduce downtime, XR applications drive real-world results. As hardware becomes more affordable and headsets more comfortable, demand for skilled AR/VR developers is only set to skyrocket. Typical Rate: $60 – $150/hr Key Skill: Unity-C# or Unreal C++/Blueprints, spatial UX 6. UX/UI Designer A clunky onboarding screen can bump churn 20%, while a friction-free flow can turn trial users into loyal customers. Senior designers create intuitive, user-friendly, and aesthetically pleasing digital interfaces—whether websites or apps—that guide users seamlessly through key actions. By blending psychology, aesthetics, and A/B testing data, they optimize every step of the user journey to maximize satisfaction and conversion rates. Their work has a direct impact on product adoption and revenue, making each pixel they design worth every dollar. Typical Rate: $40 – $100/hr Key Skill: Wireframing, prototyping (Figma, Sketch), user research, usability testing 7. Digital Marketing Strategist Anyone can boost a post; few can scale ad spend from $10K to $1 M per month while maintaining a 4× return on ad spend (ROAS). These strategists oversee every aspect of performance campaigns—from high-volume A/B creative testing to sophisticated attribution modeling that tracks exactly which ad led to a sale—and they pivot on a dime when platform algorithms change. By analyzing granular metrics and optimizing audience segments, they ensure every dollar of your marketing budget translates into measurable revenue and sustainable growth. Typical Rate: $50 – $100/hr Key Skill: Google Ads & Meta Blueprint certs, analytics (GA4), audience strategy 8. Sales Funnel Copywriter Words that sell are worth their weight in gold. Conversion copywriters and funnel architects craft the headlines, email sequences, and upsell offers that transform casual browsers into loyal buyers. They begin by conducting deep customer research—interviewing your ideal audience, analyzing what genuinely resonates, and then weaving persuasive prose that addresses pain points and triggers emotional responses. By layering strategic call-to-action placements and A/B testing different messaging, these professionals can triple conversion rates. When a $50K product launch balloons to $150K because of a winning sales page, clients happily share the upside—making stellar copywriting a high-stakes investment. Typical Rate: $0.25 – $1.00/word or $3K–$10K/funnel Key Skill: Persuasive copywriting, sales psychology, CRO techniques 9. Senior Video Editor / Motion Graphics Artist Short-form video was reported as having the highest ROI of any social media marketing strategy in 2024. Senior editors and motion graphics artists take raw footage and elevate it—splicing together narrative beats, applying color grading, and layering dynamic animations. Their work keeps viewers glued to screens: a product teaser with eye-popping transitions, a brand story punctuated by kinetic typography, or a tutorial that feels more cinematic than instructional. Because social platforms serve up short attention spans, these creators blend

