5 Fastest Growing Ecommerce Companies in 2026

Americans now spend more on e-commerce than the GDP of Denmark and these 5 innovative companies are cashing in. Forget Amazon clones. These disruptors are creating entirely new ways to shop. 1. Whatnot – Livestream Shopping Marketplace Imagine scrolling through TikTok, but instead of just watching, you can instantly buy what you see. That is Whatnot. This platform brings the thrill of live auctions to your phone, where sellers host real-time video streams to showcase everything from rare Pokémon cards to sneakers, vintage toys, and luxury handbags. Unlike traditional marketplaces like eBay or Facebook Marketplace, Whatnot makes shopping entertaining. Sellers hype up their products like game show hosts, buyers chat and bid in real time, and rare items can sell for thousands in minutes. It is QVC meets social media and it is no longer just for collectors. Think about that for a second. The average Whatnot user spends 95 minutes per day on the app. That is more than YouTube. More than TikTok. When people stay that long, they buy things. In October 2025, Whatnot raised $225 million in a Series F round, more than doubling its valuation from $5 billion at the start of the year to $11.5 billion by the end of it. Platform GMV hit $8 billion for the full year, up from $3 billion in 2024. Revenue reached an estimated $1 billion. The company ranked as the number one Shopping app in both the U.S. and U.K. App Stores, and generated over $100 million in live sales on Black Friday 2025 alone. The platform is also expanding fast into new categories. Beauty grew 791% year-over-year. Electronics grew 444%. Women’s fashion grew 223%. This is no longer a niche collectibles site; it is becoming a mainstream shopping destination built around entertainment. Key Figures: Why it works: Live auctions create urgency that static product pages simply cannot replicate. When you can see a seller’s face, hear the excitement in the room, and watch a countdown timer, buying feels different. That psychology drives conversion rates that traditional ecommerce can only dream about. 2. ShopMy – Creator-Affiliate Commerce Platform Ever click an Instagram link to buy a product? There is a good chance ShopMy powered it. This platform helps influencers monetise their audiences by turning their posts into shoppable storefronts. Brands like Nike, Lululemon, Gucci, and Sephora use ShopMy to track which creators actually drive sales, not just likes. Meanwhile, creators get a commission on every purchase without needing a clunky Shopify store. It is a clean arrangement: brands pay for performance, creators get rewarded for taste, and shoppers discover products through people they actually trust. What makes ShopMy different from older affiliate platforms is the quality filter. This is not a platform for any influencer with a discount code. It is built around vetted tastemakers, which keeps the product recommendations credible and the conversion rates high. Brands on the premium end of the market, the ones that would run a mile from a generic influencer campaign, are lining up to use it. As affiliate revenue scales, creators must treat this income like a true business. If you are monetising your audience, our guide to tax deductions for independent professionals can help you protect those earnings. ShopMy raised $70 million in a Series C round in October 2025 at a $1.5 billion valuation, officially becoming a unicorn five years after founding. Revenue grew 200% year-over-year to $80 million, up from $27 million in 2024 and just $4 million in 2023. The platform now facilitates over $1 billion in annual sales across 185,000+ vetted creators and 1,200+ brand partners. In August 2025, ShopMy launched Circles, a consumer-facing shopping app built around curated product feeds. Within months, users had created 30,000+ Circles and wishlisted over 150,000 products. The company is no longer just a backend tool for brands; it is becoming a shopping destination in its own right. Key Figures: Why it works: Shoppers are tired of being sold to by algorithms. When a creator they follow and trust recommends a product, it feels like advice from a friend, not an ad. ShopMy has built the infrastructure that makes that trust transaction scalable, measurable, and profitable for everyone involved. 3. Little Spoon – Direct-to-Consumer Baby and Kids’ Food Parents are tired of processed baby food filled with preservatives. Little Spoon delivers fresh, organic meals for babies and toddlers, shipped cold and ready to eat. Their Babyblends line covers first foods for infants, while their Plates range for toddlers includes meals like turkey meatballs and quinoa bowls. They also offer vitamins and probiotics under their Boosters line. In March 2026, they launched organic infant formula, making them a genuine one-stop shop for children’s nutrition from birth through the big kid years. Here is what the traditional baby food industry never figured out: millennial parents do not trust what they cannot read on the label. They grew up Googling ingredients and questioning everything. Little Spoon built its entire brand around that scepticism, making transparency a feature rather than a legal requirement. Little Spoon has raised $90 million in total funding across five rounds and has delivered meals to over 300,000 families since launch. In 2025, the company became the first and only baby food maker in the U.S. to publicly set EU-aligned safety standards and share test results for heavy metals, pesticides, and plasticisers. That is an unusually bold move in a category where most brands stay quiet on ingredient testing. It paid off in brand trust. The subscription model is the engine behind the business. Parents who sign up once tend to stay for years, moving from Babyblends to Plates to the Boosters vitamin line as their children grow. That lifetime value per customer is what makes the unit economics work. Key Figures: Why it works: The subscription model creates predictable revenue and deep customer loyalty. Once a parent trusts a brand with their baby’s food, switching costs are high. Not financial switching costs, emotional ones. That is a powerful moat. 4. Market Wagon – Online Farmers Market Farmers markets are amazing, but who has time to go every weekend? Market Wagon brings local farms to your doorstep. You can order grass-fed beef, organic eggs, artisan cheese, and fresh-picked produce, all from small farmers in your area. They handle delivery, so you get farm-fresh food

