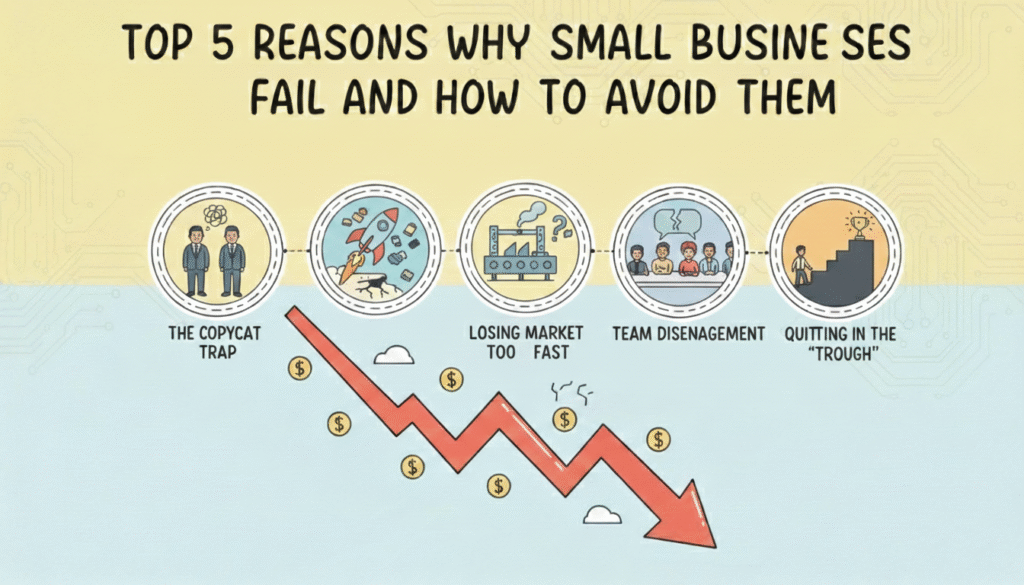

Top 5 Reasons Why Small Businesses Fail and How to Avoid Them

Starting a business is easily one of the most rewarding journeys you’ll ever embark on. There’s nothing quite like the rush of that first sale or the pride of seeing your logo on a real office door. Yet, for all the excitement, it’s also incredibly lonely and, at times, brutal. As we look toward 2026, the entrepreneurial spirit is louder than ever, yet the quiet reality remains: many small businesses struggle to stay afloat. According to 2024 data from the U.S. Bureau of Labor Statistics, nearly 50% of businesses fail within their first five years. We don’t believe failure is a foregone conclusion. Usually, it isn’t one giant catastrophe that sinks the ship; it’s a series of small, quiet cracks in the hull that no one noticed or wanted to see. In our experience watching what separates the survivors from the statistics, success often comes down to navigating a few specific, hidden hurdles. Here are the five real reasons businesses stall, and how you can navigate around them to build something that lasts. In this article 1. The Copycat Trap It starts with a seductive, familiar thought: “They’re making a killing, and I know I can do it better at a lower price.” It’s a common mindset that feels like a shortcut to success. You see a local leader or a big industry player and try to mirror their every move while undercutting their costs. This is the “Copycat Model,” and while it feels like a safe bet, it’s actually a trap. When you copy, you’re competing against someone who has more history, deeper pockets, and an established reputation. If your only way to win is to be “slightly cheaper,” you aren’t building a business; you’re operating on razor-thin margins that leave no room for error or future growth. When your only edge is price, any increase in your costs or a counter-move from a larger competitor can instantly wipe out your remaining profit. As Peter Thiel famously wrote in Zero to One: “The next Bill Gates will not build an operating system. The next Larry Page or Sergey Brin won’t make a search engine.” If you aren’t bringing something uniquely you to the table, you’re just holding a spot until someone with more capital decides to take it. You don’t need to reinvent the wheel, but you do need to give people a reason to choose yours. How to stay ahead: 2. Scaling Too Fast We’ve all felt that “first milestone” adrenaline. You’ve got your first big clients, you’ve hired a Virtual Assistant, and for the first time, the dream feels real. This can be the danger zone. It’s when founders get impatient and start pouring money into massive hiring sprees or new markets before their core engine is actually stable. The numbers are staggering: 74% of high-growth startups fail because they scaled prematurely, according to the Startup Genome Report. Take the story of Bench, the bookkeeping giant. They raised over $100 million, had a massive team, and were the darlings of the tech world. But despite the funding and the hype, the company eventually had to shut down its core operations. They scaled their burn rate before they mastered their efficiency. Scaling a broken process doesn’t make you bigger; it just makes your mistakes louder and much more expensive. How to stay ahead: 3. Losing Market Flexibility There is a thin, blurry line between being “persistent” and being “stubborn.” We often fall in love with our original vision, treating it like a sacred text rather than a living document. Take Kodak as a prime example. In 1975, one of their own engineers invented the first digital camera. But the leadership was so protective of their film business that they buried the tech. They clung to the past while the world moved on. This reluctance eventually led the once-dominant giant to file for bankruptcy in 2012, which serves as a powerful lesson that past success is no guarantee of future survival. Today, failing to pivot is just as risky. According to a report by CB Insights, 42% of startups fail because there is simply no market need, often because the founders were so busy building a “perfect” product that they forgot to check if anyone actually wanted it. If you stop listening to your customers because you’re too busy “staying true to your vision,” it’s easy for the path forward to get a bit blurry. How to stay ahead: 4. Team Disengagement A business isn’t a machine; it’s a collection of people. If the people lose their spark, the engine stalls. Most of us recognize the signs: the “silent office” where everyone is just going through the motions. Gallup’s research shows that engaged teams are 21% more profitable, yet so many founders treat culture as an afterthought. High turnover isn’t just an HR headache; it’s a massive financial leak. It costs an average of $6,000 to replace a single employee, but the loss of trust and institutional knowledge is even higher. When your team feels like they are just “clocking in,” they won’t have your back when things get difficult. How to stay ahead: 5. Quitting in the “Trough” Every entrepreneur eventually finds themselves in the “Trough of Sorrow.” It’s that long, quiet stretch after the initial excitement has worn off, but the big results haven’t arrived yet. It’s the 2 AM nights spent wondering if you’ve made a huge mistake. 53% of founders reported feeling burned out. That exhaustion often leads to “Premature Capitulation”—closing a perfectly healthy business simply because the founder is spent. There’s a nuance here: you should be flexible with your method (as we saw in Point 3), but you must be relentless with your mission. Success usually happens right after you’ve considered walking away. Thomas Edison said it best: “Many of life’s failures are people who did not realize how close they were to success when they gave up.” How to stay ahead: Building for the Long Haul Professionalism doesn’t have to cost money, but looking amateur will cost you opportunities. As your workload grows, tools that automate invoicing, reminders, and tracking can make a noticeable difference. Exploring a dedicated invoicing platform like Fynlo is a simple next step if you want fewer follow-ups and more predictable payments. Book a free demo to see how Fynlo might fit into your day-to-day.