5 Best States to Incorporate In and Why

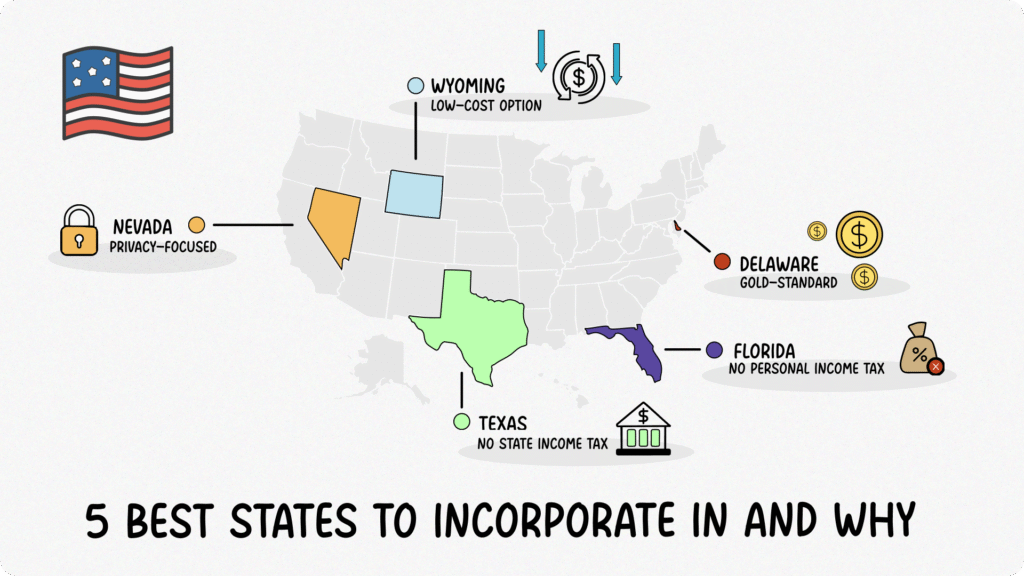

When I started my first small business, I remember staring at a blank screen, Googling “where should I incorporate?” I found conflicting advice, fees that seemed to change overnight, and legal jargon that made my head spin. Over time—after a few “oops” moments and some late-night research—I narrowed it down to five states that consistently offer the best mix of low costs, solid legal protections, and friendly environments for entrepreneurs. Here’s what I’ve learned, with real numbers (as of 2025) and a few personal notes about why these states stand out. Table of Contents Delaware: The Gold Standard for Big (and Small) Businesses “People joke that Delaware exists just so corporations can incorporate there—and it almost feels that way when you see how slick their system is.” Why Delaware? Fees (2025): If you budget about $540/year (minimum franchise tax + report), you’re covered. And if your business grows—say, you issue more shares or have a high par-value capital structure—you might pay more, but startups typically stay at the minimum. Personal note: My first LLC wasn’t in Delaware—it was in my home state. But after attending a startup accelerator and hearing investors talk about “Delaware C-Corp, please,” I re-formed there. I still recall breathing a sigh of relief when I realized investors are so comfortable with Delaware entities that legal due diligence becomes that much smoother. Wyoming: The Friendly, Low-Cost Option for Small Businesses “Think of Wyoming as the underdog—no one talks about it as much as Delaware, but it quietly checks all the right boxes for a lean, mean small-business machine.” Why Wyoming? Personal note: When I was a freelancer, I formed a single-member Wyoming LLC just because the yearly cost was so low. It felt thrilling to pay only $160 total each year and know my personal assets had a legal buffer. Nevada: Privacy-Focused with No Corporate Income Tax “Nevada is like Wyoming’s more opulent cousin—privacy protections, no state income tax, and a reputation as the ‘Florida of the West’ for tax benefits.” Why Nevada? Fees (2025): In total, expect around $875 in year one (incorporation + list + license). Subsequent years are $650 (license $500 + list $150). I know that sounds steeper than Wyoming, but if privacy and zero state tax on profits matter, many entrepreneurs find Nevada worth the up-front costs. Personal note: A colleague once told me, “If you live in California but want to keep your taxes honest, move to Nevada for your mental health.” He wasn’t wrong—no state income tax means one fewer headache at tax time. Texas: No State Income Tax + Seller’s Market for Services “Texas is booming—no state income tax, a thriving entrepreneurial scene, and a sense of ‘everything’s bigger in Texas,’ including opportunities.” Why Texas? Personal note: I once thought I’d set up shop in California, but I cringed at that 13.3% top-bracket personal rate on top of corporate taxes. Texas felt like a breath of fresh air—zero state income tax, and Austin’s startup vibe makes you feel like anything’s possible. Florida: No Personal Income Tax + Moderate Corporate Tax “Florida is that friend who loves to chill in flip-flops but still knows how to hustle—no personal income tax, solid consumer market, and a growing tech ecosystem.” Why Florida? Personal note: I spent a summer in Miami Beach brainstorming a business plan on the sand. The idea of paying zero state income tax gave me the energy to work late nights—and if you’ve ever tried running spreadsheets in 90-degree heat, trust me, you’ll appreciate anything that saves you a percentage point of tax. Things to Consider When Choosing a State TL;DR A quick overview of the five best states to incorporate in, plus why they might be a fit for you: State Formation Fee Annual Cost Corporate Tax Personal Tax Key Benefits Delaware $89 (C-Corp) $400 franchise tax + $50 report None on C-Corp profits None on pass-through – Chancery Court– Flexible corporate laws– Investor-friendly Wyoming $100 (LLC) $60 annual report None None – Lowest fees– Strong privacy & asset protection– No state income tax Nevada $75 (C-Corp) $500 business license + $150 list None None – Robust privacy– No corporate/personal income tax– Business court by 2026 Texas $300 (Corp) Exempt under $1.23M revenue; otherwise 0.375%–0.75% margin tax 0.375%–0.75% (varies) None – No personal income tax– Large business ecosystem– Franchise tax exemption under $1.23M Florida $70 (C-Corp) $150 annual report 5.5% None – No personal income tax– Growing tech hubs– Moderate corporate tax Final Thoughts There’s no one-size-fits-all “best state”—it really depends on your budget, growth plans, and tolerance for paperwork. When I first started, the difference between $60/year (Wyoming) and $540/year (Delaware) felt huge. But as my business matured and I talked to investors, it became clear that Delaware could save me weeks of legal back-and-forth. Meanwhile, friends who run lean e-commerce stores from home still swear by their $160/year Wyoming LLCs. In the end, pick the state that aligns with your current priorities: cost, privacy, investor confidence, or community. And remember, you can always form in one state and later register as a foreign entity in another (it’s called “qualifying” to do business in your home state). That’s exactly what many growth-stage startups do: incorporate in Delaware, then register in their home state so they can open a bank account, hire W-2 employees, and sign leases without legal headaches. I hope this guide helps you sleep a little easier as you choose your business’s “home.” Wherever you decide to incorporate, know that every entrepreneur—myself included— started exactly where you are right now: staring at a blank filing form, hoping they made the right choice. Need Help with Your Accounting? At Fynlo, we know every state has its own quirks—whether it’s Delaware’s Chancery Court, Wyoming’s low fees, Nevada’s privacy rules, Texas’s franchise tax, or Florida’s corporate rate. Our expert team can handle your bookkeeping, annual filings, and state-specific tax planning no matter where you incorporate. Schedule a call today, and let us make sure your business stays