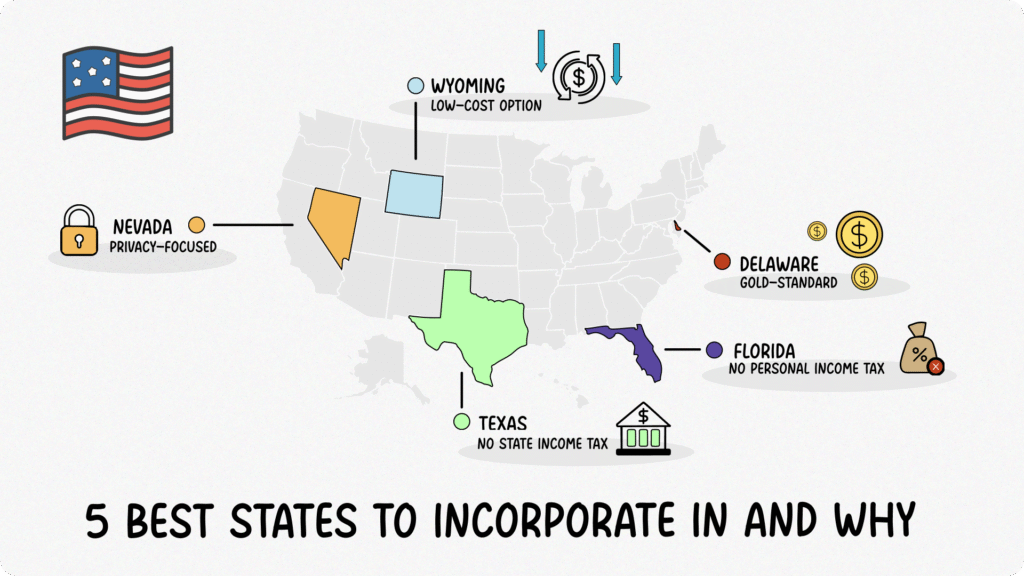

5 Best U.S. States to Incorporate In: 2026 Tax & Legal Guide

Choosing where to legally anchor your business is a major decision that impacts your tax liabilities, how easily you can manage your company, and your long-term legal protection. Many entrepreneurs default to filing in their home state, only to realize later that their funding strategies or business models would have been better served by a different jurisdiction. There is no single “best” state for every business. The right choice depends entirely on your capital structure, privacy requirements, and where you physically operate. This guide breaks down exactly how Delaware, Wyoming, Nevada, Texas, and Florida offer distinct advantages for corporate formation, looking beyond basic filing fees to examine the underlying legal and tax frameworks that impact your growth. In this Article Key Factors in Selecting a State When evaluating a state for incorporation, you need to look at four primary financial and regulatory angles. The right balance depends entirely on your specific business priorities. Comprehensive State-by-State Analysis Delaware: The Institutional and Venture Capital Standard Delaware differentiates itself not by being cost-effective, but by acting as the universally accepted legal framework for outside investors. While other states pitch low fees, Delaware focuses on corporate flexibility, maximizing options for complex equity structures, and offering unparalleled legal predictability. This is why tech giants like Alphabet (Google), Amazon, Apple, and high-growth scale-ups like Stripe and Airbnb choose Delaware. Note on Delaware LLCs vs. Corporations: If you form an LLC instead of a corporation in Delaware, you owe a flat $300 annual tax due June 1 each year instead of the franchise tax, and you do not need to file an annual report. Wyoming: Low-Cost Maintenance and Administrative Simplicity Wyoming differentiates itself by offering the leanest, most affordable corporate maintenance structure in the country. Where Delaware targets venture-backed corporations, Wyoming targets solopreneurs, digital nomads, and bootstrapped e-commerce brands looking for solid asset protection without ongoing paperwork burdens. Nevada: Premium Privacy and Robust Asset Protection Nevada differentiates itself by actively shielding corporate leadership teams from public visibility. It combines a zero-tax structure with some of the strictest operational privacy rules in the United States. Texas: Scaling Infrastructure and High-Volume Local Markets Texas differentiates itself by being an operational powerhouse rather than a passive filing haven. It is built for growing agencies, technology scale-ups, and companies that intend to establish a physical footprint, hire local talent, and capture market share within a massive domestic economy. Important Compliance Note: Even if your revenue is below the $2.65 million threshold and you owe zero franchise tax, you are still required to file a Public Information Report with the Texas Comptroller by May 15 each year. Skipping this filing triggers a $50 penalty. Florida: Balanced Taxation and Regional Ecosystem Growth Florida differentiates itself by offering an ideal tax environment for business owners who prioritize personal income retention. It strikes a highly attractive balance with a predictable low-rate corporate tax and a completely tax-free landscape for individual income. TL;DR: Summary Matrix State Primary Strategic Advantage Best Suited For Top Operational Priority Delaware Institutional credibility, VC readiness, advanced corporate courts Venture-backed startups, high-growth entities, complex boards Raising Outside Capital / IPO Roadmap Wyoming Maximum affordability, asset shielding, low paperwork Solopreneurs, e-commerce, bootstrapped digital companies Minimizing Upkeep & Protecting Solo Assets Nevada Strict leadership anonymity, asset protection, business courts Privacy-conscious owners, asset managers, mid-size firms Maximum Operational Privacy Texas Massive regional market, zero franchise tax under $2.65M revenue Agencies, regional employers, manufacturing, tech scale-ups Scaling Physical Infrastructure & Local Hiring Florida Balanced founder tax environment, high consumer market access Profitable brands, regional agencies, expanding tech hubs Founder Wealth Maximization & Distribution Critical Questions Before Filing To avoid inadvertently triggering double-compliance obligations, analyze these operational realities prior to registration: Final Thoughts Every entrepreneur starts exactly where you are right now: staring at a blank filing form, weighing numbers, and trying to predict the future layout of their company. If you find yourself stuck in analysis paralysis, simplify your decision by looking at your business model’s immediate 12-month horizon: Once you have identified the state that aligns with your current priorities, your next steps are straightforward: secure a registered agent in that jurisdiction, file your Articles of Organization or Incorporation, and obtain your federal EIN. One final reminder that applies regardless of which state you choose: incorporating in a different state from where you actually live and operate does not eliminate your home state tax obligations. You will almost certainly need to register as a foreign entity in your operating state, meaning you pay fees and meet compliance requirements in both. Factor this into your total cost comparison before making a final decision. By taking the time to match your state selection to your actual operational strategy today, you protect your personal assets and build a clean foundation for wherever your business takes you next. For a visual breakdown of how these specific legal and financial trade-offs operate side-by-side, this Wyoming LLC vs. Delaware LLC video provides a practical analysis of ongoing maintenance fees, asset protections, and exact filing pathways to help you choose the correct entity structure. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

15 Highest Paying Freelance Jobs in 2026 (With Real Rates, Growth Stats, and Exactly Where to Start)

I was chatting with an ex-FAANG engineer at a co-working space the other day. He had left Big Tech in 2019 to freelance full-time. I assumed he had traded a cushy salary for a bit more freedom, but I was wrong. He is actually out-earning his old salary now, and the real win is that he can trade his standing desk for a surfboard on a Wednesday morning without checking a calendar or asking for permission. Stories like his are not rare anymore. The freelance economy has matured, and companies now view top contractors as mission-critical talent, not budget line items. According to industry research from April 2026, an estimated 70 to 73 million workers, approximately one third of the labour force, engage in independent or gig work in some capacity. At the upper end of the market, highly specialized roles regularly command triple-digit hourly rates. Below are 15 freelance careers that pay exceptionally well and give you the freedom to spend afternoons with family, jet off on a moment’s notice, catch the perfect swell, or whatever your version of freedom looks like. In this Article Is 2026 Actually a Good Time to Go Freelance? The short answer: it depends entirely on what you do. AI is the elephant in the room, and it cuts both ways. On the threat side, entry-level creative and writing work has been hit hard. If you were charging $30/hr for basic blog posts or simple graphic design, that pipeline has thinned considerably. Junior roles that once served as stepping stones into freelance careers are disappearing faster than anyone expected, and that is a genuine problem worth acknowledging. But here is where it gets interesting. The same AI wave that is eroding entry-level work is creating an acute shortage of senior specialists who can work with it. Enterprises can now prototype faster and cheaper than ever before, but someone still needs to validate the output, fix what the model gets wrong, and translate technical results into business decisions. That someone is increasingly a senior freelance specialist brought in on contract. The people building AI pipelines, auditing AI security vulnerabilities, and advising boards on AI strategy are in higher demand today than they were two years ago. There is also a structural tailwind that has nothing to do with AI. Companies are leaner than ever. Hiring a full-time specialist with salary, benefits, equity, and office space is expensive and slow. A freelance expert who parachutes in, solves the problem, and invoices cleanly is increasingly the preferred model for project-based work. The honest summary: if you are early in your career or working in commoditised skills, 2026 is a challenging market. If you are a senior specialist with a track record in a high-demand field, the conditions have rarely been better. The roles on this list belong firmly in the second category. The 15 High-Paying Roles Each role on this list meets three criteria: it commands a meaningful hourly rate (above $40/hr at entry), it has documented demand growth, and it is genuinely accessible to a freelancer without needing to be on-site five days a week. Annual earning estimates are based on 20 billable hours per week, applied consistently across every role in this article. Pressed for time? [Click here to skip to the full rate comparison table.] 1. Blockchain (Web3) Developer Blockchain is no longer a buzzword; it underpins billions of dollars worth of transactions in finance, supply chain, and even gaming. Even though the crypto market has seen its share of volatility, demand for skilled blockchain engineers remains strong because companies still need private ledgers, supply-chain tracking, and secure tokenisation. From writing tamper-proof smart contracts to auditing DeFi protocols for seven-figure exploits, top-tier engineers sit at the crossroads of money and math, and companies happily pay to keep them on speed-dial. Why demand is surging: The global blockchain technology market is projected to grow from $47.96 billion in 2026 to $577.36 billion by 2034, at a compound annual growth rate of 36.5% (Fortune Business Insights, 2025). Enterprises across finance, healthcare, and logistics are actively hiring, and there simply are not enough qualified developers to go around. Typical Rate: $50 – $150/hr Annual Earning Potential: $52,000 – $156,000 2. AI / Machine-Learning Consultant AI is red-hot, and every investor is hunting for the next breakthrough. Enterprises are scrambling to move from “AI pilot” to real ROI, but pre-trained models still need custom data, guardrails, and cost controls. Freelance ML pros step in to fine-tune LLMs, build anomaly-detection pipelines, and translate geek-speak into boardroom slides. When a single algorithm tweak can save or earn millions, these specialists name their price. Why demand is surging: LinkedIn’s 2025 Jobs on the Rise report showed AI Engineer roles growing at 59% year-over-year, the fastest of any role tracked. The median annual salary for full-time AI/ML engineers sits at $145,000 (US Bureau of Labor, 2024), which gives you a sense of what companies are willing to pay for this expertise on a permanent basis, let alone contract. Typical Rate: $120 – $160/hr Annual Earning Potential: $124,800 – $166,400 3. Cloud Architect/Engineer One mis-tagged S3 bucket can leak data, and unoptimized infrastructure wastes over 80% of a company’s container budget on idle resources. Large companies know that poor cloud setup risks both security breaches and massive unexpected bills, so they take cloud architecture very seriously. Architects who tame AWS, Azure, or GCP keep uptime high and costs low, guiding organisations through migrations and DevOps automation. Their invoices cost far less than the cloud horror stories they prevent. If cloud architecture is about building the fortress, the next role on this list is about defending it. The two skills frequently appear on the same enterprise contract. Why demand is surging: (BLS) projects cloud architect roles to grow 13% through 2033, well above the national average of 4%. The average annual salary for a full-time cloud architect sits at $150,000 (Glassdoor), making freelance contracts in this space extremely well-compensated. Typical Rate: $80 – $180/hr Annual Earning Potential: $83,200 – $187,200 4. Cybersecurity Specialist A single breach now averages $4.4M (IBM 2025). High-profile incidents like the Equifax breach and Colonial Pipeline hack have shuttered operations overnight. Ethical hackers and compliance experts harden networks, run red-team drills, and navigate audits. The pitch to clients essentially writes itself: pay me five figures now, or pay ransomware double

8 Free QuickBooks Alternatives for 2026: Maintaining Financial Clarity Without the Subscription

Running a micro-business or a growing freelance operation means constantly balancing costs against value. You know you need professional accounting software—you need reports, tax compliance, and clean books. Yet, paying a monthly subscription for QuickBooks or Xero when your income is still irregular can feel like an unnecessary burden. You’re looking for a free alternative, but the search can be overwhelming. There are dozens of tools out there, and finding one that is truly free and powerful enough for a real micro-business is a challenge. The right tool is a strategic investment; it saves you time and ensures you build the solid financial foundation you need for future growth. Here, we review the top genuinely free alternatives available today. We look at their core features, limitations, and help you find the best starting point for your micro-business. Note: Fynlo is developed and operated by our team. We aim to keep this review entirely fair and balanced, evaluating all platforms purely on their documented features, limitations, and operational suitability. In this Article 8 Platforms at a Glance Functional Limits of Each Free Plan These platforms all offer a permanently free tier, making them excellent starting points for sole traders and service-based freelancers. Software Primary Free Plan Name Ideal Use Case Key Free Limitations Wave Starter Plan North American Micro-Businesses Many automated bookkeeping features, including bank connection functionality, are reserved for the Pro plan; Receipt scanning is available as a paid add-on or included with Pro Zoho Books Free Plan High-Growth Small Teams Revenue limits (typically <$50k USD / £35k UK, depending on region and eligibility rules) QuickFile XS, S, and M UK Low-Volume Transactions Limited to 1,000 accounting entries (nominal ledger postings) per year Pandle Pandle Free Simplified Bookkeeping Automated bank feeds reserved for paid version Fynlo Forever Free Global / Multi-Currency Restricted to 20 monthly invoices Manager.io Desktop Edition Privacy & Offline Power Users No cloud access or mobile application Akaunting Standard (Self-Hosted) Tech-Savvy Owners Advanced modules and bank feeds carry extra costs ZipBooks Starter Tier Digital Service Providers Restricted to a single user and basic reporting Strengths and Constraints of Each Platform 1. Wave Wave has established itself as a leading choice for micro-businesses in the United States and Canada, reporting support for more than 5.9 million small business owners since 2009 (company data, accessed May 2026). It carried approximately a 4.4/5 rating on G2 as of May 2026 and remains popular due to its lack of caps on the number of customers, invoices, or transactions. The “Starter Plan” provides a full double-entry accounting system at no cost. However, it is important to note that as of 2026, Wave has moved several core features to its “Pro” tier. Many automated bookkeeping features, including bank connection functionality, are now reserved for Pro users in most cases. Transaction data may therefore need to be manually uploaded via CSV or Excel files. Receipt scanning is available as a separate paid add-on on the free Starter plan, or included at no extra cost for Pro users. Certain invoice customization options also require a paid subscription. Wave generates revenue primarily through payment processing fees, making it a viable long-term solution for businesses that accept credit card payments through the platform. 2. Zoho Books Zoho Books is part of a much larger ecosystem of business software, giving it a powerful advantage in scalability. It currently held approximately a 4.6/5 rating on G2 and a 4.7/5 rating on SoftwareSuggest as of May 2026. The “Free Plan” is generous but carries strict operational caps: it is limited to a single user plus one accountant, and allows for up to 1,000 invoices per year. Furthermore, the plan is only available to businesses that do not exceed an annual revenue threshold specific to their region, such as approximately $50,000 in the USA or £35,000 in the UK. For businesses under these limits, Zoho offers sophisticated features including a dedicated client portal and multi-lingual invoicing. However, more advanced requirements like multi-currency handling and automated bank reconciliation are reserved for the paid tiers starting at $20 per month. 3. QuickFile QuickFile is a feature-rich solution that is highly regarded for its flexibility, especially within the UK market. It carries a 4.8/5 rating on Trustpilot as of May 2026. The software is permanently free for businesses that maintain fewer than 1,000 accounting entries (nominal ledger postings) in a rolling 12-month period. Unlike many free competitors, QuickFile includes full multi-currency support and MTD-compatible VAT filing within its free tiers (XS, S, and M). If a business exceeds the 1,000-transaction limit, an annual fee of £60 plus VAT applies. It also offers a “Power User” subscription for approximately £54 + VAT per year, which unlocks advanced customization and white-labeling options for those requiring a more professional appearance. 4. Pandle Pandle is designed with a focus on simplicity, currently maintaining approximately a 4.7/5 rating on Trustpilot based on more than 800 reviews as of May 2026. It is particularly popular among UK-based sole traders due to its built-in Making Tax Digital (MTD) VAT compliance. The “Pandle Free” plan provides unlimited invoicing, customers, and core bookkeeping features without a revenue cap. Its primary limitation is the lack of automated bank feeds; free users must manually import bank statements and categorize transactions. While it lacks some of the complex inventory and project management features found in larger platforms, its “Smart Automation” features (available in the £5/month Pro version) are designed to eventually reduce manual entry as the business grows. 5. Fynlo Fynlo is a specialized accounting tool designed for global freelancers and micro-businesses that require robust multi-currency reporting and project-level budget tracking. The “Forever Free” plan allows for up to 20 monthly invoices and includes income and expense tracking, budget variance analysis, and multi-currency reporting. Fynlo also includes automatic Foreign Exchange (FX) gain/loss calculations, which may be particularly useful for businesses working with international clients. The free tier supports access for one user plus one accountant. However, the free tier’s 20-invoice monthly cap may be restrictive for businesses with higher client volume. More advanced features, such as automated payment collection and advanced budgeting, are available in the paid Starter ($9/month) and Professional tiers. 6. Manager.io Manager.io provides a unique value proposition for businesses that prefer

QuickBooks Desktop 2023 Sunset: What Breaks, What Works, and Your Best Next Steps

