10 Time-Saving Accounting Automations Every Small Business Owner Should Implement

As a small business owner or freelancer, your time is your most valuable asset. Between managing clients, delivering services, and growing your business, bookkeeping can feel like a relentless time sink. Manual tasks like invoicing, expense tracking, and payroll eat up hours that could be spent on high-value work. Fortunately, accounting automation is transforming how small businesses manage finances, offering time-saving accounting tools that streamline processes and boost efficiency. According to the 2024 Intuit QuickBooks Accountant Technology Survey, nearly all (98%) respondents say they’ve used AI to help clients over the last 12 months, with top applications including data entry and processing (69%), fraud detection and prevention (51%), and real-time financial insights (47%) For small business owners, adopting the best accounting automation for small business can save hours each week, reduce errors, and free you to focus on growth. This guide explores 10 time-saving accounting automations every small business owner should implement. From automating bookkeeping to streamlining tax prep, these tools will help you automate small business finances with ease. Whether you’re a solo freelancer or running a small team, these solutions will keep your finances on track. Table of Contents Why Accounting Automation Matters for Small Businesses Small businesses face unique financial challenges: limited budgets, complex tax rules, and the need to stay competitive. Manual accounting tasks not only drain time but also increase the risk of errors that can lead to costly penalties. A Tech.co survey found that 75% of accountants reported a positive impact from automation, citing time savings, improved productivity, cloud access, enhanced data accuracy, and faster data retrieval as key benefits. Accounting automation uses software and AI to handle repetitive tasks like data entry, invoicing, and reporting, freeing you to focus on strategic priorities. The Rightworks Accounting Firm Technology Survey 2024 revealed that early adopters of automation earn 39% more revenue per employee, proving its impact on profitability. By adopting small business accounting software with automation features, you can: With the right time-saving accounting tools, you can automate small business finances and focus on what matters most—growing your business. ear and leveraging data, you can take your nonprofit to new heights. 10 Time-Saving Accounting Automations to Implement Here are 10 easy bookkeeping automation solutions to streamline your small business finances: 1. Automated Invoicing Manual invoicing demands significant effort and often leads to payment delays due to errors. Automated invoicing tools streamline the process by creating, sending, and tracking invoices instantly, ensuring timely payments. A PayStream Advisors study found that companies using automated invoice processing increased productivity by 33% and reduced processing costs by 42%. 2. Expense Tracking Automation Manually logging receipts requires considerable time and increases the risk of oversight. Small business expense tracking automation syncs bank transactions and categorizes expenses in real time, eliminating manual entry and ensuring accurate, up-to-date records. 3. Payroll Automation Manually processing payroll—calculating wages, taxes, and deductions—is time-intensive and error-prone. Payroll automation ensures accurate, timely payments while maintaining compliance. According to the American Payroll Association, automation can reduce payroll processing costs by up to 80%. 4. Bank Reconciliation Reconciling bank accounts manually is a tedious process that often results in errors. Automated reconciliation matches transactions between your books and bank statements, ensuring precision. According to HighRadius, 95% of reconciliation errors stem from manual mistakes. 5. Tax Preparation Automation Tax season can overwhelm small business owners with complex deductions and filing requirements. Automating bookkeeping for taxes simplifies the process by organizing deductions and generating accurate reports for seamless compliance. 6. Accounts Payable Automation Manually processing vendor bills is inefficient and prone to delays. Accounts payable (AP) automation streamlines bill payments and approvals, enhancing operational efficiency. A Payouts.com report found that automated AP solutions can cut invoice processing times by up to 80%. 7. Accounts Receivable Automation Chasing late payments consumes valuable time and disrupts cash flow. Accounts receivable (AR) automation sends reminders and tracks overdue invoices, improving collections. According to NetSuite, 85% of CFOs at companies with over 50% automated AR processes saw a decrease in days sales outstanding (DSO). 8. Financial Reporting Automation Manual financial reporting is labor-intensive and susceptible to errors. Automated reporting generates real-time insights, such as profit and loss statements, with minimal effort. PWC states that automation can reduce financial reporting time by 30–40%. 9. Time Tracking Integration Manually tracking billable hours is a challenge for service-based businesses, often leading to inaccurate billing. Automated time tracking streamlines invoicing and payroll processes by seamlessly integrating with accounting systems. 10. Budgeting and Forecasting Automation Manual budgeting is complex and quickly outdated, hindering effective financial planning. Automated budgeting tools simplify cash flow projections and performance tracking for agile decision-making. TL;DR: Summary of Time-Saving Accounting Automations The following table summarizes the best accounting automation for small business, highlighting key benefits and time-saving accounting tools to streamline your finances. Automation Key Benefit Example Tools Automated Invoicing Improves cash flow QuickBooks, Xero, FreshBooks, Fynlo Expense Tracking Automation Simplifies receipt management Expensify, Zoho Expense, Receipt Bank Payroll Automation Ensures accurate payments Gusto, ADP, Paychex Bank Reconciliation Enhances data accuracy QuickBooks, Wave, Xero Tax Preparation Automation Eases tax season workload TurboTax, TaxAct, H&R Block Accounts Payable Automation Streamlines bill payments Bill.com, Tipalti, Melio Accounts Receivable Automation Speeds up payment collection FreshBooks, Zoho Invoice, Invoice Ninja Financial Reporting Automation Delivers real-time insights QuickBooks, Sage Intacct, NetSuite, Fynlo Time Tracking Integration Boosts billing efficiency Toggl, Harvest, Clockify Budgeting & Forecasting Simplifies financial planning Float, PlanGuru, QuickBooks What’s Next Implementing these 10 time-saving accounting automations can transform how you manage your small business finances. From automating invoicing to forecasting cash flow, these easy bookkeeping automation solutions save hours each week, reduce errors, and empower you to focus on growth. Ready to streamline your finances? Our time-saving accounting tools offer real-time tracking, seamless integrations, and powerful automation to boost your business. Schedule a call with our team to discover how we can help you save time and grow smarter. [Schedule a Call] For more financial management tips, check out our blogs:

What is an Invoice? (And How to Create One)

Getting paid on time doesn’t have to be a struggle! Creating clear and professional invoices is the first step towards reliable income. In this article, you’ll learn exactly what an invoice is and how to create one that helps you get paid faster. Table of Contents What is an Invoice? An invoice is a formal document you send to customers requesting payment for the goods or services you’ve provided. It provides a detailed breakdown of the costs involved, including individual items or services, quantities, rates, and any applicable taxes or discounts. It tells your customer everything they need to know to pay you by the specified due date. It’s important to remember that invoices are different from quotes (estimates of cost) and receipts (proof of payment). Creating an Effective Invoice: A Step-by-Step Guide with Sample Want to get paid faster and keep things running smoothly with your clients? Here are some key best practices to keep in mind, referencing the sections you’ll typically find on a professional invoice like the one below: Top Tips for Smoother Invoicing Want to make invoicing easier for both you and your clients? Here are some key best practices to keep in mind: What’s Next? Invoicing doesn’t have to be complicated or time-consuming, and it definitely shouldn’t stand between you and getting paid. By creating clear, professional invoices and following a few simple best practices, you can reduce delays, avoid misunderstandings, and maintain smoother relationships with your clients. Start creating your next invoice with confidence. Fynlo offers professional templates and flexible editing tools to help you build, send, and track invoices that get you paid faster. Find out more about Fynlo and see how easy invoicing can be.