The Fynlo Guarantee: Accurate, On-Time, and Stress-Free Accounting

Running a freelance gig or small business means juggling dozens of responsibilities, from marketing and client work to operations and finances. At Fynlo, we take accounting off your plate with our Fynlo Guarantee: every client receives bookkeeping and tax services that are Accurate, delivered On-Time, and completely Stress-Free. 1. Accurate Records—Every Time Even minor mistakes can lead to penalties or missed deductions. Accuracy is non-negotiable: Result: Financial statements you can trust, helping you maximize deductions and maintain compliance. 2. On-Time Delivery—And Smarter Decisions Through Clarity Late reports can derail cash-flow plans, loan applications, or investor pitches. With Fynlo: Result: You receive up-to-date financials exactly when expected, plus the strategic clarity to guide your next move. 3. Stress-Free Experience—Focus on What Matters Worrying about bookkeeping drains time and energy. Fynlo makes accounting seamless: Result: Zero late-night “where did that charge go?” moments. Instead, you stay focused on clients and growth. Meet the Team Behind the Guarantee Our combined expertise, backed by best-in-class technology, ensures your accounting is both personalized and scalable. How to Get Started Unlock peace of mind and a clear financial roadmap. Experience Accurate, On-Time, and Stress-Free accounting with Fynlo. Book your free discovery call today.