If your business runs on QuickBooks Desktop 2023, there’s a hard deadline approaching: May 31, 2026. This is the official “Service Discontinuation” deadline. While software updates are a routine part of business life, this sunset is particularly important because it marks a major shift in how Intuit supports its legacy products. For the hundreds of thousands of US small businesses still using Desktop, the next few weeks are a critical window to plan your next move. In Short: The May 31st Essentials What Actually Breaks on June 1st? It is a common misconception that your software will stop opening after the deadline. You can still access your data locally on your machine. However, the “pipes” that connect your records to the outside world will be cut. Intuit refers to this as losing Connected Services. 1. Automated Bank FeedsThe engine of most modern bookkeeping is the automatic download of transactions. After May 31, this connection is severed. You will be left entering every expense by hand or manually importing bank files—a slower, manual process that is more prone to data entry errors. 2. Integrated Payroll & PaymentsIf you handle payroll within the software, it will stop calculating federal and state taxes and won’t process direct deposits. Similarly, integrated payment processing will deactivate. While Intuit provides instructions for customers to pay you through other means, the seamless “click-to-pay” workflow that helps you get paid faster will be broken. 3. Security and Live SupportSafety is the most critical factor. After May 31, Intuit will no longer provide security patches for the 2023 version. Furthermore, their live technical support teams will no longer be authorized to help with file corruptions or 2023-specific issues. Evaluating Your Options: A Decision Framework Since Intuit shifted to a subscription-only model in late 2021, the landscape for Desktop users has changed. Use this framework to decide which path fits your specific needs. If your business… Your best path is likely… The Reality Check Has complex inventory or deep job-costing needs. QuickBooks Desktop Enterprise This is a “rolling update” model, not a new yearly release. It is powerful, but prices rose ~10% in early 2026. Wants continuity for 12–18 months. QuickBooks Desktop 2024 This is the final version for Pro/Premier Plus.Support officially ends September 30, 2027. Wants standard cloud access. QuickBooks Online (QBO) A major shift in UI.Caution: Depending on your plan, the migration tool may only carry over two years of history. Wants simplicity and high automation. A Modern Alternative Best for those who find legacy systems too feature-heavy for their actual needs. The Strategic Path Forward: Moving Beyond Legacy Workflows The “QuickBooks Sunset” is the perfect moment for a bit of operational honesty: Is your current system actually serving you, or are you just used to its quirks? Staying on a discontinued system for the sake of familiarity often costs more in manual labor and security risk than the migration itself. The goal for your next system shouldn’t just be “replacing what I had.” It should be about finding a workflow that removes the “financial fog” and automates the repetitive tasks that drain your mental bandwidth. Whether you move to the cloud or stick with the final Desktop version, make sure your choice rewards your hard work instead of creating more manual “to-do” lists. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

Why “Cheap” Bookkeeping is the Most Expensive Risk Your Business Can Take

TL;DR: A growing trucking company hired a budget bookkeeper to save on overhead. Two years later, the business was insolvent due to nearly $300,000 in unremitted payroll taxes and IFTA fraud. This post-mortem explores the “Price of Cheap” and the specific red flags that preceded a total business collapse. In this Article Why “saving money” on bookkeeping backfires It started with a simple desire to protect the bottom line. As the owner of a growing trucking service, John knew that every cent was spoken for. Between rising diesel prices, insurance premiums, and constant fleet maintenance, the overhead was suffocating. When he found a local bookkeeper who promised to handle the entire operation for a few hundred dollars a month—roughly a fifth of what established firms quoted—it didn’t feel like a risk. It felt like a win. For the first eighteen months, the “win” seemed real. The reports arrived on time, the bank balances looked healthy, and the bookkeeper was always a friendly voice on the phone. John used the “saved” money to buy a new rig and hire two more drivers. He was scaling. He thought he was safe. The early warning signs John missed The first sign of trouble wasn’t a roar; it was a whisper. John received a notice from the state regarding a discrepancy in his International Fuel Tax Agreement (IFTA) filings. When he questioned his bookkeeper, the answer was smooth: “It’s just state bureaucracy, John. They probably lost a page. I’ll send a corrected copy.” A month later, a second notice arrived—this time from the IRS regarding payroll tax underpayments. Again, the bookkeeper had a plausible explanation. He blamed a software “glitch” and promised it was handled. In the fast-paced world of logistics, where trucks run 24/7, John took him at his word. He had a fleet to manage; he didn’t have time to audit the auditor. When the bookkeeper went radio silent The “glitches” turned into a nightmare when the IRS triggered a formal audit. For the first time, John heard a flicker of panic in his bookkeeper’s voice. Then came the silence. Voicemails went unreturned. Emails began to bounce. When John finally drove to the bookkeeper’s small rented office, he found the lights off and the desk cleared. The “affordable” professional had vanished, leaving behind three years of digital records that were nothing more than a house of cards. What we found when we looked at the books When a reputable accounting firm finally stepped in to perform the forensic cleanup, the reality was horrifying. The “professional” reports John had received every month were complete fabrications. The bookkeeper hadn’t been filing the returns at all. Instead, he was making the bare minimum payments to the IRS—just enough to keep the automated “Final Notice” letters from being triggered—while pocketing the remainder of the tax escrow money. By the time the audit was finished, the bill was staggering: The penalties and interest alone were more than a year’s worth of profit. The business—the dream John had spent a decade building—was legally and financially insolvent. He had to sell his fleet and close his doors. How to spot a bad bookkeeper early If you see these signs, investigate immediately: Comparing budget services vs. professional firms To understand how this happens, we have to look at the math. A “cheap” service is often cheap because it lacks the multi-layer oversight and insurance that protects a business owner. Expense Category Budget “Solo” Bookkeeper Established Professional Firm Typical Monthly Fee $250 – $400 $1,200 – $2,500 Staffing Structure One person (no backup) Team of CPAs & Specialized Staff Internal Controls None (they hold the keys) Multi-person review & verification Compliance Liability High (you are responsible) Low (covered by errors/omissions) Total Cost of Ownership Infinite Risk Predictable Overhead Protecting your business John’s story is a cautionary tale, but it’s one that can be avoided. Before you entrust your life’s work to someone, do your due diligence. Check credentials, call references, and never hand over the reins completely. Maintain oversight by reviewing your financial statements monthly and ensuring you have “view-only” access to your tax accounts. The most expensive service you can buy is the one that doesn’t actually do the job. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

Is Your Business Actually Profitable? Revenue vs. Income Explained

The 30-Second Summary Revenue represents the total volume of sales your business generates, while income is the actual profit remaining after all obligations—including operating costs, taxes, and interest—are met. High revenue indicates market demand, but only high income ensures long-term business sustainability. To grow effectively in 2026, founders must prioritize their efficiency ratio over top-line sales figures. In this Article Why Looking at General Expenditure Is Not Enough It is a common mistake to look at expenses as one large bucket. While tracking total expenditure tells you how much you spent, it doesn’t tell you where the business is failing. By breaking income into three distinct layers, you can diagnose the specific health of your business model. If you only look at the bottom line, you might see a loss and assume you need to cut staff. However, a three-layer analysis might reveal that your staff is efficient, but your raw material costs have risen, meaning you actually need to raise your prices, not reduce your headcount. The Three Layers of Financial Diagnosis 1. Gross Income (The Product Filter) Formula: Revenue – Cost of Goods Sold (COGS) This measures how much profit you make on the actual item or service sold before any overhead is considered. 2. Operating Income (The Management Filter) Formula: Gross Income – Operating Expenses (OPEX) This accounts for the costs of staying in business: rent, payroll, software, and marketing. 3. Net Income (The Owner Filter) Formula: Operating Income – Taxes and Interest This is the final residue, the money that actually belongs to the shareholders. In professional reporting, the terms Income, Profit, and Net Income are used interchangeably to mean exactly this: what remains after every single expense is paid. Common Misconceptions About Financial Growth How to Maximize Your Actual Profit To drive profitability in the current economic climate, consider these advanced financial levers that move beyond basic cost-cutting. 1. Prioritize High-Quality Revenue Not all sales are equal. Sophisticated founders track the Contribution Margin by Customer to identify which clients are actually driving profit. You may find that your top 10% of customers produce 80% of your income, while the bottom 20% actually cost you money in support and custom work. Scaling your bottom line often involves parting ways with low-margin clients to focus on high-efficiency revenue. 2. Test Your Pricing Elasticity Many businesses leave significant income on the table by failing to test price increases. Because a price increase has zero associated production costs, it flows directly to your net income. Even a small 5% increase in price can often lead to a 20–30% boost in profit, yet it is the lever founders are most afraid to pull. 3. Optimize Your Working Capital Cycles Profitability is often choked by the gap between paying your suppliers and getting paid by customers. By shortening your Days Sales Outstanding (DSO) – the time it takes to collect payment – you increase your liquid income without needing a single new sale. Even a five-day improvement in collections can significantly stabilize your cash position. 4. Monitor Your Labor Efficiency Ratio Instead of just looking at total payroll, calculate your Labor Efficiency Ratio (LER): your Gross Profit divided by your Total Labor Cost. This tells you exactly how much gross profit every dollar of salary produces. If your LER is dropping while you hire, your management overhead is likely outstripping your production. 5. Audit Subscription Creep and Shadow IT Industry benchmarks suggest that an average 30% reduction in software expenses can be achieved by eliminating underutilized or redundant tools, a phenomenon often called Shadow IT. Perform a zero-based tech audit: review every recurring subscription. You will frequently find you are paying for licenses for tools your team abandoned months ago or for multiple platforms that perform the same function. The Shift from Growth to Efficiency In the earlier stages of a business, it is natural to obsess over revenue. High sales figures feel like validation that your idea works. However, as a business matures, the focus must shift from how much you can sell to how much you can keep. Financial health is not found in the total volume of money passing through your accounts, but in the efficiency of the “filters” you have built. By diagnosing your business through these three layers, you stop guessing where your money is going and start making data-driven decisions. Whether you need to raise your prices, trim your software stack, or restructure your taxes, the path to a sustainable 2026 starts with looking past the top line. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

Stop the 20% Profit Leak: Why 88% of Spreadsheet Budgets Struggle to Scale (+ Free Templates)

When you first start a business, financial oversight is natural. With a team of five, you likely see every receipt and approve every software subscription. But as you grow, that direct visibility begins to fade. You decentralize, giving credit cards to department heads and autonomy to managers. This transition often leads to what procurement professionals call “Maverick Spend”: purchasing that happens outside of agreed-upon budgets or central visibility. It isn’t usually the result of bad intentions; it is simply the result of a growing team moving faster than its financial systems. A 35-person SaaS company discovered they were paying for 214 SaaS licenses, but only 147 were active users. The excess cost them $4,800 per month. No one intended the waste. It accumulated silently. Most founders don’t lose control because they’re reckless. They lose control because their systems were built for 5 people—and they’re now managing 50. In this guide, we explore how to regain control of this “profit leak” and provide a practical blueprint for departmental financial health. In this article What is a Departmental Budgeting? At its core, a departmental budget is a financial roadmap for a specific segment of your business. It is a document, typically a spreadsheet or dashboard, that forecasts revenue and expenses for a set period—usually a month, quarter, or year. Core Elements: The Spreadsheet Risk Multiplier While decentralization causes visibility issues, the tools we use to manage that growth often introduce their own risks. Most scaling companies rely on a master spreadsheet—a file with dozens of tabs and thousands of rows. The danger here is rarely a single massive catastrophe; it is the accumulation of small, invisible mistakes. Imagine a manager accidentally hard-coding a $5,000 monthly expense into a cell rather than using a dynamic formula. At a small scale, you might spot the discrepancy. Yet in a complex file, that static number remains unchanged while your actual costs triple. By the time the error is caught six months later, you have over-allocated $60,000 based on a single “broken cell.” In a landscape where research by Professor Ray Panko shows that 88% of spreadsheets contain significant errors, these minor technical slips are often the hidden reason runways disappear faster than expected. Top Free Budgeting Templates If you aren’t ready for software, a template is a solid starting point. The right choice depends on your team’s bandwidth, your comfort with formulas, and whether you need basic tracking or in-depth departmental ROI analysis. Microsoft Office Templates: SlideTeam Presentation Templates: Liveflow SaaS Templates: Smartsheet Budget Templates: Your 5-Step Implementation Guide If you’re ready to move from a single consolidated budget to departmental accountability, follow this path: Step 1: Assign Departmental Leads Identify your primary departments (e.g., Marketing, Sales, Product, Ops). Assign one leader to each who is responsible for their team’s spending accuracy. Step 2: Conduct a 3-Month Look-Back Gather the last 90 days of transactions and categorize them by department. You will likely find expenses that “belong” to everyone (like Slack seats) and expenses that should be isolated (like specific LinkedIn ad spend). Step 3: Define Your Fixed Monthly Costs Work with leads to determine their fixed monthly costs—salaries and essential software. This is their “Baseline.” Any spend above this must be linked to a specific growth target. Step 4: Establish the Request Protocol Create a process for new expenses. If Marketing wants a new $200/month tool, they must identify which “Baseline” expense they are cutting to make room for it, or prove how it increases their specific ROI. Step 5: Monthly Performance Comparison On the 5th of every month, sit down with your leads for 15 minutes. Compare what they planned to spend vs. what they actually spent. This creates a culture of transparency where numbers aren’t a surprise. The Strategic Blueprint for Advanced Control 1. The Zero-Based Variance AuditMany companies take last year’s figures and add 5%. This often makes wasteful spending permanent. A more robust method is the Zero-Based Audit, where once a year, every department must justify their expenses from $0 up. This is the most effective way to identify “ghost subscriptions” for tools your team no longer uses. 2. Aligning Budgets with Contribution Margins Rather than simply assigning a “pot of money,” consider setting budgets based on Contribution Margin targets. This means every dollar allocated to a department should be tied to an efficiency metric. For instance, you might authorize a budget that fluctuates based on the team’s ability to keep the Customer Acquisition Cost (CAC) within a certain range. 3. Decentralizing Responsibility through LERTrue financial control happens when department heads feel ownership. One way to foster this is by tracking the Labor Efficiency Ratio (LER). By asking managers to monitor how much gross profit their specific team generates for every dollar spent on their payroll, you shift their focus from “spending” to “value creation.” 4. Implementing “Soft-Close” VisibilityWaiting for a formal “Month-End Close” is often too slow. Implementing a Soft-Close dashboard allows you to see “committed spend” (money promised to vendors) alongside “actual spend” (money that has already left the bank). This prevents the surprise of a large, unforecasted vendor bill hitting your books on the 30th. The Path to Strategic Oversight Spreadsheets eventually reach a functional breaking point. When you’re spending more time fixing formulas than analyzing margins, it’s a clear sign you’ve outgrown manual tools. Shifting toward an integrated system lets you stop reacting to data and start using it as a strategic dashboard to steer your growth. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.

LLC vs. S-Corp in 2026: How to Save $10,000 in Self-Employment Tax

If you’ve successfully scaled your business past the six-figure mark, you’ve reached a significant milestone. Yet, as your revenue grows, the business structure that served you as a lean startup may no longer be the most efficient vehicle for your success. In 2026, many high-performing founders are discovering that staying in their “default” setup is a choice that costs them thousands of dollars in unnecessary tax leakage every single year. Most freelancers stay in a basic LLC because it’s easy. While simplicity has its merits in the beginning, relying on it indefinitely often leads to a massive missed opportunity for wealth building. In a six-figure business, that “simplicity” isn’t free—it represents capital that could be better spent on a strategic new hire, upgrading your technology stack, or funding your retirement. In this article Understanding the Self-Employment Tax Threshold To understand how to save money, we first have to look at how the IRS views a standard LLC. In the eyes of the tax man, you and your LLC are a “disregarded entity”—meaning you are essentially the same person. This results in 100% of your net profit being hit with a 15.3% self-employment tax to cover Social Security and Medicare. As you scale, this math becomes painful. By electing S-Corp status, you fundamentally change the relationship between you and your money. You become an employee of your own business, allowing you to pay yourself a “reasonable salary” (which is taxed) while taking the remaining profit as a distribution. These distributions are exempt from that 15.3% tax, which is exactly where the five-figure savings come from. Business Structure Comparison Between LLC vs S-Corp vs C-Corp Selecting a structure is more than just tax optimization; it is about ensuring your legal framework aligns with your long-term strategic vision. While the S-Corp is often the ideal choice for service-based founders, the C-Corp (or “Inc.”) remains the gold standard for those intending to scale globally or raise outside capital. In fact, approximately 95% of venture capital is directed toward C-Corps because they support the unlimited shareholders and complex stock classes that institutional investors demand. Feature Standard LLC S-Corp Election C-Corp (Inc.) Tax Filing Personal 1040 (Schedule C) 1120-S + K-1 Form 1120 (Corporate) Payroll Requirement None Mandatory W-2 salary Mandatory for active owners Self-Employment Tax 15.3% on 100% of profit 15.3% on salary only None (on dividends) Management Style Flexible; Member-managed; no board required Formal; Requires Board of Directors and Officers Strict; Board oversight with mandatory annual minutes Audit Risk Higher; Schedule C filings often draw IRS scrutiny Lower; Formal structure and payroll reduce “red flags” Moderate; Professional compliance is expected Primary Benefit Maximum simplicity Tax savings for $100k+ earners Scalability & VC funding Primary Drawback High tax as revenue scales Compliance & payroll costs Potential double taxation Finding the Salary Sweet Spot for Maximum Savings The biggest “catch” with an S-Corp is that you must pay yourself a “reasonable salary”. If you pay yourself $0 to avoid all taxes, the IRS will audit you; if you pay yourself your entire profit, the S-Corp becomes a useless expense. We generally look at three tiers of profit to find that “sweet spot”: Maximizing the 20% Qualified Business Income Deduction The Qualified Business Income (QBI) deduction allows many business owners to deduct up to 20% of their business income from their taxes. For S-Corp owners, this deduction is calculated on your profit after your salary is paid. While powerful, the 20% Qualified Business Income (QBI) deduction is subject to limits once your total taxable income rises above the annual thresholds (for example, around $203,000 for single filers and $406,000 for married filing jointly, indexed for inflation). Above these levels, the deduction is gradually restricted based on the type of business you operate and how much you pay in W-2 wages or own in qualified business property. For specified service businesses (such as consulting, legal, medical, and similar fields), the deduction phases out completely as income increases. For other businesses, the deduction can still apply but is capped using wage and property formulas. The key planning strategy is to set a salary that meets IRS “reasonable compensation” rules without unnecessarily reducing the pool of business profit that may qualify for the 20% QBI deduction. Protecting Your Assets by Maintaining the Corporate Veil Both LLCs and Corporations offer a layer of protection for your personal assets, shielding them from business debts and lawsuits. However, this protection depends on maintaining a clear separation between personal and business activity. Implementation Checklist & Deadlines Transitioning to an S-Corp requires discipline in your accounting and adherence to strict IRS timelines. 1. The March 15th DeadlineTo be taxed as an S-Corp for the 2026 calendar year, you must file IRS Form 2553 by March 15, 2026. If you miss this date, your election typically won’t take effect until the following tax year, though “Late Election Relief” is sometimes available for businesses with a valid reason for the delay. 2. Formalize Your BookkeepingBecause the S-Corp is a separate tax entity, “co-mingling” funds (using business money for personal groceries) is a significant compliance risk. You must maintain pristine records and clear separation between business and personal accounts. 3. Set Up Monthly PayrollYou cannot simply “take money out” as an S-Corp owner. You must use a payroll provider (like Gusto or Rippling) to withhold taxes from your salary and issue yourself a W-2 at the end of the year. Moving Toward an Optimized Structure The move from a standard LLC to an S-Corp is a sign of business maturity. It shifts your focus from simply maintaining operations to strategically optimizing for wealth. If your business is consistently netting over $100,000, continuing as a basic LLC is no longer a matter of simplicity—it’s a matter of unnecessary expense. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and

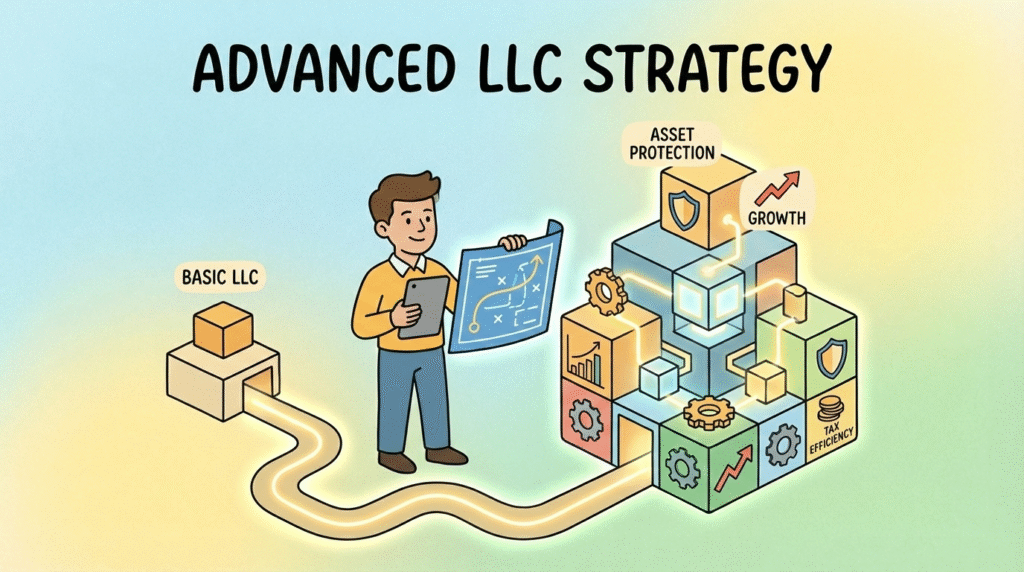

Advanced LLC Strategy: How to Structure for Growth and Asset Protection in 2026

Most founders start with a single LLC because it is the simplest path to getting a tax ID. But as your revenue grows or you begin developing your own products, a single-entity setup may no longer be the most efficient choice. In 2026, the goal is to build a structure that protects your personal assets while remaining flexible enough to scale. Here is how experienced founders structure their businesses to manage risk and optimize for long-term growth. In this article The “Parent & Child” Strategy (Holding Companies) When all your business assets—client contracts, intellectual property (IP), and equipment—live in one LLC, they are all exposed to the same risks. If a client dispute leads to a lawsuit against that LLC, every asset inside it is potentially at risk. The Solution: A Two-Tiered Structure Strategic State Selection: Where to Place Your Entities When choosing where to register your “Parent” or “Child” companies, you can take advantage of specific state rules to manage your tax burden and maximize protection. Wyoming: The Ideal “Parent” Home Wyoming is frequently chosen for the Parent company because it does not require the names of owners to be listed in public records. In 2026, this state-level anonymity provides a layer of data security. Additionally, Wyoming has strong Charging Order laws, meaning if you face a personal lawsuit, it is very difficult for a creditor to seize your business assets. Texas: Scaling the “Child” Company For an Operating Company with a physical presence, Texas offers a significant threshold for small businesses. While Texas has a “Margin Tax,” businesses with total revenue below $2,650,000 in 2026 generally owe $0 in state franchise tax. This allows you to utilize Texas’s vast talent pool and infrastructure without a state-level tax bill until you reach a significant scale. Nevada: High-Level Liability Protection If your business operates in a high-liability field, Nevada is a strong choice for your Operating Company. Nevada law provides an “Exclusive Remedy” protection. This means that a charging order is the only way a creditor can pursue a member’s interest, preventing them from ever seizing business assets or forcing the company to shut down to pay a debt. Tennessee: The “Asset-Light” Advantage Tennessee recently overhauled its tax code, which is highly beneficial for remote agencies and freelancers. In the past, the state taxed businesses based on the value of the physical property they owned (the “property measure”). As of 2026, that rule has been eliminated. Now, the franchise tax is calculated at 0.25% of your apportioned net worth. For example, if your business has a net worth of $200,000 and 50% of your activity is in Tennessee, you are taxed on $100,000 ($250 per year). Additionally, a $50,000 standard deduction now applies to the excise tax, which exempts many small businesses with modest profits from paying that portion of the tax entirely. Planning for an Institutional Exit Even if you do not plan to sell your business immediately, keeping your entity “exit-ready” ensures you don’t lose value during a future sale or funding round. The “Delaware Flip”Most startups begin in Wyoming or their home state to save on costs. Institutional investors, though, almost exclusively require a Delaware entity because of its sophisticated court system. “Flipping” to Delaware involves a legal process called a Statutory Conversion. In this process, you file “Articles of Conversion” in both your current state and Delaware. This legally transforms your existing LLC into a Delaware Corporation while maintaining your business’s history, EIN, and contracts. Doing this 12 months before a planned sale ensures that your legal foundation is already in the format buyers expect, preventing delays in the deal. The Financial Impact of Professional Record-KeepingDuring a sale, buyers perform “due diligence” to verify your business’s health. If your financial records are unorganized or personal and business expenses are blurred, it increases the buyer’s risk. Professionally maintained books signal a mature, low-risk operation, which often results in a higher final valuation for the founder. The Strategic Path Forward Moving beyond a single-entity setup is a clear signal that your business has transitioned from a proof-of-concept to a scaling enterprise. While the administrative weight of managing a “Parent and Child” structure or maintaining multi-state compliance in Wyoming and Delaware can feel significant, it is the most effective way to decouple your hard-earned assets from daily operational risks. Building this legal “firewall” today ensures that when you reach the point of an institutional exit or a major funding round, your foundation is already in the format that sophisticated buyers expect. By prioritizing professional record-keeping and clear entity separation now, you turn your corporate structure into a silent partner that supports your growth instead of a liability that limits it. About the Author Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity. With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.