Most of us who go out on our own do it for the work itself. Whether you’re a designer, a writer, or a consultant, you’re driven by the craft. But then you start your business, and you realize you’ve also become its reluctant Chief Financial Officer.

I remember my first year, staring at my accounting software and feeling completely out of my depth. I was great at my actual job, but when it came to the money side, I was just guessing. I’d look at my bank account, see money in there, and figure I was doing okay. But I always had this low-level hum of uncertainty. Am I really making a profit? Am I charging enough? Where is all the money going?

It turns out the answers to those questions are sitting in three financial reports. They sound intimidating, but they’re really just tools to help you trade that uncertainty for clarity.

Table of Contents

- The Income Statement: Answering, “Did I Actually Make a Profit?”

- The Balance Sheet: A Snapshot of Your Business’s Financial Health

- The Cash Flow Statement: Tracking Where Your Money Really Goes

- From Numbers to Know-How

The Income Statement: Answering, “Did I Actually Make a Profit?”

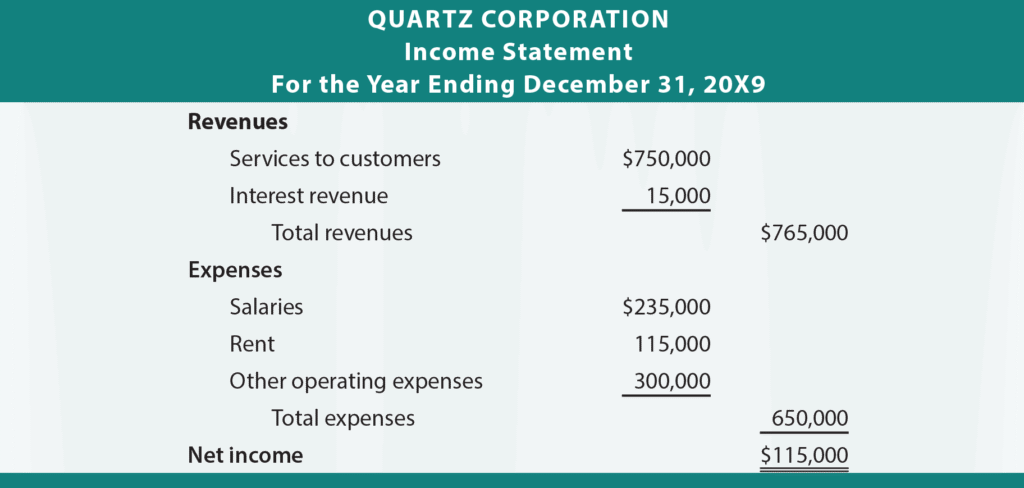

Example of Income Statement (Source: principlesofaccounting.com)

This is the most basic question, and the Income Statement (often called the P&L for Profit & Loss) answers it directly. It’s a simple summary of your revenue versus your expenses over a specific period, like a month or a quarter.

- Revenues: Everything clients paid you.

- Expenses: Everything you spent to run your business.

- Net Income (Bottom Line): What’s left over.

In my early days, I felt like I was working constantly but my savings weren’t growing. I finally sat down and looked at my P&L. The “aha!” moment wasn’t some huge, dramatic discovery. It was seeing I was spending nearly $150 a month on various software subscriptions I’d signed up for and forgotten about. It’s the small leaks that often sink the ship. The P&L helps you spot them. It shows you the real cost of doing business, beyond just the big, obvious expenses.

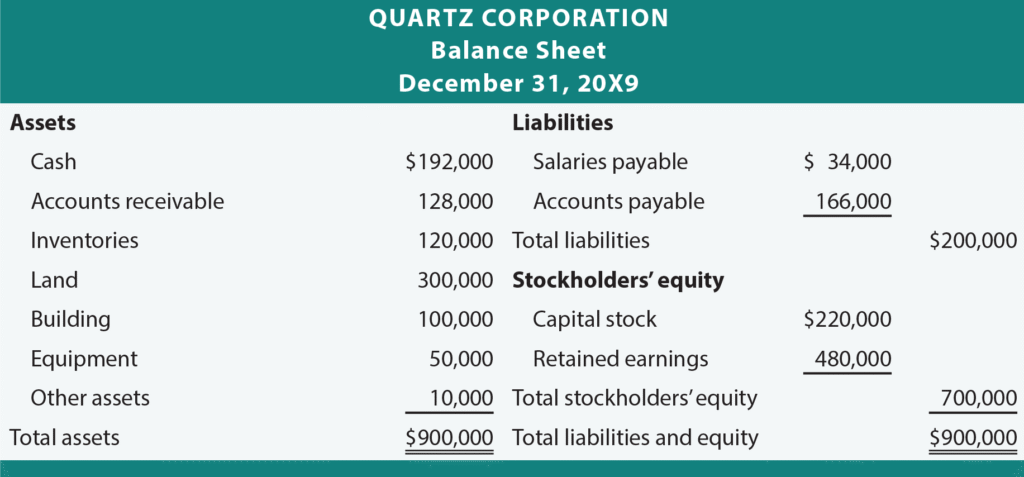

The Balance Sheet: A Snapshot of Your Business’s Financial Health

Example of Balance Sheet (Source: principlesofaccounting.com)

Being profitable month-to-month is great, but you also want to know if you’re building a stable business over the long term. That’s where the Balance Sheet comes in.