11 Questions to Ask Before Hiring an Accountant

Table of Contents The Day I Fired Myself It was 1 a.m. on a Tuesday in April. My online boutique had just had its best quarter ever, but I wasn’t celebrating. Instead, I was surrounded by a sea of crumpled receipts, staring at a spreadsheet that looked more like abstract art than a financial statement. I was trying to figure out if I could depreciate my new shipping label printer. I remember thinking, “I spent four years building this brand I love, and now I’m losing sleep over a printer.” That was the night I fired myself… from being my own accountant. For so many freelancers and small business owners in the USA, this story is familiar. We start out wearing all the hats: CEO, marketer, customer service rep, and, yes, bookkeeper. But there comes a point where the time and stress of managing the finances cost more than the money you think you’re saving. The Federation of Small Businesses revealed that small business owners spend up to 44 hours per year on tax compliance alone. That’s a full work week you could be spending on generating sales, creating your product, or just recharging. Hiring an accountant isn’t admitting defeat; it’s making a strategic investment in your success and sanity. But how do you find the right person? It’s not just about finding someone who can file your taxes. It’s about finding a financial partner. To help you find that partner, here are 11 essential questions to ask your potential candidates. 11 Questions to Ask Before Hiring an Accountant 1. Do you have experience with other businesses like mine? The financial landscape of a freelance graphic designer is vastly different from that of a small e-commerce shop or a local restaurant. An accountant who specializes in your field will already be familiar with the specific deductions, tax challenges, and revenue models unique to your industry. They won’t be learning on your dime. Ask them to give examples of how they’ve helped similar businesses. 2. What are your credentials (e.g., CPA, EA)? These letters represent very different skill sets. Knowing their designation tells you exactly where their expertise lies. 3. Who will be my main point of contact? At larger firms, you might meet with a senior partner initially, but your day-to-day work could be handled by a junior associate. There’s nothing wrong with this model, but you need to know who you’ll be speaking with regularly. Building a relationship with the person who is actually in your books is crucial for trust and clear communication. 4. How do you structure your fees? Why it Matters: There’s no single answer here, so you need to find what works for you. Common structures include: A retainer model is often preferred by business owners who want predictable costs and ongoing access to advice without worrying about getting a surprise bill for every phone call. 5. What specific services are included in your fee? This is arguably the most important question to avoid future misunderstandings. Does their fee include just the annual tax return? Or does it also cover quarterly estimated tax calculations, bookkeeping cleanup, payroll processing, and responding to tax notices? Get a detailed list. You need to be comparing apples to apples when you evaluate different accountants. 6. What accounting software do you prefer to work with? The days of the shoebox of receipts are over. Modern accounting live in cloud tools such as QuickBooks, Xero, Wave, or Fynlo. You need an accountant who is proficient with your current system or can seamlessly migrate you to a better one. Their comfort with technology is a good indicator of their overall efficiency. 7. Are you available for questions throughout the year? Your business doesn’t just happen during tax season. You might have a question about a major purchase in June or need to make a hiring decision in October. You want an accountant who sees themselves as a year-round advisor, not just a once-a-year tax preparer. Their answer will tell you a lot about their service philosophy. 8. How would you describe your approach: are you focused on historical compliance or proactive planning? A good accountant keeps you compliant and makes sure your taxes are filed correctly. A great accountant looks ahead. They’ll come to you with ideas for tax savings, help you plan for future growth, and advise on strategies to improve your cash flow. You’re looking for a proactive partner, not a financial historian. 9. Can you represent me in the event of an IRS audit? While IRS audit rates for small businesses are relatively low, they are not zero. If you are ever audited, it can be an incredibly stressful and time-consuming process. CPAs and EAs have unlimited representation rights, meaning they can represent you before the IRS on any matter. Knowing you have an expert in your corner provides invaluable peace of mind. 10. From your experience, what is the biggest financial mistake you see business owners in my position make? This question gives you a glimpse into their expertise and proactive mindset. Their answer will reveal how well they understand the common pitfalls of your industry. It also opens the door for them to provide immediate value and show you how they can prevent you from making those same mistakes. 11. What information do you need from me to get started? A professional accountant will have a clear, organized onboarding process. Their answer to this question will demonstrate their level of organization and set clear expectations for the working relationship. It shows they have a system and are ready to get to work. Finding Your Perfect Match Choosing your accountant isn’t just ticking boxes, it’s about forging a trusted partnership. Take the time to shortlist candidates, interview them, compare answers side by side, and go with the professional you trust. At Fynlo, we understand the challenges of financial management firsthand. That’s why we pair you with seasoned professionals who speak your language. Our junior accountants bring over five years of experience, while our senior accountants boast