5 Areas You Need to Automate Your Finance

It’s 9 in the morning, and after that first essential cup of coffee, the busy day begins. You gather all those slips of paper and digital documents, which already feels like a full task in itself. After carefully reviewing every detail, you finally finish creating invoices, recording financial transactions, and confirming payment statuses. Before you know it, it’s almost noon. The tedious accounting tasks have already consumed half your day, and you’re still not finished. Does any of this sound familiar? When you’re handling finances manually, things can quickly pile up, leading to those frustrating errors, the anxiety of delayed payments, and that constant feeling of your valuable time and energy just disappearing. If this resonates with your experience, read on to discover the power of automated finances and invoicing, especially when integrated with your accounting software and invoicing software. Table of Contents Is Your Manual Finance Process a Struggle? Here’s a quick check to see if automated finances might be necessary for you: If you recognize two or more of these pain points, you’ll likely be eager to learn more about what automated finances can offer: Don’t worry, these struggles are common. In fact, you’re like the majority of small businesses and freelancers still navigating the complexities of manual finances. Let’s explore how automation can change that. The Power of Automated Finances and Invoicing Automated finances and invoicing use technology to handle everyday financial tasks. This includes things like creating invoices, sending payment reminders, tracking payments, and managing cash flow – without needing you to do it all manually. It replaces time-consuming spreadsheets, repetitive data entry, and paper-heavy processes with smooth, digital workflows. Essentially, financial automation lets your financial tasks run like a well-oiled machine in the engine room, operating consistently without constant attention. This ensures invoices go out on time, reminders are sent automatically, and financial data is recorded accurately, all without you having to chase. Why It’s Powerful Key Areas of Financial Automation Financial automation goes beyond invoicing. It touches nearly every part of your financial workflow. When routine tasks are handled by smart systems, you save time, reduce errors, and gain clearer insights. Your Action Plan for Financial Automation Ready to move beyond the manual invoicing process? Here’s a simple roadmap to get you started: Ready to Streamline Your Financial Workflow? Let’s talk. We’ll help you find the right automation tools, like invoicing systems that integrate directly with your accounting platform, simplify your process, and set your business up for scalable success.

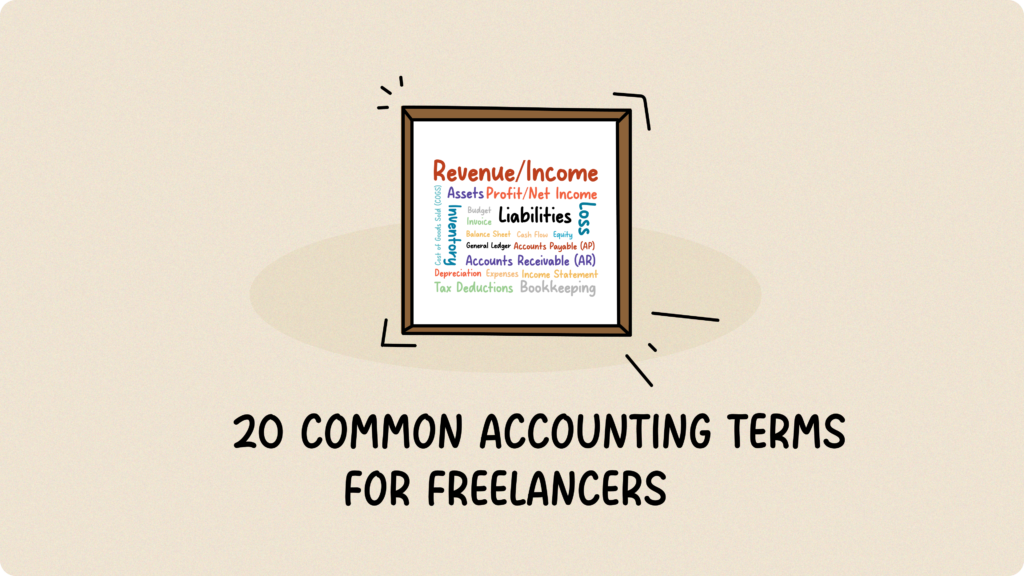

20 Common Accounting Terms for Freelancers

Running a business, big or small, means dealing with numbers. But for many of us with not much accounting background, those accounting terms can feel like a foreign language. Here’s the thing, Go Remotely’s Accounting Statistics say that 60% of small business owners don’t feel knowledgeable about finances and accounting. Don’t worry, you’re not alone. This guide breaks down 20 essential accounting terms every freelancer or small business owners needs to know. Let’s make sense of the numbers together. Your Financial Glossary Let’s dive into each term, starting with: 1. Revenue/Income Revenue is simply the total money your business brings in from sales or services. Think of it as your gross income, before you subtract any expenses. 2. Expenses Expenses are what you spend to keep your business running and generate revenue. Here are the main types: 3. Profit/Net Income Profit is essentially the financial gain your business achieves when your revenue, the money you bring in, surpasses your expenses, the money you spend. To put it simply, it’s what you get to keep. So, for example, if your business generated $10,000 in revenue and you incurred $6,000 in expenses, you’d end up with a profit of $4,000. 4. Loss A loss is the opposite: when your expenses are higher than your revenue. If you spent $8,000 and only made $5,000, you’ve got a $3,000 loss. This trend is not sustainable in the long term. 5. Assets Assets are anything your business owns that has value, from cash and equipment to your laptop or even your website and intellectual property. 6. Liabilities Liabilities are what your business owes to others, like loans, supplier payments, and credit card balances. 7. Equity Equity is essentially your net worth in the business. It’s what would be left if you sold all your assets and paid off all your debts. 8. Cash Flow Cash flow is the movement of money in and out of your business over a period of time. It’s about having enough cash on hand to pay the bills. Even profitable businesses can struggle with poor cash flow. (Check out our blog on Cash Flow Projection!) 9. Accounts Payable (AP) Accounts Payable (AP) represents the money your business owes to suppliers or other creditors for goods or services received but not yet paid. For instance, if you’ve received inventory or supplies on credit and haven’t paid the invoice yet, that amount is considered Accounts Payable. 10. Accounts Receivable (AR) Accounts Receivable (AR), on the other hand, is the money your customers owe your business for goods or services you’ve already delivered or provided. It’s the opposite of Accounts Payable; it’s money coming in. For example, if you’ve sent an invoice for $500 for services rendered and the customer hasn’t paid yet, that $500 is an Accounts Receivable. It’s important to track AR carefully, as it directly impacts your cash flow and ability to cover your own expenses. 11. Inventory Inventory refers to the goods your business holds for sale. It’s the items you have on hand, ready to meet customer demand. In essence, effective inventory management is crucial. You don’t want to run out of stock and lose sales, but you also don’t want too much stock sitting around, which leads to waste and ties up your capital. 12. Depreciation Depreciation is the gradual loss of value of your assets over time, like a restaurant oven getting older. It’s recorded as an expense on your income statement. 13. Cost of Goods Sold (COGS) COGS is the direct cost of producing your goods, including materials and labor. For a restaurant, it’s the cost of ingredients and food preparation. For an online shop selling handmade crafts, it’s the cost of raw materials like fabric and yarn, plus the labor involved in creating the finished products. 14. Balance Sheet A balance sheet is a financial picture of your business at a specific moment, showing what your business owns (your assets), who your business owes money to (your liabilities), and how much you, the owner, have invested (your equity). It’s based on the equation: Assets = Liabilities + Equity. (Learn more about balance sheets here.) 15. Income Statement An income statement shows your business’s revenue, expenses, and profit or loss over a specific period (e.g., a month or a year). It tells you how well your business performed during that time. So, how does it differ from a balance sheet? Well, a balance sheet provides a snapshot of your business’s financial position at a specific moment, while the income statement focuses on your performance over time. They work together to give you a full picture of your financial health. 16. General Ledger The general ledger is the comprehensive record that organizes all your business’s financial transactions. Imagine it as a detailed logbook of every financial event, categorized by type, such as sales, expenses, and asset changes. This organization makes it easy to see the complete picture of your business’s financial activity and is the backbone of your accounting system. 17. Tax Deductions Tax deductions are expenses you can subtract from your income to lower your tax bill. (Want some crazy tax deduction examples? Check out these approved deductions!) 18. Budget A budget is your financial plan for a future period, showing your estimated revenue and expenses. It’s usually re-evaluated regularly to ensure it remains accurate and reflects the current state of your business. 19. Invoice An invoice is a bill you send to your customers for goods or services you’ve provided. It details what they owe you and when it’s due. 20. Bookkeeping Bookkeeping is the essential process of recording and organizing your business’s financial transactions. It’s about keeping a detailed record of every dollar that comes in and goes out, like customer payments and vendor bills. While it used to be done in physical ledgers, modern bookkeeping is largely handled by digital software, making it more efficient and accurate. So, there you have it, 20 accounting terms you need to know as

10 Signs of a Bad Bookkeeper to Absolutely Avoid

Whether you’re a startup or a growing small business, knowing your financial status is key to keeping your business on track. Whether you work with bookkeeping software that offers support, a part-time bookkeeper, or external accountants, it’s crucial to ensure they are doing their job properly, making your life easier, not harder. Good bookkeepers are your financial peace of mind, keeping things organized and making sure you are compliant. But bad ones can drain your profits and intensify your tax nightmares. Is your bookkeeper the right fit? Read on for 10 troubling signs that it may be time to find a new bookkeeping solution. 10 signs of a Bad Bookkeeper Why Fynlo is a Trusted Solution If you’ve recognized one (or more) of the signs of a bad bookkeeper in your current service, it’s time to consider a reliable alternative. At Fynlo, we understand the challenges of financial management firsthand. That’s why we’ve built an intuitive platform designed to simplify your financial life and put you back in control. Fynlo provides access to seasoned accounting professionals. Our junior accountants bring over five years of experience, while our senior accountants boast more than ten years, most honed at top-tier firms like the Big Four, Baker Tilly, BDO, and Grant Thornton. We also prioritize confidentiality and data security. Every client relationship includes a signed Non-Disclosure Agreement (NDA), so your sensitive financial data is protected at all times. Here’s how Fynlo can benefit your business: Click here to schedule a call with our expert and take the stress out of bookkeeping. Fynlo team can handle everything from categorizing your transactions and reconciling your accounts to delivering precise, tax-ready financial statements.

Retained Earnings for Freelancers

As a freelancer, you juggle more than just projects—you’re also in charge of running a business. Navigating fluctuating income, covering expenses, and planning for growth can feel overwhelming. That’s where retained earnings come into play. In simple terms, retained earnings are the portion of your income that stays in your business after paying expenses and taking what you need for personal use. Think of it as your business’s savings account—a safety net and a springboard for growth. For freelancers, retained earnings are more than just a financial term; they’re a lifeline. They help you weather slow months, invest in your craft, and prepare for opportunities that come your way. By mastering retained earnings, you lay the foundation for a freelance business that’s resilient and poised for long-term success. This article explains the role of retained earnings, offers tips for tracking them, shares strategies for financial stability, and covers key tax considerations. With the right steps, freelancers can build a strong, sustainable business. Why are Retained Earnings important for freelancers? Retained earnings (RE) for a freelancer represent the portion of his income that remains in the business after covering all expenses and withdrawing personal income. Unlike a traditional salary, retained earnings are profits set aside and reinvested into the business to support growth, maintain stability, and prepare for unexpected challenges. For freelancers, this could mean allocating funds for essential tools, marketing efforts, skill development, or creating a financial safety net for slower work periods. The concept of retained earnings varies significantly between freelancers and traditional businesses due to differences in structure, financial management, and long-term goals. This table provides a detailed comparison, assuming freelancers operate as sole proprietors or partnerships rather than LLCs. While businesses formally calculate and report retained earnings in financial statements, freelancers handle them informally, focusing on personal development, savings, and tools for business sustainability: Freelancers Businesses Legal structure Typically sole proprietorship or partnership, rarely LLC Commonly LLC or corporation Management formality Informal — Retained earnings are tracked personally or through simple systems Formal — Retained earnings are officially recorded in structured accounting systems RE formula Total Income – Expenses -Withdrawals Beginning retained earnings + Net Income – Dividends Paid RE tracking Managed through personal bookkeeping or basic software Monitored using professional accounting systems and formal financial records Reporting Reported on the freelancer’s balance sheet Officially reported on the corporate balance sheet under the equity section Taxation Included in personal income tax filings Subject to corporate income tax regulations Purpose Used for emergency funds, skill development, or stability during slow periods Reinvested for business growth, expansion, debt reduction, or dividend distribution Use of Funds Focused on purchasing tools, marketing, or savings for operational needs Directed toward business expansion, R&D, or other strategic initiatives Dividend distribution Not applicable — earnings are withdrawn as personal income May be distributed to shareholders as dividends How to Calculate Retained Earnings The formula for calculating retained earnings for freelancers over a year is as follows: Retained Earnings = Total Income − Business Expenses − Personal Withdrawals Where: Example: Let’s say you’re a freelance designer working on branding projects, website designs, and marketing collateral. At the end of the year, your financial details look like this: Using the formula: Retained Earnings = Total Income − Business Expenses − Personal Withdrawals Retained Earnings = $60,000 – $18,000 – $25,000 = $17,000 At the end of the year, you have $17,000 in retained earnings. This amount could be reinvested into upgrading your equipment, enrolling in a professional course, or saved as an emergency fund for slower months. Why Are Retained Earnings Important for Freelancers? For freelancers, retained earnings serve as a crucial foundation for financial resilience and business growth. By saving a portion of your income, you create a safety net that helps manage unpredictable income cycles, cover emergencies, and invest in opportunities to advance your career. From upgrading equipment to developing new skills or preparing for long-term goals like retirement, retained earnings are key to building a thriving and sustainable freelance business. 1. Financial Stability Freelancers often face fluctuating income, with some months being highly profitable and others quieter. Retained earnings act as a safety net, helping you manage your expenses during slower periods without financial stress. Example: As a wedding photographer, July to September are peak months, bringing in $15,000. To stay financially stable during the slower January to March period, you set aside $5,000 in retained earnings to cover expenses. This buffer helps you manage through the off-season with ease. 2. Emergency PreparednessUnexpected expenses can arise at any time, such as replacing a broken laptop, repairing a work tool, or dealing with unforeseen personal circumstances. Retained earnings give you the flexibility to handle these emergencies without disrupting your cash flow. Example: Suppose you’re a graphic designer and your primary design tool—your laptop—suddenly stops working. If you’ve set aside $2,500 in retained earnings, you can quickly buy a replacement without using credit or delaying projects for clients. This preparedness keeps your business running smoothly. 3. Business GrowthRetained earnings allow you to reinvest in your business to stay competitive and grow. Whether it’s purchasing better tools, upgrading your skills, or running a marketing campaign to attract new clients, having funds set aside makes growth possible. Example: You’re a freelance photographer who has been using a basic camera. With $3,000 in retained earnings, you invest in a high-quality camera and lens. This upgrade allows you to take on higher-paying clients who require professional-grade photography, boosting your income potential. 4. Upskilling and Professional DevelopmentThe freelance market is constantly evolving, and staying competitive often requires learning new skills or upgrading existing ones. Retained earnings can fund courses, certifications, or workshops that help you offer better services to clients. Example: As a web developer, you realize many clients are asking for expertise in React.js, but you only have basic knowledge of it. With $1,200 saved in retained earnings, you enroll in an advanced online course and improve your skills. As a result, you can take on projects requiring React.js and charge higher rates. 5. Managing Large Projects Freelancers sometimes need upfront