If you’ve successfully scaled your business past the six-figure mark, you’ve reached a significant milestone. Yet, as your revenue grows, the business structure that served you as a startup may no longer be the most efficient vehicle for your success. In 2026, many high-performing founders are finding that the “default” setup is quietly absorbing capital that could otherwise be used to fuel their next phase of growth.

Most freelancers stay in a basic LLC because it’s easy. While simplicity has its merits, relying on it indefinitely often leads to a significant missed opportunity. In a six-figure business, that “simplicity” can represent thousands of dollars in overpaid taxes—capital that could be better spent on strategic hires, advanced technology, or long-term wealth building.

In this article

- Understanding the Tax Threshold

- Comparison: LLC vs. S-Corp

- The 2026 Salary Strategy: Finding the “Sweet Spot”

- Two Advanced Concepts Every Founder Should Know

- Implementation Checklist & Deadlines

- Next Steps: Moving Toward an Optimized Structure

Understanding the Tax Threshold

In a standard LLC, the IRS treats you and your business as one entity for tax purposes. This means 100% of your net profit is subject to a 15.3% self-employment tax (covering Social Security and Medicare).

- At $50,000 profit: You pay ~$7,650 in self-employment tax.

- At $150,000 profit: That bill climbs to over $21,000.

By electing S-Corp status, you change the math. You become an employee of your business, paying yourself a “reasonable salary” (subject to the 15.3% tax), while taking the rest of your profit as a distribution. Distributions are not subject to self-employment tax, allowing you to shield a large portion of your income from that 15.3% hit.

Comparison: LLC vs. S-Corp

To help you decide which structure aligns with your current goals, here is a breakdown of the practical differences in 2026.

| Feature | Standard LLC (Disregarded Entity) | S-Corp Election |

| Tax Filing | Filed on your personal 1040 (Sch C) | Separate 1120-S business return + K-1 |

| Payroll Requirement | None (Personal draws) | Mandatory W-2 payroll for the owner |

| Self-Employment Tax | Paid on 100% of profit | Paid only on W-2 salary |

| Admin Complexity | Low | Moderate (requires payroll & bookkeeping) |

| Primary Benefit | Maximum simplicity & flexibility | Maximum tax savings for $100k+ earners |

| Primary Drawback | High tax burden as revenue scales | Higher annual filing & compliance costs |

The 2026 Salary Strategy: Finding the “Sweet Spot”

The key to a successful S-Corp is setting a “reasonable salary.” If your salary is too low, you risk an audit; if it’s too high, you lose the tax benefit.

Tiered Salary Guidelines

- Profit under $60,000: Generally, we recommend staying as a standard LLC. The administrative costs of payroll and extra tax filings often outweigh the tax savings at this level.

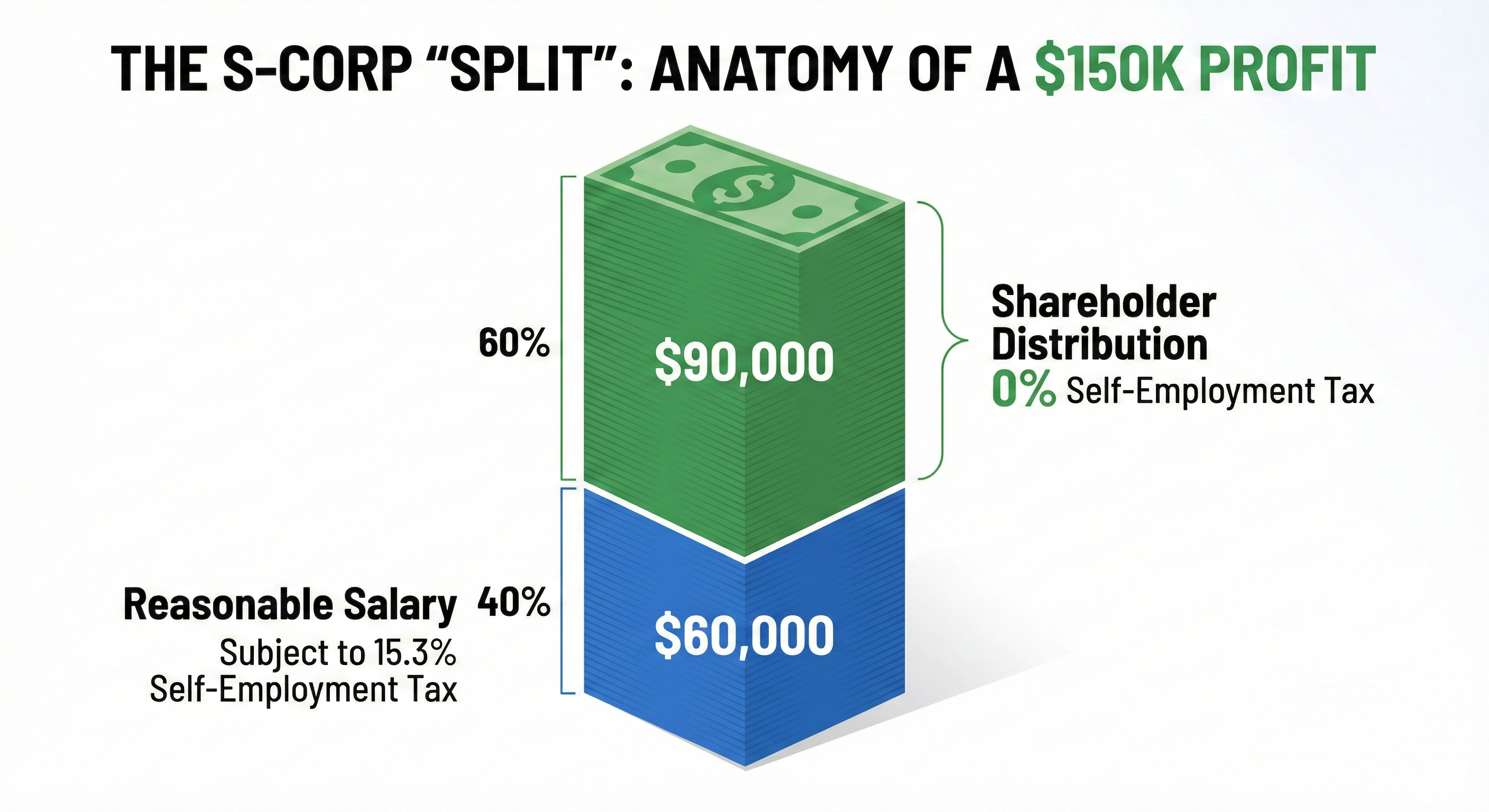

- Profit $80,000 – $150,000: This is the ideal range for the 40/60 or 50/50 rule. For example, at $150,000 profit, paying yourself a $60,000 salary is typically defensible for most professional services. This structure allows you to take the remaining $90,000 as a distribution, saving you approximately $10,000 to $12,000 in taxes compared to a standard LLC.

- Profit $250,000+: At this level, we must account for the Social Security Wage Base cap. In 2026, only the first $176,100 (estimated) of your salary is hit with the 12.4% Social Security tax. Once you pass this, your salary only incurs the 2.9% Medicare tax.

Two Advanced Concepts Every Founder Should Know

When moving to an S-Corp, it’s important to understand two specific mechanisms that affect your final bottom line: the QBI deduction and the change in audit profiles.

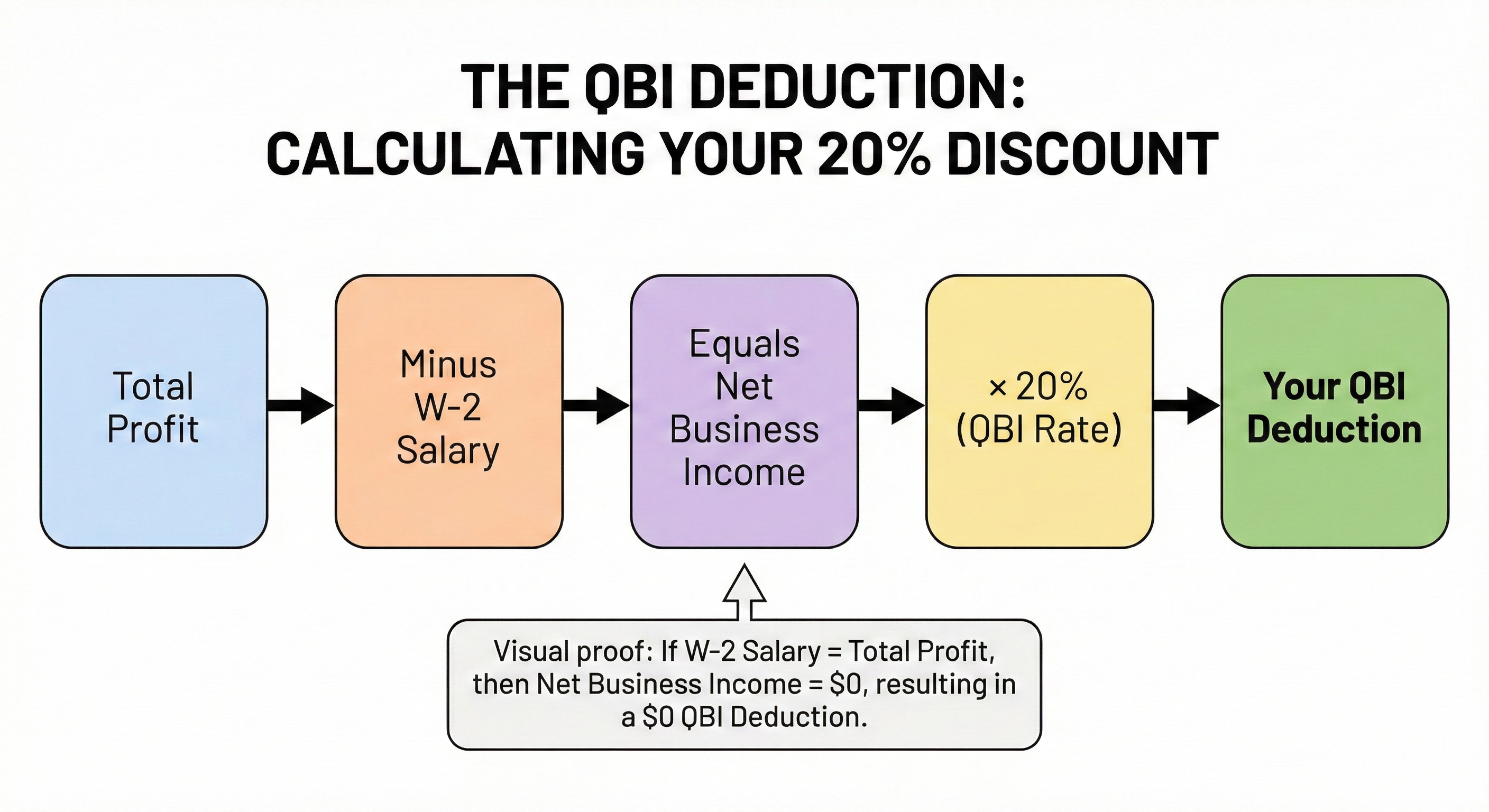

1. The QBI Deduction: The “20% Discount” Rule

The Qualified Business Income (QBI) deduction allows many business owners to deduct up to 20% of their business income from their taxes. For S-Corp owners, this deduction is calculated on your profit after your salary is paid.

While powerful, the 20% Qualified Business Income (QBI) deduction is subject to limits once your total taxable income rises above the annual thresholds (for example, around $203,000 for single filers and $406,000 for married filing jointly, indexed for inflation). Above these levels, the deduction is gradually restricted based on the type of business you operate and how much you pay in W-2 wages or own in qualified business property.

For specified service businesses (such as consulting, legal, medical, and similar fields), the deduction phases out completely as income increases. For other businesses, the deduction can still apply but is capped using wage and property formulas. The key planning strategy is to set a salary that meets IRS “reasonable compensation” rules without unnecessarily reducing the pool of business profit that may qualify for the 20% QBI deduction.

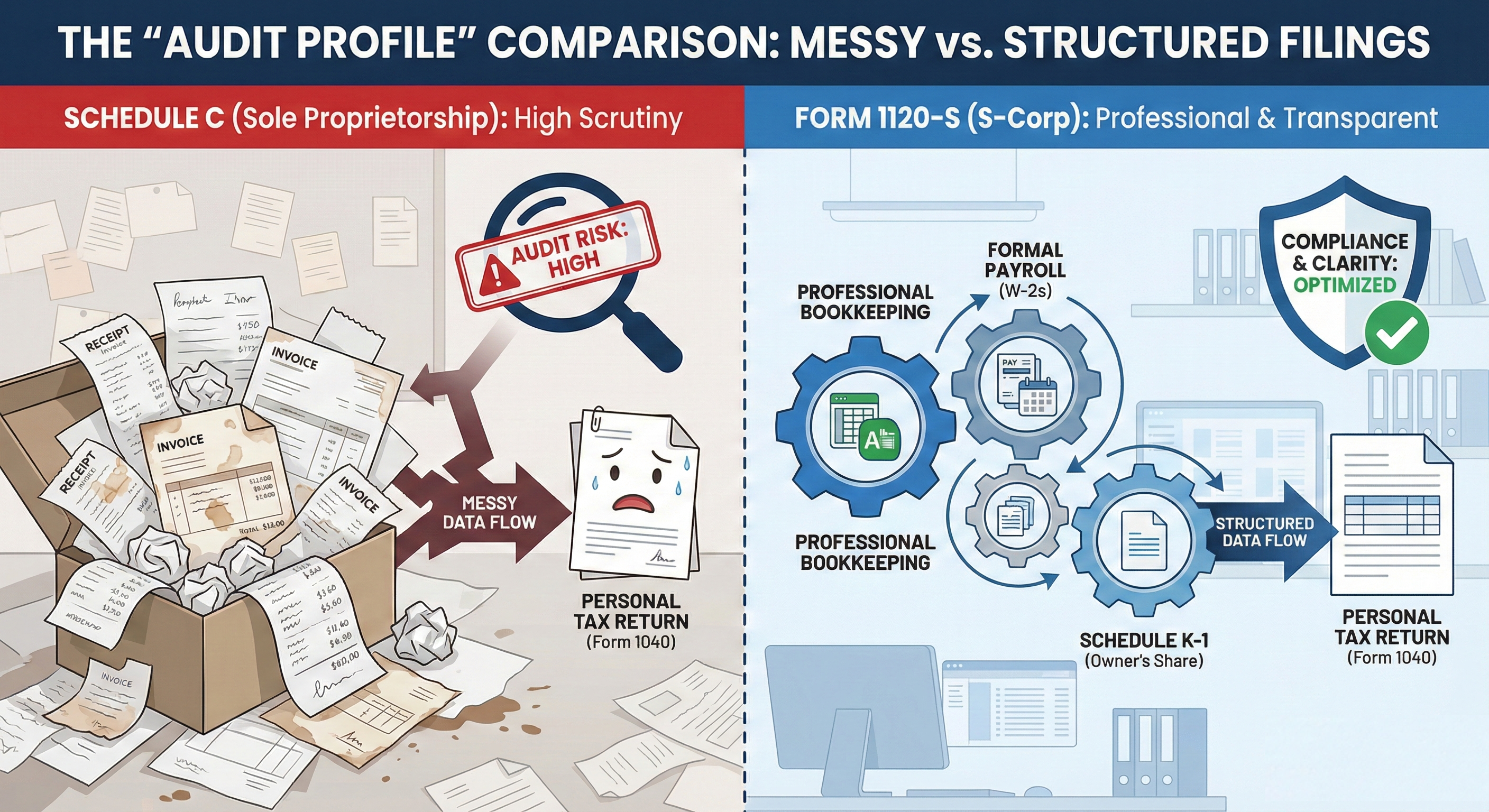

2. 1120-S vs. Schedule C: The “Audit Profile” Shift

Standard LLCs usually report income on Schedule C as part of the owner’s personal tax return. These filings often blur the line between personal and business activity, which can draw extra attention when deductions look inconsistent or unsupported.

- The S-Corp Advantage: An S-Corp files its own business tax return (Form 1120-S). The profit or loss is then passed to you through a K-1 and reported on your personal return.

- Why it matters: An S-Corp must run payroll, issue W-2s, and maintain clean financial statements. This level of structure tends to reduce red flags that are common with loosely tracked Schedule C filings. Choosing an S-Corp isn’t just about tax savings — it also moves your business into a more formal compliance category that often carries a lower audit risk.

Implementation Checklist & Deadlines

Transitioning to an S-Corp requires discipline in your accounting and adherence to strict IRS timelines.

1. The March 15th Deadline

To be taxed as an S-Corp for the 2026 calendar year, you must file IRS Form 2553 by March 15, 2026. If you miss this date, your election typically won’t take effect until the following tax year, though “Late Election Relief” is sometimes available for businesses with a valid reason for the delay.

2. Formalize Your Bookkeeping

Because the S-Corp is a separate tax entity, “co-mingling” funds (using business money for personal groceries) is a significant compliance risk. You must maintain pristine records and clear separation between business and personal accounts.

3. Set Up Monthly Payroll

You cannot simply “take money out” as an S-Corp owner. You must use a payroll provider (like Gusto or Rippling) to withhold taxes from your salary and issue yourself a W-2 at the end of the year.

Next Steps: Moving Toward an Optimized Structure

The move from a standard LLC to an S-Corp is a sign of business maturity. It shifts your focus from simply maintaining operations to strategically optimizing for wealth. If your business is consistently netting over $100,000, continuing as a basic LLC is no longer a matter of simplicity—it’s a matter of unnecessary expense.

Ready to Optimize Your 2026 Tax Strategy?

Don’t let March 15th slip by without a plan. Fynlo helps six-figure founders transition to optimized structures that protect their revenue and simplify their compliance.

Schedule a Strategy Audit to see if an S-Corp election is the right move for your 2026 revenue goals.