Why Bookkeeping Isn’t Just for Big Companies

I still remember the first time I called myself a “business owner.” I’d just launched my Etsy shop selling handmade candles, and I felt unstoppable—until tax season hit. My “bookkeeping” was a pile of crumpled receipts in a desk drawer and a bank account I checked with one eye closed, hoping I hadn’t overspent. When I realized I’d missed $900 in deductions and owed an extra $400 because I hadn’t tracked my expenses, I felt crushed at my desk. That moment taught me something I wish I’d known sooner: bookkeeping isn’t just for corporate giants with skyscraper offices. It’s for freelancers, side hustlers, and small business owners like me—and you. If you’re a freelancer designing websites or running a small bakery, you might think bookkeeping is too complex or unnecessary for your one-person show. But it’s not about being “big”—it’s about taking control of your finances. The hard truth is, neglecting your books is one of the quickest ways to watch your dream crumble. It’s not about becoming a math whiz overnight; it’s about understanding the financial heartbeat of your business. And for the 75 million freelancers in the U.S., and the millions more small business owners, that heartbeat can be the difference between thriving and just surviving. Table of Contents The Sobering Numbers Behind the Dream We all love a good success story, but it’s crucial to acknowledge the reality. According to the Bureau of Labor Statistics, about 20% of new businesses fail within the first two years. Dig a little deeper, and a staggering 82% of small business failures are due to poor cash flow management, as reported by SCORE. Think about that. It’s not necessarily a bad product or a lack of passion that sinks the ship. It’s running out of money. It’s not knowing where your money is going, who owes you, or when your next big expense is due. That’s where bookkeeping makes its quiet, heroic entrance. 5 Ways Bookkeeping Empowers Freelancers and Small Businesses 1. Slash Your Tax Bill (Legally) Detailed expense tracking turns everyday costs into legit write-offs. By assigning each transaction to categories like office rent, utilities, software subscriptions, professional fees, and business mileage, you ensure nothing slips through the cracks. Many pass-through businesses qualify for the Qualified Business Income deduction, shaving up to 20% off taxable income. For instance, on $100,000 net profit, that’s a $20,000 deduction—potentially reducing your federal tax liability by around $5,000 at a 25% bracket . Add retirement-plan contributions (up to $23,000 for a Solo 401(k)) and self-employed health-insurance premiums, and you can stack multiple tax-saving strategies—all made simple when your books are up to date. 2. Stop Cash-Flow Surprises Profit on paper doesn’t always equal cash in the bank. This distinction is critical: a business might show a profit, but if customers aren’t paying their invoices promptly, cash flow can still be a major problem. In fact, 46% of small businesses seeking financing did so just to smooth out cash-flow bumps. To stay ahead of shortfalls, carve out a weekly bookkeeping slot and: By making these three steps routine, you catch cash leaks before they become full-blown crises—and keep your bank balance as healthy as your bottom line. 3. Make Choices That Grow Your Business Real-time dashboards turn raw numbers into actionable insights. With up-to-the-minute profit-and-loss, balance-sheet, and cash-flow reports, you can: Don’t just take our word for it—here’s what the numbers say. According to a 2024 QuickBooks survey, 95% of growing small businesses say integrated, automated accounting systems are critical to scale, yet the same percentage struggle with manual data entry. Clean books eliminate guesswork, so you invest with confidence. 4. Get Ready for Loans or Investors Opportunities to expand—or the need for capital to tackle unexpected challenges—can arise at any moment. When they do, financial readiness is non-negotiable. Banks, agencies such as the U.S. Small Business Administration (SBA), and potential investors will ask for clear, accurate statements to assess your risk and viability. Keep these documents up to date and on hand: Lenders and investors often make decisions within days; messy or incomplete records can stall or even derail your application. By maintaining clean books, you shorten approval timelines, minimize follow-up questions, and enter negotiations from a position of strength. 5. Reduce Financial Uncertainty and Stress Messy finances weigh you down. Uncertainty about your cash position and looming deadlines fuels anxiety. In fact, 49% of small-business owners report their mental health has suffered from the stress of managing their finances. The good news? You don’t need hours of work to turn that around. By carving out just 15 minutes each week to update your books—assigning transactions to the right categories, reconciling recent bank activity, and glancing at a one-page financial dashboard—you’ll eliminate nasty surprises from unexpected tax bills or overdrafts. Over time, this simple, predictable habit builds genuine confidence in your money management, frees up mental bandwidth to focus on your clients and creativity, and replaces financial dread with clear, calm control. “The journey of a freelancer or a small business owner is one of passion, grit, and a whole lot of heart. Don’t let the fear of numbers hold you back from building the thriving business you deserve. Replace the shoebox approach with organized records and gain the clarity and confidence that come from a clear view of your finances. Your future self will thank you for it.” Getting Started It’s easier than you think. You don’t need to be a certified public accountant to get your books in order. Here are a few simple steps to get you started: > Schedule your free discovery call < Further Reading Continue your learning journey with these related resources:

What is the Delaware Franchise Tax? Tax Calculation and Payment Process Explained

If you’re a freelancer or small business owner with a registered entity in Delaware, you’ve likely heard of the Delaware Franchise Tax. Don’t let the name intimidate you. It’s not a tax on your income or profits, but rather a fee you pay to the state of Delaware for the privilege of having your business registered there. Think of it as an annual maintenance fee for your business entity. This guide will break down everything you need to know about the Delaware Franchise Tax in simple, easy-to-understand terms. Table of Contents Who Needs to Pay the Delaware Franchise Tax? Any business entity registered in Delaware is required to pay this tax. This includes: Note: Exempt domestic corporations (e.g., non-profits) are not required to pay the tax but must still file an annual report (and pay the $50 report fee). Fast Facts & Data (Sources: Delaware Division of Corporations, 2023 Annual Report) Due Dates: Mark Your Calendar! Entity Type Tax Due Report Due Penalty for Late Filing C-Corporations $175–$200K March 1 $200 + 1.5% interest/month on unpaid LLCs, LPs, GPs $300 June 1 $200 + 1.5% interest/month on unpaid How to Calculate the Delaware Franchise Tax Delaware offers two ways to calculate your corporate franchise tax—Authorized Shares or Assumed Par Value Capital—and you’ll pay the lower amount. When you file on the official Delaware Division of Corporations website, it defaults to Authorized Shares, so run the Assumed Par Value Capital calculation yourself to compare. For LLCs and Partnerships: A Simple Flat Fee For LLCs, LPs, and GPs, the calculation is straightforward. It’s a flat annual fee of $300. For Corporations: Two Calculation Methods For corporations, the calculation is more complex. Delaware provides two methods to calculate your franchise tax. You are permitted to pay the lower of the two amounts. When you go to pay your tax online, the state’s system will default to the Authorized Shares Method, so it’s worth taking the time to calculate your tax using both methods. Here is a step-by-step breakdown of the calculation: Step 1 – Calculate the “Assumed Par”: Divide your Total Gross Assets by your Total Issued Shares. Carry the result to six decimal places. This gives you the “assumed par.” Step 2 – Calculate the “Assumed Par Value Capital”: Multiply the “assumed par” you just calculated by the Total Number of Authorized Shares. Step 3 – Calculate the Tax: The tax rate is $400 for every $1,000,000 of Assumed Par Value Capital. If your Assumed Par Value Capital is less than $1,000,000, you will divide it by 1,000,000 and then multiply by $400. If it’s over $1,000,000, you round up to the next million. Since the minimum tax for this method is $400, your final tax due using the Assumed Par Value Capital Method would be $400. By using the Assumed Par Value Capital Method and paying the minimum of $400 (plus the $50 annual report fee), a corporation in this example would save a significant amount compared to the Authorized Shares Method, which would have resulted in a much higher tax bill. How to Pay Your Delaware Franchise Tax The state of Delaware requires online payment for the franchise tax and annual report filing. Here’s how to do it: By understanding these simple blocks—and knowing where to look on the official Delaware Division of Corporations website—you’ll stay in good standing and keep your focus on growing your business. Take the Next Step Ready to take the hassle out of your business finances? At Fynlo, we specialize in helping freelancers and small business owners—just like you—stay compliant, organized, and focused on growth. From managing your Delaware Franchise Tax filings to crafting custom financial dashboards, our team acts as your in-house finance department—without the overhead. Schedule your free discovery call Continue your learning journey with these related accounting insights:

