Stop Overpaying the IRS: Your 2025 Guide to Freelance Tax Write-Offs

Freelancing is more than just a job; it’s a business. And one of the biggest perks of being your own boss is the ability to lower your tax bill by legally deducting business expenses. Every missed deduction is lost cash — and most freelancers are giving money away without realizing it. IRS data shows that nearly 70% of self-employed filers underclaim business expenses. Misplaced receipts, fear of audits, and assuming “it’s not worth it” are some of the most common reasons. I’ll admit, in my early days I made the same mistakes and missed out on valuable write-offs simply because I didn’t know what to look for or how to track them. It’s like leaving free money on the table, and who wants to do that? This isn’t just a list of deductions. Think of it as your personal guide to navigating the ins and outs of freelance finances for the 2025 tax year. We’ll cover everything from the home office to health insurance, helping you keep more of your hard-earned money and avoid a last-minute scramble. Ultimately, a stress-free tax season starts with good record-keeping, and the journey to a lower tax bill begins today. Table of Contents What’s the Big Deal with Tax Deductions? Think of a tax deduction as a way to reduce your taxable income. The more you can legally deduct, the lower your taxable income becomes, which means you pay less in income tax. For example, if you earn $60,000 in freelance income and have $10,000 in eligible business expenses, you’ll only be taxed on $50,000. That’s a huge difference! However, it’s not just about what you deduct—it’s about doing it correctly. The IRS is known for its strict rules, and getting it wrong can lead to penalties. The IRS requires you to file a tax return if you have net earnings from self-employment of $400 or more. It’s crucial to file on time and accurately report all income and expenses. The Most Common Tax Write-Offs for Freelancers Here are some of the most popular tax deductions that freelancers and gig workers can claim. It’s vital to remember the golden rule of tax deductions: an expense must be “ordinary and necessary” for your business. 1. Home Office Deduction This is one of the most significant tax benefits for freelancers who work from home. You can deduct a portion of your home-related expenses if you use a part of your home “exclusively and regularly” as your principal place of business. This includes: There are two ways to calculate this deduction: 2. Vehicle Expenses If you use your car for business — whether that’s meeting clients, attending conferences, or hauling equipment — those costs are deductible. It’s worth noting that you can’t deduct your normal commute from home to a regular office, but if you travel between temporary worksites or make trips that are directly tied to your business, those miles count. 3. Health Insurance Premiums Health insurance can be one of the biggest expenses for freelancers, but the good news is that you can deduct the full cost if you’re self-employed and not covered by a plan through your employer or your spouse’s job. That means 100% of what you pay in premiums for medical, dental, and even long-term care insurance can be written off. This deduction is especially valuable because it directly lowers the income you’re taxed on, not just as part of itemized deductions. In other words, every dollar you spend on health insurance premiums reduces the income the IRS uses to calculate your taxes — which can make a real difference at tax time. 4. Business Supplies and Equipment The tools of your trade are fully deductible. This includes: 5. Advertising and Marketing Every successful freelance business needs clients, and getting your name out there comes with costs. The good news is that advertising and marketing expenses are 100% deductible. This can cover a wide range of things you might already be using to grow your business: 6. Education and Training Investing in yourself is a smart business move, and the IRS agrees. If the education or training you pay for helps you maintain or improve the skills you already use in your current business, those costs are deductible. This can include: Keep in mind that you can only deduct training that builds on the work you already do. If the education prepares you for a completely new career, it doesn’t qualify. For instance, a freelance writer could deduct a course on copywriting, but not the cost of a degree in accounting. rates and access discounted prices. Take advantage of flat-rate boxes, which can be cheaper for heavier, smaller items. What You Can’t Deduct Knowing what doesn’t qualify is just as important as knowing what does. Mixing in personal expenses is one of the most common mistakes new freelancers make, and it can be a red flag for the IRS. Here are some things that may feel work-related but don’t actually count: Simple Money Habits That Save You Stress When I first started out, I used to dread tax season. Every March I’d find myself scrolling through old bank statements, trying to remember if that random coffee shop charge in July was a client meeting or just me needing caffeine. If that sounds familiar, you’re not alone. So many freelancers end up scrambling and, as a result, miss out on deductions and peace of mind. The truth is, managing your finances doesn’t have to be a source of anxiety. With a few simple habits built into your routine, you can save yourself hours of stress and keep more of what you earn. Here are some of the most valuable lessons I’ve learned along the way: Don’t Let Tax Season Overwhelm You Taxes for freelancers don’t have to be a source of stress. By understanding what you can deduct and diligently tracking your expenses throughout the year, you’ll not only save money but also feel in control of your business’s financial health. This

The Freelancer’s Guide to the 2025 Self-Employed Quarterly Tax Schedule

One of the best parts of being self-employed is the freedom it brings. You’re the boss, setting your own hours and charting your own course. But with that freedom comes a responsibility that new freelancers and business owners often discover the hard way: you’re also the payroll department. Unlike a traditional job where taxes are automatically withheld from each paycheck, when you work for yourself, you’re responsible for paying your own taxes directly to the IRS. This isn’t done in one lump sum at the end of the year. Instead, the U.S. operates on a “pay-as-you-go” system, which for the self-employed, means paying estimated taxes four times a year. Although it may seem daunting, staying on top of your quarterly payments is manageable. Missing a deadline can lead to underpayment penalties that often catch self-employed individuals off guard. By familiarizing yourself with the due dates and the required steps, you can avoid surprises and keep your cash flow on track. Table of Contents TL;DR Summary What Are Estimated Taxes? Think of these as the self-employed version of the tax withholding (W-4) you had at a traditional job. They are periodic payments you make throughout the year to cover your tax liability. These payments cover two main things: By paying quarterly, you avoid a massive tax bill in April and stay compliant with IRS requirements. Who Needs to Pay Estimated Taxes? The rule of thumb from the IRS is straightforward. You generally must pay estimated taxes if you expect to owe at least $1,000 in tax for the year 2025 after subtracting any withholding or credits. This applies to most freelancers, independent contractors, and small business owners who operate as: If you also earn W-2 wages, you may be able to avoid estimated tax payments by simply having your employer withhold more tax from your regular paycheck. The 2025 Quarterly Tax Deadline Schedule The quarterly deadlines are not evenly spaced every three months, which is a common point of confusion. It’s essential to mark these dates on your calendar. The next deadline is Sept. 15, 2025, for income earned from June 1 to Aug. 31. Here are the deadlines for paying your 2025 estimated taxes: Quarter For Income Earned Between: Deadline Q1 Jan 1–Mar 31, 2025 April 15, 2025 Q2 Apr 1–May 31, 2025 June 16, 2025 (Note: June 15 is a Sunday) Q3 Jun 1–Aug 31, 2025 Sept 15, 2025 Q4 Sep 1–Dec 31, 2025 Jan 15, 2026 Note: Deadlines that fall on a weekend or holiday are moved to the next business day. How to Calculate Your Estimated Tax Payment Calculating your payment requires a bit of forecasting, but it can be broken down into simple steps. Step 1: Estimate Your Total Net Income for the YearStart with your projected gross income (everything you expect to earn). Then, subtract your estimated business expenses (software, supplies, home office costs, etc.). This gives you your net self-employment income. This is why diligent, year-round tracking of income and expenses is so critical. Step 2: Calculate Your Self-Employment (SE) Tax For 2025, the SE tax rate is 15.3% on the first $176,100 of net earnings. This breaks down into 12.4% for Social Security and 2.9% for Medicare. If you earn more than that, you continue to pay only the 2.9% Medicare tax on the excess, plus a 0.9% Additional Medicare Tax if your earnings exceed $200,000 (single) or $250,000 (married filing jointly). Step 3: Calculate Your Estimated Income Tax Take your net income, subtract the deduction for one-half of your SE tax, and then apply the appropriate federal income tax bracket based on your filing status (single, married filing jointly, etc.). Step 4: Add It Up and Divide by Four Add your estimated income tax and your self-employment tax together to get your total estimated tax for the year. Divide this number by four to get your quarterly payment amount. Pro-Tip: The “Safe Harbor” Rule Worried your estimate will be off? The IRS offers a “safe harbor” rule to help you avoid underpayment penalties. You are generally protected from penalties if you pay, through withholding and estimated payments, at least: Many freelancers use the 100% rule for simplicity if their income is stable, as it’s based on a known number from last year’s tax return. Worked Example Here’s how to calculate quarterly taxes for a freelancer expecting $100,000 in net earnings (after expenses) in 2025: Note: Your actual tax rate depends on your filing status; check IRS brackets or consult a professional. How to Pay Your Estimated Taxes The IRS makes it easy to pay online. Here are the most common methods: What If My Income Is Uneven? What if you have a huge project in the spring and a slow winter? If your income fluctuates significantly, you can use the annualized income installment method. This allows you to adjust your payments based on the income you earned in each specific period, rather than paying four equal installments. It’s more complex and may require Form 2210 and professional assistance, but modern accounting tools like Fynlo can help you track income by period to make this calculation easier. Don’t Fear the Deadlines. Systemize Them Quarterly estimated taxes are a fundamental part of self-employment, but they don’t have to be a source of anxiety. The key is to move from reactive, last-minute calculations to a proactive, organized system. When you have a clear, real-time picture of your income and expenses throughout the year, calculating your payments becomes a simple check-in, not a frantic scramble. Ready to swap tax-season anxiety for year-round financial clarity? Modern accounting tools like Fynlo can reduce tax prep time by up to 40–60%, according to industry benchmarks. Sign up for a free Fynlo account today or schedule a call with our team to discover how our intuitive platform can transform your business.

20 Common Accounting Terms for Freelancers

Running a business, big or small, means dealing with numbers. But for many of us with not much accounting background, those accounting terms can feel like a foreign language. Here’s the thing, Go Remotely’s Accounting Statistics say that 60% of small business owners don’t feel knowledgeable about finances and accounting. Don’t worry, you’re not alone. This guide breaks down 20 essential accounting terms every freelancer or small business owners needs to know. Let’s make sense of the numbers together. Your Financial Glossary Let’s dive into each term, starting with: 1. Revenue/Income Revenue is simply the total money your business brings in from sales or services. Think of it as your gross income, before you subtract any expenses. 2. Expenses Expenses are what you spend to keep your business running and generate revenue. Here are the main types: 3. Profit/Net Income Profit is essentially the financial gain your business achieves when your revenue, the money you bring in, surpasses your expenses, the money you spend. To put it simply, it’s what you get to keep. So, for example, if your business generated $10,000 in revenue and you incurred $6,000 in expenses, you’d end up with a profit of $4,000. 4. Loss A loss is the opposite: when your expenses are higher than your revenue. If you spent $8,000 and only made $5,000, you’ve got a $3,000 loss. This trend is not sustainable in the long term. 5. Assets Assets are anything your business owns that has value, from cash and equipment to your laptop or even your website and intellectual property. 6. Liabilities Liabilities are what your business owes to others, like loans, supplier payments, and credit card balances. 7. Equity Equity is essentially your net worth in the business. It’s what would be left if you sold all your assets and paid off all your debts. 8. Cash Flow Cash flow is the movement of money in and out of your business over a period of time. It’s about having enough cash on hand to pay the bills. Even profitable businesses can struggle with poor cash flow. (Check out our blog on Cash Flow Projection!) 9. Accounts Payable (AP) Accounts Payable (AP) represents the money your business owes to suppliers or other creditors for goods or services received but not yet paid. For instance, if you’ve received inventory or supplies on credit and haven’t paid the invoice yet, that amount is considered Accounts Payable. 10. Accounts Receivable (AR) Accounts Receivable (AR), on the other hand, is the money your customers owe your business for goods or services you’ve already delivered or provided. It’s the opposite of Accounts Payable; it’s money coming in. For example, if you’ve sent an invoice for $500 for services rendered and the customer hasn’t paid yet, that $500 is an Accounts Receivable. It’s important to track AR carefully, as it directly impacts your cash flow and ability to cover your own expenses. 11. Inventory Inventory refers to the goods your business holds for sale. It’s the items you have on hand, ready to meet customer demand. In essence, effective inventory management is crucial. You don’t want to run out of stock and lose sales, but you also don’t want too much stock sitting around, which leads to waste and ties up your capital. 12. Depreciation Depreciation is the gradual loss of value of your assets over time, like a restaurant oven getting older. It’s recorded as an expense on your income statement. 13. Cost of Goods Sold (COGS) COGS is the direct cost of producing your goods, including materials and labor. For a restaurant, it’s the cost of ingredients and food preparation. For an online shop selling handmade crafts, it’s the cost of raw materials like fabric and yarn, plus the labor involved in creating the finished products. 14. Balance Sheet A balance sheet is a financial picture of your business at a specific moment, showing what your business owns (your assets), who your business owes money to (your liabilities), and how much you, the owner, have invested (your equity). It’s based on the equation: Assets = Liabilities + Equity. (Learn more about balance sheets here.) 15. Income Statement An income statement shows your business’s revenue, expenses, and profit or loss over a specific period (e.g., a month or a year). It tells you how well your business performed during that time. So, how does it differ from a balance sheet? Well, a balance sheet provides a snapshot of your business’s financial position at a specific moment, while the income statement focuses on your performance over time. They work together to give you a full picture of your financial health. 16. General Ledger The general ledger is the comprehensive record that organizes all your business’s financial transactions. Imagine it as a detailed logbook of every financial event, categorized by type, such as sales, expenses, and asset changes. This organization makes it easy to see the complete picture of your business’s financial activity and is the backbone of your accounting system. 17. Tax Deductions Tax deductions are expenses you can subtract from your income to lower your tax bill. (Want some crazy tax deduction examples? Check out these approved deductions!) 18. Budget A budget is your financial plan for a future period, showing your estimated revenue and expenses. It’s usually re-evaluated regularly to ensure it remains accurate and reflects the current state of your business. 19. Invoice An invoice is a bill you send to your customers for goods or services you’ve provided. It details what they owe you and when it’s due. 20. Bookkeeping Bookkeeping is the essential process of recording and organizing your business’s financial transactions. It’s about keeping a detailed record of every dollar that comes in and goes out, like customer payments and vendor bills. While it used to be done in physical ledgers, modern bookkeeping is largely handled by digital software, making it more efficient and accurate. So, there you have it, 20 accounting terms you need to know as

How Ryan Robinson & Justin Welsh Scaled Freelancing into a Six-Figure Business

Let’s face it: as a freelance content marketer, you’re up against stiff competition. The field is overflowing with talented individuals vying for the same opportunities. But don’t let that discourage you! Countless freelance content marketers are not just surviving, but thriving in this competitive landscape. Want to know how they did it? In this article, we’ll dive deep into the journeys of five successful freelance content marketers, uncovering the strategies and mindsets that propelled them to the top. Get ready to be inspired and learn how you can apply their lessons to your own freelance career. Table of Contents Ryan Robinson: From Failure to a $35K/Month Blog Empire Ryan Robinson wasn’t an overnight success—he built his empire from scratch. After multiple entrepreneurial failures, he took a different approach: documenting his journey. What started as a side project—RyRob.com—soon became a go-to resource for freelancers and entrepreneurs looking to grow online. With 500,000+ monthly readers and 250,000 email subscribers, Ryan has mastered the art of SEO, affiliate marketing, and content monetization. His blog now generates $25,000 to $35,000 per month, proving that strategic content creation is a powerful business model. But he didn’t stop there—he co-founded RightBlogger, a suite of 80+ tools for bloggers, filling the gap he wished existed when he started. Beyond his blog, Ryan has worked with LinkedIn, Zendesk, Adobe, Google, and other Fortune 500 brands, helping them grow through high-impact content marketing. His expertise has been featured in Forbes, Fast Company, Business Insider, and Entrepreneur. Here are some of his most impactful insights: “It takes time to make money blogging. In fact, it takes a good deal of time to make money blogging.” “You’ll Make Mistakes with a New Blog and That’s Okay (in Fact, it’s Vital)” “Quality is Much More Important than Quantity with a New Blog.” Justin Welsh: From Corporate Burnout to Million-Dollar Solopreneur Justin Welsh wasn’t just another corporate executive—he was a high-performing leader in the SaaS world. Over the last decade, he played a pivotal role in scaling two companies past a $1 billion valuation and helped raise over $300 million in venture capital. His expertise in growth, sales, and strategy made him a powerhouse in the startup ecosystem. But despite his impressive achievements, something was missing. By 2019, burnout had taken its toll. The relentless grind, high-pressure environment, and constant chase for the next milestone left him drained. He realized that while he was helping companies succeed, he wasn’t designing a life that fulfilled him. So, he made a bold move—he and his wife quit their high-paying jobs, packed up their lives, and moved to the Catskill Mountains in New York to start fresh. Rather than jumping into another corporate role, Justin decided to build something of his own. He turned his knowledge of business, marketing, and personal branding into a thriving one-person business. Starting with LinkedIn, he crafted a strategy of sharing actionable insights, industry wisdom, and personal reflections—consistently and authentically. Over time, he grew his audience to over 700,000 followers and became one of the most influential solopreneurs on the platform. But he didn’t stop at content creation. Justin monetized his expertise through digital products and coaching, focusing on simplicity and scalable systems. His courses, including The LinkedIn Operating System, have helped thousands of professionals build their brands and businesses. His model? One niche. One clear problem. One systematized solution. No unnecessary complexity. Justin’s Key Lessons for Solopreneur Success: “You should have a very “long game’ mentality.“ Start a side project. Build it to 60% of your salary. Then go all in.” “The solopreneur playbook is simple: One niche. 1,000 true fans. One solvable problem. One systematized solution. Everything else is just overcomplication.” “The most successful people I know don’t have better ideas. They have a higher tolerance for discomfort. They’re simply willing to sit in the mess longer than everyone else.” Miranda Marquit: From $5 Articles to Six-Figure Financial Writer Miranda Marquit’s journey as a freelance writer didn’t start with six-figure clients or prestigious bylines—it began with $5 keyword-stuffed articles for content mills. Like many freelancers, she started at the bottom, taking low-paying gigs just to gain experience. But she knew she couldn’t stay there. Instead of grinding away for pennies, she made a strategic decision to specialize in a lucrative niche: personal finance. At first, Miranda wrote for independent bloggers, gradually building her portfolio and credibility. As her expertise grew, she transitioned into corporate clients—banks, fintech firms, and investment companies that valued her deep knowledge of finance. With each step, she increased her rates, moving away from the content mills and into the world of high-paying clients. But it wasn’t just her financial expertise that set her apart—it was her commitment to quality, networking, and long-term relationships. Miranda actively engaged in finance writing communities, built strong professional connections, and positioned herself as a thought leader in her niche. Over time, she secured premium clients, established herself as a go-to financial writer, and turned her freelance work into a sustainable six-figure career. Miranda’s Takeaways for Aspiring Freelance Writers: “There are so many great opportunities, and I’d hate for people to be afraid to try just because they feel they don’t have the time.” “My favorite moments are when readers email to let me know that something I wrote taught them something new or encouraged them to think about money in a different way.” “Try to make those personal connections and, most of all, try to be useful. That personal connection really does make a difference.” Bani Kaur: The Fearless Freelancer Who Faked It Until She Made It “Can you write for our SaaS?” The voice on the other end asked. Without hesitation, Bani Kaur replied, “Yes, of course.” The truth was, she had never written about SaaS before. Up until that moment, her writing experience was rooted in architectural publications. But instead of letting inexperience hold her back, she hung up the phone and immediately Googled, “What is SaaS?”—and so began her crash course into the tech industry.

How to Build a Personal Brand as a Freelance Makeup Artist

Brides, performers, actors, models, and artists browse the internet, searching for that perfect makeup artist for their special occasions. You see countless portfolios filled with stunning transformations, each makeup artist (MUA) demonstrating incredible skill and creativity. But have you ever noticed how, despite all that talent, many seem to just blend into the crowd, feeling merely “good enough” rather than truly unforgettable? What’s that missing ingredient that elevates an artist from simply skilled to utterly essential? The truth is, beyond your technical prowess, there’s a powerful, often overlooked secret weapon: your personal brand. This isn’t about slapping on a logo or just posting pretty pictures. It’s about you, authentically. It’s about why clients don’t just like your work, but why they love you, connect with your vision, and trust you implicitly. Let’s uncover why makeup artist personal branding is the absolute key to not just standing out, but truly shining in this vibrant industry. Table of Contents The Power of Personal Branding: YOU In a competitive industry, it’s easy to fall into the trap of self-doubt: The market is saturated. I’m not good enough. Imposter syndrome is creeping in. If you feel like you have to act or be someone else to succeed in your business, remember this: don’t compare your seedling to someone else’s fully grown tree. What sets you apart from the competition is your personal brand—YOU. Your personal values, mission, likes and dislikes, messaging, and even the tone you use in communication all contribute to your uniqueness. No one else can be you. Think of Apple and Steve Jobs, Elon Musk and Tesla, or Gary Vaynerchuk and VaynerMedia. People don’t just buy products or services; they buy into the people, the vision, and the story behind them. The Know, Like, Trust Factor Have you ever noticed a brand for a long time, even when you didn’t need its service, and then turned to it when you finally did?Have you ever supported a business because of its story and values?Have you ever shared a business owner’s story because it resonated with you? Behind these experiences is the marketing principle Know, Like, Trust. It’s exactly what it sounds like—people need to know who you are, like you enough to stick around, and trust you so they feel confident buying from you—once, and then again and again. Here’s a quick exercise: Which of these actions help build the Know, Like, Trust factor? Yes, you got them all right! These are all effective ways to create an emotional connection with customers. Brand Building: Where to Start Now that we know personal branding is essential, what’s next? How do we build our own brand? Brand VisualsFor a makeup artist, showcasing your work is crucial. Your website and social media needs to show off your belief in the power of makeup and transformation. Show how makeup helps people capture precious moments and memories. Show the confidence your clients gain after your work. Beyond just a logo and headshots, it’s important to display how you help clients express their beauty in their own way. Let your potential clients watch your evolution as your skills grow with experience. Brand StoryYour brand isn’t just about your portfolio—it includes your brand story and messaging. This extends to all forms of communication: emails, blog articles, social media posts. The tone, content, and even hashtags contribute to your brand’s voice. Whether your brand is serious, playful, energetic, sentimental, or introverted, it’s all okay—just be yourself. One brand story that really inspires me is Danessa Myricks’. As a single mother of two, she needed a flexible career. Through extensive research and practice, she educated herself in makeup artistry. Today, Danessa Myricks Beauty represents more than just makeup—it’s about empowering individuals to express themselves creatively and confidently. Core ValuesShow up authentically in your messaging. Your website, Instagram captions, email responses—everything should reflect you, your core values, and your personality. People should experience you online first, and then meet the same you on their makeup date. Here’s an inspiring example from Danessa: “I didn’t want to just put makeup on people. I wanted people to feel the work. Because that’s what makes it different, and that’s always been what has driven me in my artistry and in the development of my style over the years. If they’re not feeling it, it’s not good enough.” — Danessa Myricks Make Use of Social Media and Your WebsiteShow up on your social media platforms and website. Don’t just promote your services—share glimpses of your life outside of business. Post about your pets, hobbies, or quirks. Not sure what to post on Instagram? Learn from experts like Michelle Phan and Charlotte Tilbury. Experiment, find your style, and most importantly, have fun with it! Consistently Show UpTo build Know, Like, Trust, consistency is key. You can share the best story ever, but if you don’t follow up, people will move on. Life gets busy—kids, work, and everything in between can make consistency tough. But sometimes, it’s our own ego getting in the way. If you post something and hear nothing back, it’s easy to feel like no one is listening. But the truth is, you never know who’s silently paying attention. Keep showing up—you never know who’s watching and ready to connect with what you bring to the table! Worried About Putting Yourself Out There? What if people don’t like me?When you share a distinct point of view, there will always be lovers and haters. While you may turn some people away, you will also attract the right ones. Not everyone has to like you, and that’s totally okay. I think I’m not perfect…These days, perfection isn’t expected. People appreciate authenticity. They want to see who you really are—what you’re reading, where you hang out on weekends. What if my posts get low engagement?Social media moves fast. If a post flops, it will soon be forgotten. And if needed, you can always delete it. Keep going and keep creating! Time to Act! It’s time to step

My Client Wants Another Revision?! (And How I Survived)

Ugh, revisions. We’ve all been there. You nail the brief—a sleek new logo, a killer website mockup, a brochure that’s chef’s kiss—and then… the client comes back with a laundry list of “minor” tweaks. “Can we just make the logo a little bigger? And maybe try a different shade of blue? Oh, and could we see what it looks like with a completely different font?” It’s the dreaded revision cycle that never ends, especially when a client acts like “unlimited revisions” is in the contract, even if it totally isn’t. As graphic designers, we get it. You want happy clients. You want them to rave about your work. But endless revisions are a profit-killer, a creativity-drainer, and a direct path to burnout. It’s like being trapped in a never-ending PSD file of doom. So, how do you deal with clients who seem to think “just one more tweak” is their God-given right? How do you set boundaries without sounding like a jerk? And, most importantly, how do you get paid for the extra work you’re doing? Let’s break it down. Why Unlimited Revisions Are a Disaster “Unlimited” anything is a bad idea, especially in design. Here’s why: Why Clients Think They’re Entitled to Unlimited Revisions Now that we understand why unlimited revisions are problematic, let’s explore why clients may expect them. Setting Boundaries and Charging for Extra Iterations Here’s how to take back control of your time and creativity: Any requests for additional meetings or design rounds, exceeding what is defined in this contract, may necessitate a modification to the estimated price and timeline of this project. This clause sets the stage for fair boundaries. Combine it with these specific points: Detailed Proposals: Before finalizing the contract, your proposal should clearly define the project scope, deliverables, milestones, timeline, and revision policy. This helps set client expectations upfront and avoids misunderstandings later. Here’s a sample: This clear structure helps clients see where revisions fit in and keeps the project on track. “Just a friendly reminder, this revision goes beyond what was included in the original agreement. I’d be happy to proceed at my hourly rate of $50/hour. Would you like me to send over an updated estimate?” Expand the use of time-tracking tools like Toggl or Clockify to monitor all revisions, even the included ones. These tools not only help justify your fees but also refine your pricing for future projects by providing clear data on how long each revision takes. Stop letting endless revisions drain your creativity and earnings. By setting clear boundaries, using structured feedback rounds, and leveraging time-tracking tools, you can stay in control while delivering top-notch designs. You’ve got this!

How to Price Your Rates as a Freelancer (Even With Inflation!)

Hey freelancers! Figuring out your rates can be a bit of a hassle, especially with prices for everything—from coffee to gas—on the rise. Whether you’re new to freelancing, juggling side gigs, or working full-time, nailing your pricing strategy is essential to building a thriving career. Let’s break it down into simple steps so you can keep up with inflation and get paid what you’re worth. 1. Know Your Worth and Your Costs First off, you’ve got to figure out what your work is worth. Here’s how to get started: Once you have a clear picture of your costs and the market, you can set a base rate that covers your expenses and reflects your value. Don’t undersell yourself—your time and skills are worth it! 2. Price for Profit Covering your costs is just the start. Build in a profit margin to account for expenses like software, ads, and taxes. For instance, if your base rate is $20/hour to cover costs, adding a 20% profit margin would bring it to $24/hour. This extra margin allows you to invest in your business or save for slow periods. As you gain experience and improve your skills, don’t be afraid to increase your profit margin to reflect the added value you bring. 3. Add an Inflation Buffer Inflation reduces the value of money, so it’s crucial to adjust your rates to keep up with rising costs. For example, if the prices of essential tools like software subscriptions or supplies increase, your earnings might not cover your expenses unless you adjust. Keeping your rates updated helps you stay on top of rising costs. Here’s how: Inflation impacts your earnings. For example, if your rate is $20/hour and inflation is 3%, increasing your rate to $20.60/hour keeps your purchasing power intact. Reviewing your rates annually ensures you stay ahead of rising costs. 4. Communicate Changes Clearly If you’re raising your rates for existing clients, explain your unique contributions clearly. For instance, graphic designers can show how their work boosts sales or strengthens branding, while content writers might highlight metrics like higher engagement or increased traffic. Demonstrating tangible results justifies your rate increase and reinforces your value. Let clients know in advance. Here’s an example of what you could say: Hi [Client Name], I’ve loved working with you on [Project/Service]! Over the past [time period], my work has helped deliver [specific achievement, e.g., 20% more followers, better engagement rates, or improved results]. To continue providing this level of quality and support, I’m updating my rates to reflect current market conditions. Starting [Date], my new rate will be [$XX]. Thank you for your understanding and support! Most clients will appreciate your transparency and professionalism. 5. Offer Packages or Retainers Inflation can make one-off projects feel unpredictable, but offering packages or retainers can create stability for both you and your clients. For example: These options make your pricing more appealing while ensuring consistent income. Setting your freelance rates doesn’t have to be intimidating, even with inflation making things tricky. By understanding your costs, building in a profit margin, and communicating your value effectively, you’ll stay ahead of the game and thrive as a freelancer. How do you plan to update your rates? Start today and take control of your freelance career. Your hard work and skills deserve to shine!

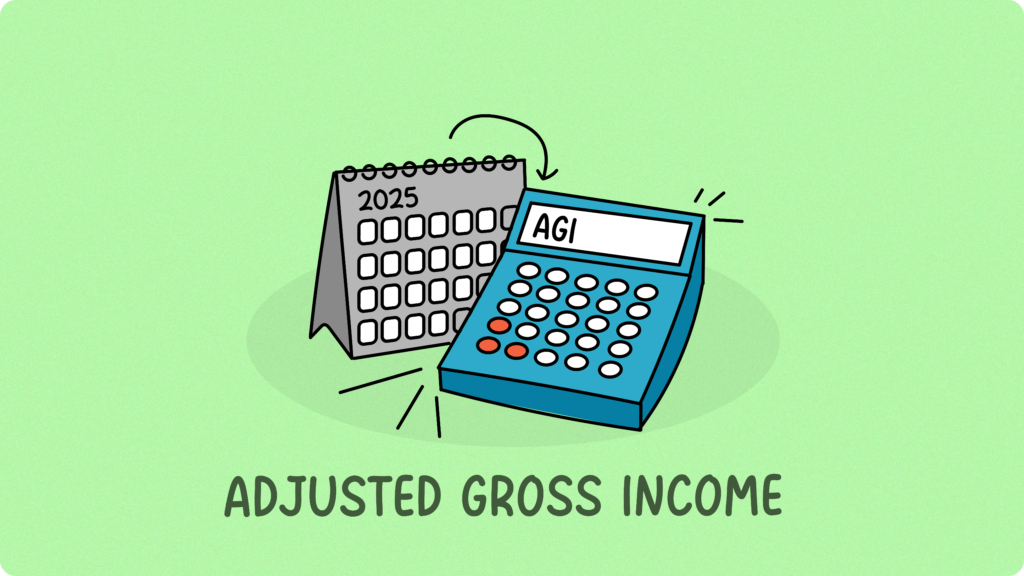

What Is Adjusted Gross Income (AGI) and why should freelancers care?

If you’re a brand-new freelancer just stepping into the world of taxes, you’ve probably come across the phrase “Adjusted Gross Income” (AGI) at some point. Don’t worry if it sounds intimidating—AGI is simply a fancy term that helps the IRS figure out how much of your income is actually taxable. Think of it like peeling layers off an onion until you get to the core number that truly matters for your taxes. So, what is AGI exactly? Your AGI is basically your total income for the year minus some specific deductions. Start with the money you made from all your work—whether that’s freelance writing gigs, design projects, or coding contracts—plus any other income sources like interest earned from a business savings account. That gives you your gross income. From there, you subtract certain qualified expenses (we’ll go over some common ones in a second). The number you’re left with after subtracting these allowed deductions is your Adjusted Gross Income. Why does AGI matter? Your AGI is a starting point for figuring out how much tax you owe. The IRS uses your AGI to figure out if you qualify for certain tax credits, deductions, or other breaks. In short, it’s the number that tells the IRS, “This is how much I really earned after the most basic deductions.” The lower your AGI, generally speaking, the less tax you’ll pay. Common deductions that affect Your AGI As a freelancer, you get to subtract some pretty useful stuff to lower your AGI. Here are a few common ones: Keep in mind, there are specific IRS rules for these deductions, and not everyone qualifies. But if you do, they’re a handy way to trim down that number and potentially save some money. How to Find Your AGI If you use a tax software or pay a professional, they’ll automatically crunch the numbers for you. But here’s the basic formula: Gross Income – Above-the-Line Deductions = Adjusted Gross Income (AGI) Here’s an example to show you how it all comes together: Item Amount Freelance Income $60,000 Self-Employment Tax $9,000 Self-Employment Deduction -$4,500 (50% from self-employment tax) IRA Contribution -$3,000 HSA Contribution -$2,000 Adjusted Gross Income $50,500 Wrapping it up For many new freelancers, taxes feel like a giant, tangled mess of complicated terms. But understanding key concepts like AGI can make the whole process feel a lot less scary. Keep in mind that your AGI serves as a building block for figuring out your overall tax situation. The more you understand it, the more control you’ll have over how much you pay—or don’t pay—at tax time. As you get comfortable with these basics, you’ll find that tax season isn’t as overwhelming as it first appears. And remember, if you’re ever unsure, talking to a tax professional or using trusted tax software can give you the peace of mind you need.

Self-Employed? Here’s How to Handle Taxes Like a Pro

So, you’ve joined the self-employment squad—congrats! Being your own boss is awesome, but let’s talk about the not-so-fun part: taxes. Managing your self-employed taxes doesn’t have to be a headache, though. Here’s the lowdown to help you save money, stay organized, and avoid any awkward IRS letters. What’s the Deal with Self-Employment Taxes? Here’s the kicker: when you’re self-employed, you pay more taxes. Why? Because you’re both the employee and the boss. That means you’re covering the full 15.3% Social Security and Medicare taxes. Ouch, right? Unlike regular employees, you don’t get taxes taken out of your paycheck—you’ve got to handle it yourself. Oh, and the IRS expects you to pay quarterly, not just at tax time. Quarterly Taxes: Love Them or Hate Them, They’re Mandatory Quarterly taxes are your “pay-as-you-go” system. Four times a year, you send Uncle Sam an estimate of how much you owe. Skip them, and you could face penalties. Pro Tip: Use a budgeting app or a spreadsheet to keep tabs on your income and estimate what you’ll owe. Better safe than sorry! Freelancer Tax Hacks You Need to Know Keep more of your hard-earned cash with these deductions: To check out more about which items can be tax-deducted, head over to our blog detailing everything you need to know! Tax Nightmares to Dodge Help! I Missed My Quarterly Payments! Uh-oh. If you didn’t pay enough, the IRS might hit you with penalties. Sometimes they’ll let you set up a payment plan, but why risk it? Stay ahead of the game, and you’ll sleep way better. Budget Like a Boss Monthly money check-ins = no surprises. Get yourself some accounting software, or at least a spreadsheet, and track those dollars. Bonus points if you save your receipts digitally (hello, organized life!). Stay on top of your taxes, and focus on what truly matters—growing your business. Do You Need a Tax Pro? If your taxes are pretty simple, doing them yourself might be just fine. But U.S. tax rules can get confusing fast. There’s that strict $25 gift limit, entertainment deductions, and tons of tiny details you could accidentally miss. Add in the risk of late lings, penalties, or overlooking new updates, and it’s easy to get in over your head. If your budget allows, hiring a pro (like a CPA) can make a huge difference. They’ll help you with the best deductions, keep you on top of the rules, and ensure you never sweat a deadline again. Think of it as an investment that saves you time, keeps more cash in your pocket, and spares you a whole lot of stress. Bringing It Home Taxes don’t have to suck. Stay on top of them, know your deductions, and keep your books tidy. The goal? Less stress, more focus on building that dream biz. Now go crush it—your taxes (and your business) are in good hands.

The Freelancer’s Guide to Tax Deductions: Keep More of Your Cash

Hey there, freelancer! Tax season doesn’t have to be scary, especially when you know how to use deductions to keep more of your hard-earned money. Here’s a simple official guide to the most common expenses freelancers can claim to lower their tax bill. We’ll also clarify if everyday items like meals, cable TV subscriptions, or books can be claimed. Let’s dive in! 1. Home Office Space Got a dedicated spot at home where you work your magic? Whether it’s a full room or just a cozy corner, you can deduct a portion of your rent or mortgage, utilities, and even internet costs. Use the simplified method to claim $5 per square foot, up to 300 square feet. It’s easy and avoids complicated calculations. Just make sure it’s used exclusively for work—no Netflix binging allowed! IRS Rule: To qualify for this deduction, your home office must be your principal place of business, and the area must be used regularly and exclusively for work. 2. Tools of the Trade Need a laptop, software, fancy camera, or even a printer for your work? These are deductible! Even smaller items like notebooks, pens, or that ergonomic chair count too. Basically, if you’re using it for work, it’s probably deductible. Keep receipts for everything—even for that mouse pad with the wrist support. IRS Rule: Equipment and tools used for business can often be fully deductible in the year of purchase under Section 179, or depreciated over time if the cost is significant. 3. Business Travel and Mileage Driving to a client meeting or picking up supplies? Track your mileage. You can deduct the cost of work-related travel, whether it’s by car, plane, train, or even bike. Hotels and meals during business trips? Those count too! Use an app to track your miles—it’ll save you a ton of time and hassle. IRS Rule: The standard mileage rate for 2023 is 65.5 cents per mile. Keep a detailed log of your business-related travel, including dates, mileage, and purpose. 4. Health Insurance Premiums Freelancers pay for their own health insurance, and guess what? You can deduct those premiums, up to 100% of the cost if you’re self-employed and not covered by any other plan. This deduction can be a huge help when you’re juggling all the other costs of being self-employed. Just be aware that this deduction applies to health, dental, and long-term care premiums for yourself, your spouse, and dependents. IRS Rule: This deduction is claimed on Form 1040, Schedule 1, and cannot exceed your net self-employment income. 5. Marketing and Advertising Spent money on promoting your services? Ads, social media boosts, website hosting, and even business cards can all be deducted. If it helps you land clients, it’s fair game. IRS Rule: Any expense directly tied to promoting or advertising your business is deductible under ordinary and necessary expenses. 6. Professional Services Got an accountant or lawyer helping you out? Their fees are deductible. Paying for a coworking space? Deduct that too. These are essential costs of running your business. Keep contracts or invoices as proof of these expenses. IRS Rule: Professional fees for services that are ordinary and necessary for your business operations are deductible. 7. Education and Training Sharpening your skills with an online course, workshop, or certification? Deduct those fees! Books and training materials count too. Just make sure the education is directly related to your freelancing work. For example, a pottery class for a graphic designer? Probably not. A Photoshop course? Absolutely! IRS Rule: Education expenses must maintain or improve skills required in your business or be required by law to maintain your professional status. They cannot qualify you for a new trade or business. 8. What You Can’t Deduct Not everything counts as a business expense. Here are some common items that usually can’t be deducted: Always ask yourself: “Is this expense directly related to my work?” If the answer is no, it’s likely not deductible. TL;DR Quick Reference Table Deductible Non-deductible Home office space Personal home décor Business equipment & tools (laptop, software) Personal electronics (gaming consoles) Work-related travel & mileage Personal leisure travel Health insurance premiums Personal gym memberships Marketing & advertising (ads, business cards) Cable TV subscription for entertainment Professional fees (accountants, lawyers) Bribes, kickbacks, political contributions Education & training related to your field Hobby classes unrelated to your work (e.g. pottery) Business meals (with clients) Meals for personal enjoyment Books related to skill development Books for leisure Specialized uniforms & safety gear General clothing Gifts up to $25 per recipient Non-deductible amount: Any portion of a business gift exceeding $25 per recipient Final Thoughts Taxes don’t have to be a headache. By keeping track of these common deductions, you’ll not only save money but also feel more in control of your finances. Start tracking your expenses and keeping those receipts handy—every bit counts! For more tips on managing self-employment taxes, check out our blog, Self-Employed? Here’s How to Handle Taxes Like a Pro. (Remember, these are just some common examples—there’s plenty more out there. If you’re not sure about a specific expense or think we’ve missed something, just check out the IRS website or talk to a tax pro for the full scoop.) Happy freelancing!