If you’re a brand-new freelancer just stepping into the world of taxes, you’ve probably come across the phrase “Adjusted Gross Income” (AGI) at some point. Don’t worry if it sounds intimidating—AGI is simply a fancy term that helps the IRS figure out how much of your income is actually taxable. Think of it like peeling layers off an onion until you get to the core number that truly matters for your taxes.

So, what is AGI exactly?

Your AGI is basically your total income for the year minus some specific deductions. Start with the money you made from all your work—whether that’s freelance writing gigs, design projects, or coding contracts—plus any other income sources like interest earned from a business savings account. That gives you your gross income.

From there, you subtract certain qualified expenses (we’ll go over some common ones in a second). The number you’re left with after subtracting these allowed deductions is your Adjusted Gross Income.

Why does AGI matter?

Your AGI is a starting point for figuring out how much tax you owe. The IRS uses your AGI to figure out if you qualify for certain tax credits, deductions, or other breaks. In short, it’s the number that tells the IRS, “This is how much I really earned after the most basic deductions.” The lower your AGI, generally speaking, the less tax you’ll pay.

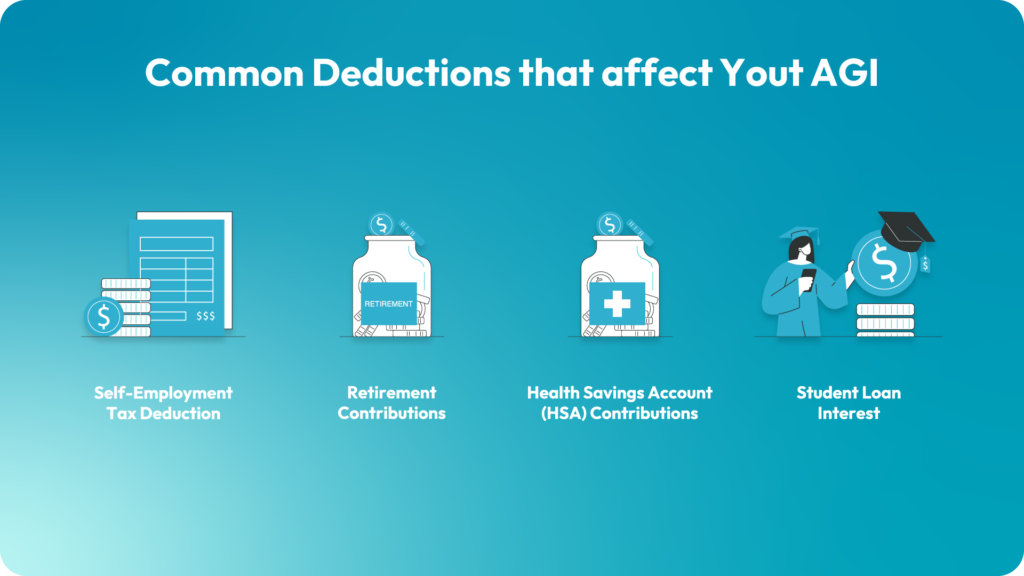

Common deductions that affect Your AGI

As a freelancer, you get to subtract some pretty useful stuff to lower your AGI. Here are a few common ones:

- Self-Employment Tax Deduction: Freelancers have to pay both the employer and employee side of Social Security and Medicare taxes. Luckily, you get to deduct half of this self-employment tax from your gross income.

- Retirement Contributions: If you’re putting money into a traditional IRA or certain other retirement plans, those contributions can often reduce your gross income.

- Health Savings Account (HSA) Contributions: If you have a high-deductible health plan and you contribute to an HSA, you can deduct those contributions directly from your gross income.

- Student Loan Interest: Paid interest on a qualifying student loan? You might be able to reduce your income by up to $2,500 (though there are income limits, so check with the IRS rules).

Keep in mind, there are specific IRS rules for these deductions, and not everyone qualifies. But if you do, they’re a handy way to trim down that number and potentially save some money.

How to Find Your AGI

If you use a tax software or pay a professional, they’ll automatically crunch the numbers for you. But here’s the basic formula:

Gross Income – Above-the-Line Deductions = Adjusted Gross Income (AGI)

- Start with your total gross income: Add up all the money you earned. This includes business income, interest, and any other income the IRS considers taxable.

- Subtract “above-the-line” deductions: These are specific expenses you can subtract from your income to calculate your AGI. They’re called “above-the-line” because they reduce your income before you reach the AGI total. These are the special deductions we just talked about (like half your self-employment tax, certain retirement contributions, and HSA contributions).

- What’s left is your AGI: Simple as that. Your AGI is basically your gross income minus these allowed deductions.

Here’s an example to show you how it all comes together:

| Item | Amount |

| Freelance Income | $60,000 |

| Self-Employment Tax | $9,000 |

| Self-Employment Deduction | -$4,500 (50% from self-employment tax) |

| IRA Contribution | -$3,000 |

| HSA Contribution | -$2,000 |

| Adjusted Gross Income | $50,500 |

Wrapping it up

For many new freelancers, taxes feel like a giant, tangled mess of complicated terms. But understanding key concepts like AGI can make the whole process feel a lot less scary. Keep in mind that your AGI serves as a building block for figuring out your overall tax situation. The more you understand it, the more control you’ll have over how much you pay—or don’t pay—at tax time.

As you get comfortable with these basics, you’ll find that tax season isn’t as overwhelming as it first appears. And remember, if you’re ever unsure, talking to a tax professional or using trusted tax software can give you the peace of mind you need.