LLC vs Inc.: Everything You Need to Know

Choosing a business structure is like picking the right tool for a job—each has its strengths, quirks, and costs. For new entrepreneurs, the Limited Liability Company (LLC) and Corporation (Inc.) are two of the most popular options in the U.S. Both protect your personal assets, but they differ in taxes, management, ownership, and paperwork. This guide breaks it all down in plain English and a clear comparison table, so you can choose the structure that fits your business dreams. Let’s get started! Table of Contents What is an LLC? A Limited Liability Company (LLC) is like bubble-wrap for your personal assets: it shields them from business debts and lawsuits while remaining simple to run. LLC owners, called members, enjoy liability protection with fewer formalities than a corporation. To form an LLC, you file Articles of Organization with your state’s Secretary of State and pay a fee—usually between $50 and $500 (e.g., $50 in Colorado; $500 in Massachusetts). While an Operating Agreement isn’t required in every state, it’s a smart way to spell out ownership, profit splits, and decision-making rules. Fun Fact: LLCs existed in limited form starting in the late 1970s, but their popularity has exploded since the mid-1990s. In recent years, LLCs have become the most common structure chosen by small-business owners, reflecting their appeal to modern entrepreneurs. What is an Inc. (Corporation)? A corporation is a separate legal person with shareholders, a board, and more built-in formality. You file Articles of Incorporation (fees range from $90 in Delaware to $125 in New York), adopt bylaws, and hold annual shareholder and board meetings. Corporations come in two tax flavors: Fun Fact: Although corporations account for roughly 8% of all business tax returns, they generate about 60% of total U.S. business receipts, underscoring how most revenue still flows through corporate entities. Key Differences at a Glance Below we compare five critical areas: liability protection, taxation, management, ownership, and compliance. Comparison Table: LLC vs. Inc. Factor LLC Inc. (C Corp) Inc. (S Corp) Liability Members protected unless they commit fraud/negligence. Courts pierce veil very rarely. Shareholders protected. Veil-piercing more common than with LLCs. Same as C Corp. Taxation Pass-through (Schedule C/K-1); can elect C/S Corp status; Members pay self-employment tax on profits by default. Double taxation: 21% corporate tax + dividend tax (0%–20%). Pass-through; no self-employment tax on distributions; strict limits. Management Flexible: member-managed or manager-managed; no board or meetings required. Formal: board + officers; annual meetings and minutes mandatory. Same as C Corp. Ownership Unlimited members; no stock; transfers need approval. Unlimited shareholders; stock easy to sell; ideal for VC. Max 100 U.S. shareholders; one stock class. Compliance Minimal: annual report (fees $0–$500) and basic bookkeeping. High: adopt bylaws, hold annual meetings and minutes; several thousand dollars per year. High: same formalities as C Corp plus S-Corp eligibility upkeep; several thousand dollars per year. Best For Small businesses, freelancers, hands-on owners. Scalable startups, VC-funded ventures, public companies. Small firms wanting pass-through taxation with corporate structure. 1. Liability Shield Both LLCs and corporations protect personal assets, but the strength of that shield depends on following the rules. 2. Taxes Below is a condensed overview of how each structure is taxed, focusing on key points a newcomer needs to know. LLC (Default Pass-Through): LLC Electing S-Corp Status (Optional): C-Corp (Traditional Corporation): S-Corp (Standalone Election): Taxation Summary Table: Structure Entity Tax Rate Owner Tax Treatment Self-Employment Tax on Profits? Key Notes LLC (Default) 0% (pass-through) Owner reports on Schedule C or K-1 → Form 1040 Yes, 15.3% on net earnings Single-member uses Schedule C; multi-member files 1065 → K-1. QBI deduction up to 20%. LLC → S-Corp 0% (pass-through) Owner takes reasonable salary (W-2); rest is dividends Only on salary (FICA) Savings vs. 15.3% if distributions > salary; requires payroll setup. LLC → C-Corp 21% Profits taxed at 21% → dividends taxed again (0%–20%) — Potential double taxation; can retain earnings; access to corporate credits. C-Corp (Standalone) 21% Dividends taxed at 0%–20% on shareholders — Traditional corporate structure; double taxation. S-Corp (Standalone) 0% (pass-through) Owner salary (W-2) + distributions via K-1 Only on salary (FICA) Must meet eligibility (≤ 100 U.S. shareholders, one stock class). 3. Management Style 4. Ownership Flexibility 5. Compliance & Cost LLC C Corp S Corp Pros and Cons of LLC vs. Inc. LLC Pros LLC Cons Inc. Pros Inc. Cons Which Should You Choose? The choice between an LLC and Inc. depends on your business goals, size, and growth plans: Need Help Deciding? At Fynlo, we understand that choosing the right business structure can feel overwhelming. Our accounting software and expert team are here to simplify the process, from formation to tax planning. Whether you’re leaning toward an LLC or a corporation, we can help you navigate the paperwork, optimize your taxes, and stay compliant. Ready to get started? Schedule a call with Fynlo today to discuss your business goals and find the perfect structure for your success. Let’s build your dream business together! You may also like these articles:

5 Ways to Avoid IRS Tax Fines

We all love the freedom and flexibility that comes with being our own boss, but at the same time, the thought of the IRS lurking can create a sense of unease. The good news is, with a little foresight and smart planning, you can drastically reduce your chances of incurring those pesky penalties. According to New York Post, the IRS levied $7 billion in tax penalties in 2023, so you’re not alone if you’ve ever felt the sting. But for freelancers and small business owners, these fines can hit particularly hard. Say no to tax fines, and don’t let the IRS ding your wallet. Let’s dive into 5 practical strategies to keep your hard-earned cash safe from the penalty box. Table of Contents 1. Master Estimated Taxes For most freelancers and small business owners, your income isn’t subject to traditional W-2 withholding. That means you’re responsible for paying your income and self-employment taxes throughout the year via estimated tax payments. To avoid underpayment penalties, the IRS requires you to pay either: These are known as “safe harbor” rules. Key Information: 2. File On Time, Every Time This might sound obvious, but the “failure to file” penalty is one of the most common fines issued by the IRS. The failure-to-file penalty is 5% of the unpaid taxes for each month or part of a month your return is late, up to a maximum of 25%. Key Information: 3. Keep Impeccable Records Think of good record-keeping as your indispensable safety net. The IRS relies on accurate information, and if your numbers don’t add up, or if you can’t back up your deductions, you’re inviting trouble. Self-employed individuals, particularly those filing Schedule C, face heightened scrutiny and are more likely to be audited. An audit can be triggered by seemingly simple things like math errors, disproportionately high deductions compared to your income, or a mismatch between what you report and what third parties (like clients issuing 1099s) report to the IRS. In fact, underreporting your income by more than 25% can extend the IRS’s audit window to six years. What to keep track of: 4. Report All Your Income This is a big one for freelancers. The IRS receives copies of 1099-NEC forms from clients who paid you $600 or more. Failing to report this income can trigger audits and penalties. The IRS computer systems automatically compare the information they receive with what you report on your return. Key Information: 5. Know Your Relief Options Life happens, and sometimes, despite your best efforts, you might miss a deadline or make a mistake. The IRS isn’t entirely without mercy, and they do offer penalty relief options. By taking these proactive steps and staying organized, freelancers and small business owners can navigate the tax landscape with confidence, avoiding unnecessary fines and keeping more of their hard-earned money where it belongs: in your pocket, fueling your entrepreneurial journey! Need assistance with your accounting or bookkeeping? Fynlo offers professional services tailored for your business. Schedule a call with us to see how we can simplify your financial life. Further Reading Continue your learning journey with these related accounting insights: