If you have successfully scaled your organization’s mission, you already know that landing a major grant is only half the battle. The real work begins when that money hits your bank account and the clock starts ticking on compliance. In 2026, donors and grantors are demanding more than just impact stories. They want surgical precision in how every dollar is tracked and spent.

Most growing nonprofits reach a point where a single bank account is no longer enough. If you are still using one general ledger to manage three different restricted grants, you increase the risk of reporting inconsistencies that can attract additional scrutiny from regulators or auditors. Fund accounting provides the structural firewall you need to keep your tax-exempt status safe.

Under U.S. nonprofit accounting standards (FASB ASC 958), organizations must clearly report how funds with donor restrictions are used. Implementing a proper fund accounting system helps ensure that reporting aligns with requirements found in filings such as IRS Form 990 and grantor financial reports.

In this Article

- The Core Difference: Why Standard Bookkeeping Fails Nonprofits

- Categorizing Your Assets: The Three Tiers of Funds

- Compliance Risks: Mistakes That Trigger IRS Reviews

- Step-by-Step: Moving to a Formal Fund Structure

- Optimizing Your Mission’s Financial Future

The Core Difference: Why Standard Bookkeeping Fails Nonprofits

Standard accounting is built to show how much profit a company made. Fund accounting exists to prove accountability. Since your goal is mission delivery rather than the bottom line, your financial system must treat different revenue sources as separate entities.

When a donor gives $10,000 specifically for a youth scholarship, that money cannot pay for office rent. In a standard setup, those dollars get buried in your general cash balance. With fund accounting, that $10,000 stays in its own self-balancing universe. This level of separation is what allows you to look a major foundation in the eye and prove exactly where their money went.

This is why fund accounting is widely used by nonprofits managing multiple grants, donor-restricted gifts, or government funding. It creates a transparent structure that simplifies donor reporting and grant compliance.

Beyond keeping your finances in order, fund accounting empowers your nonprofit to earn donor trust, attract funding, and advance your mission. By keeping finances clear and leveraging data, you can take your nonprofit to new heights.

Categorizing Your Assets: The Three Tiers of Funds

To keep your records clean, you must categorize every dollar based on the specific legal “strings” attached to it. Here is how that looks in practice.

Modern nonprofit reporting standards refer to these as “Net Assets With Donor Restrictions” and “Net Assets Without Donor Restrictions.” However, many nonprofits and grant agreements still use the traditional terms “unrestricted,” “temporarily restricted,” and “permanently restricted.” Understanding both sets of terms helps nonprofit leaders interpret financial reports, grant agreements, and accounting guidance more accurately.

Unrestricted Funds

In modern nonprofit financial statements, unrestricted funds are reported as “Net Assets Without Donor Restrictions.”

These are your most flexible assets, usually coming from general individual donations or fundraising events. You can use these to pay for salaries, utilities, or emergency repairs.

Example: A $50 gift from a monthly donor that you use to pay the office internet bill.

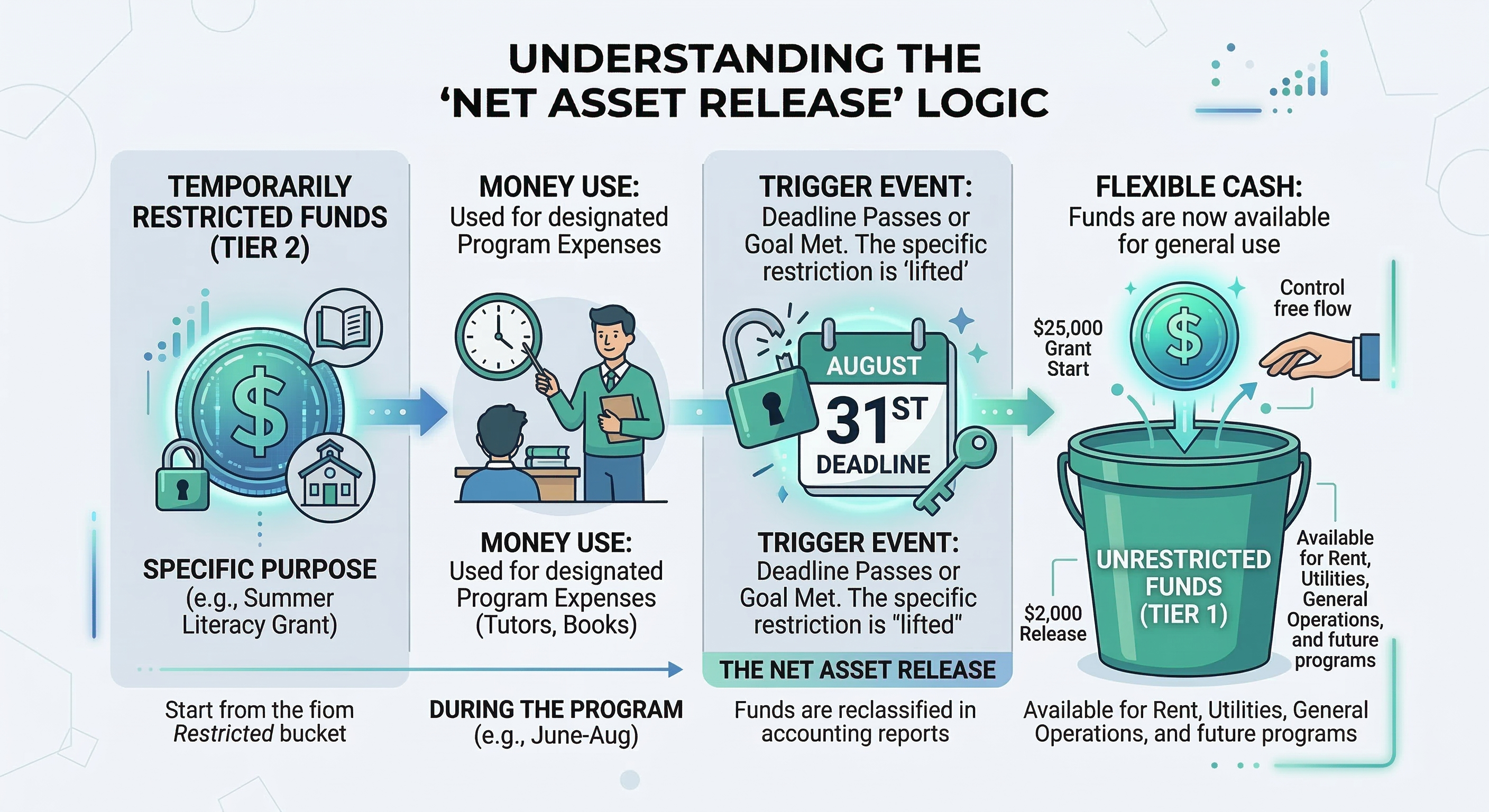

Temporarily Restricted Funds

What were historically called “temporarily restricted funds” are now reported under “Net Assets With Donor Restrictions” when the restriction relates to time or purpose.

These funds are earmarked for a specific timeframe or a specific project. Once the goal is met or the date passes, the restriction is “released” and the money moves into your unrestricted pool for general use.

Example: A $25,000 government grant for a summer literacy program. These funds can only be spent on tutors and books through August; any leftover balance typically becomes flexible cash unless the contract requires its return.

Permanently Restricted Funds

Permanently restricted funds are also reported under “Net Assets With Donor Restrictions,” but they typically involve endowments where the principal must remain intact.

These are typically endowments where the principal amount must remain untouched forever. The nonprofit is usually only permitted to spend the interest or investment income generated by that principal.

Example: A $100,000 endowment established by a founder. You keep the $100,000 in a high-yield account and use the $4,500 in annual interest to fund a yearly community award.

Compliance Risks: Mistakes That Trigger IRS Reviews

The most frequent error we see is inconsistent allocation. If you change how you split overhead costs like rent or insurance halfway through the fiscal year, your reports will look unreliable. Professional fund accounting requires a fixed, defensible method for shared costs.

Another major risk is delayed tracking. Waiting until the end of a quarter to log grant expenses makes errors almost inevitable. By the time you realize a restricted fund was used for a general expense, the damage is already done.

For organizations receiving federal or large foundation grants, accurate allocation and documentation are particularly important because grantors often review financial reports alongside your IRS Form 990 or audited financial statements.

Maintaining daily records is the only way to move your organization into a formal compliance category that carries a lower audit risk.

Step-by-Step: Moving to a Formal Fund Structure

Setting up a formal fund structure is a deliberate process. It involves more than just opening a new bank account. It requires reconfiguring your entire bookkeeping logic to prioritize transparency.

1. Conduct a Revenue Inventory

Start by reviewing every grant agreement and major donation letter from the past year. You need to identify exactly which funds have a purpose restriction, such as building a new community center, versus a time restriction, like funds earmarked specifically for the 2026 fiscal year.

2. Update Your Chart of Accounts with Dimensions

Instead of a flat list of expenses, you must transition to a multi-dimensional system. This means every transaction is tagged with a fund code and a functional code like Program, Management, or Fundraising. This setup allows your software to track a single invoice across multiple grants simultaneously, removing the need for side-spreadsheets that often lead to errors.

3. Define a Consistent Cost Allocation Method

Establish a documented method for allocating shared costs such as rent, utilities, software subscriptions, or insurance across programs and grants. Many nonprofits allocate based on staff hours, square footage, or program budgets.

Consistency is critical because auditors and grantors expect to see the same allocation methodology applied throughout the fiscal year.

4. Implement Grant-Level Expense Tracking

Each grant or restricted fund should have its own tracking code within your accounting system. This allows leadership and finance teams to generate real-time reports showing:

- Remaining grant balances

- Total program spending

- Expenses charged to each restricted fund

This level of visibility significantly reduces errors during grant reporting cycles.

5. Establish a Monthly “Release” Routine

One of the most overlooked steps is the formal release of funds. This is the process of moving money from your Restricted pool to your Unrestricted pool once you have met the donor’s requirements.

Performing this monthly, rather than waiting until the end of the year, ensures your Statement of Activities is always accurate and ready for a last-minute donor inquiry.

Optimizing Your Mission’s Financial Future

The move to formal fund accounting is a sign of organizational maturity. It shifts your focus from simply maintaining daily operations to strategically protecting your revenue.

When your finances are clear, donor trust grows, and more substantial funding follows.

For nonprofits managing multiple grants, restricted donations, or government funding, adopting a structured fund accounting system also simplifies reporting requirements tied to grant compliance, donor transparency, and annual Form 990 filings.

If your nonprofit is ready to move beyond basic spreadsheets and secure its financial foundation, we can help. Fynlo specializes in helping mission-driven leaders transition to optimized accounting structures that simplify compliance.

Schedule a Strategy Call with our team to see how we can streamline your nonprofit’s fund accounting for 2026.