If the P&L is a movie of your recent performance, the Balance Sheet is a snapshot of your business’s financial health right now. It’s based on a simple formula:

Assets (What you have) = Liabilities (What you owe) + Equity (What’s yours)

- Assets are things like the cash in your bank, the computer you use for work, and—importantly—the invoices you’ve sent that haven’t been paid yet (Accounts Receivable).

- Liabilities are your debts, like your business credit card balance or a loan you took out for equipment.

- Equity is the value left over for you, the owner.

Honestly, for a long time, I ignored my Balance Sheet. It felt too “corporate.” But it’s surprisingly practical. And critical, too: according to Intuit QuickBooks, 57% of small business owners have experienced problems with their cash flow. Business owners lose $34,000 on average by being forced to turn down work, specifically due to issues created by insufficient cash flow. That “Accounts Receivable” line shows you exactly how much money you’re waiting on from clients. Seeing that number get too big can be the nudge you need to get better about your payment terms and follow-ups.

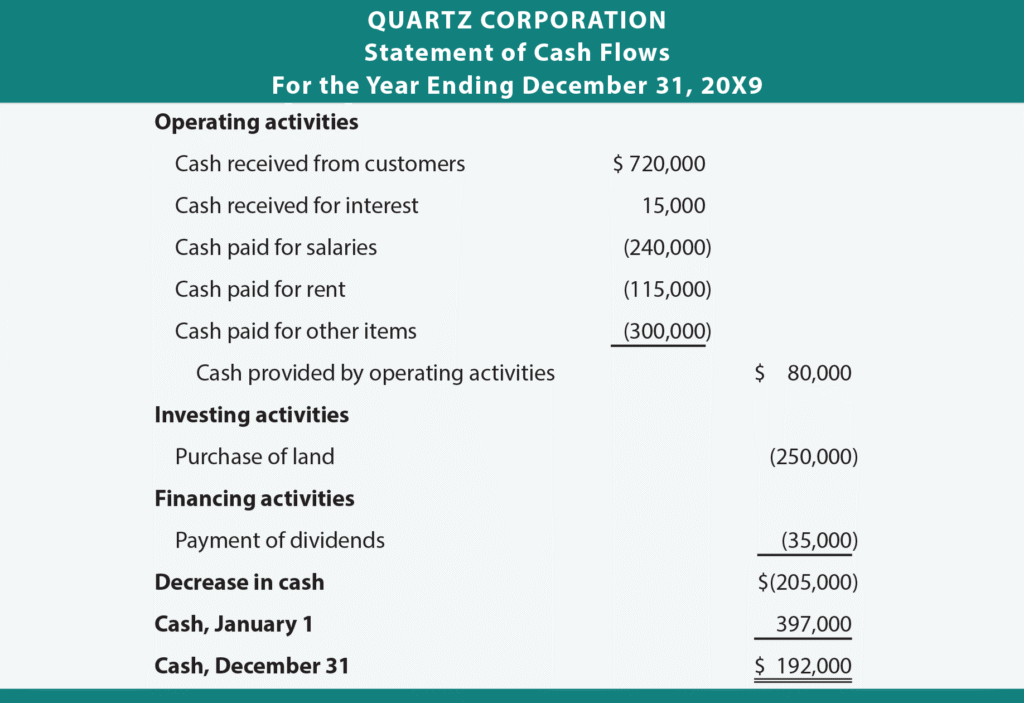

The Cash Flow Statement: Tracking Where Your Money Really Goes

Example of Cash Flow (Source: principlesofaccounting.com)

This is the big one. Have you ever had a profitable month on paper but felt completely broke? I’ve been there. You’ve done the work, you’ve sent the invoices, but your bank account is dangerously low and bills are due.

This is a cash flow problem, and the Cash Flow Statement is the tool that explains it. It tracks the actual cash moving in and out of your business. According to SCORE, 82% of small businesses that fail do so because of poor cash flow. It’s not that they aren’t profitable, it’s that they run out of cash.

A friend of mine who runs a small trade business almost learned this the hard way. His P&L looked fantastic because he was landing big jobs. But he was paying his suppliers in 30 days, while his clients were taking 60 or even 90 days to pay him. His business was profitable, but it was being starved of cash. The Cash Flow Statement made this timing gap impossible to ignore. It forced him to start collecting deposits upfront and tighten his payment deadlines. It didn’t just lower his stress; it saved his business.

From Numbers to Know-How

Look, nobody gets into freelancing because they have a passion for spreadsheets. But you owe it to yourself and your business to understand the basics. You don’t need to become an accountant, you just need to get curious.

Start small. Ask your bookkeeper or use your accounting software to run your P&L once a month. Take 20 minutes to look at it. Where did your money come from? Where did it go?

Doing this consistently replaces that vague financial anxiety with quiet confidence. You start making decisions based on real data, not just a gut feeling. And in this line of work, having fewer unpleasant surprises is one of the best assets you can have.

Ready to trade that financial uncertainty for clarity? At Fynlo, we handle the accounting and bookkeeping so you can focus on what you do best. Let us help you understand the story your numbers are telling. Schedule a free call with us today.

You may also like these articles: