When you first go full-time as a freelancer, your focus is naturally on delivery—landing contracts, hitting deadlines, and refining your craft. Legal paperwork often feels like a secondary chore, a task to be addressed “eventually.” However, the structure you choose today determines how much of your hard-earned profit you actually keep and how well your personal life is protected if a project ever faces a legal challenge. If you are billing significant amounts without a formal entity, you may be unintentionally risking your personal savings for the sake of administrative convenience.

Choosing a business structure is a trade-off between simplicity and security. For most freelancers, the transition from a Sole Proprietorship to an LLC or S-Corp is triggered by two specific milestones: reaching $50,000 in annual profit or taking on high-stakes contracts where a professional error could result in a personal lawsuit.

In this article

- The Real-World Cost of Legal Exposure

- Evaluating Your Structure Options

- Identifying the Financial Turning Point

- Maintaining Your Liability Protection

- Common Q&A

The Real-World Cost of Legal Exposure

These risks are more than theoretical; without a legal bridge between your business and your personal life, a simple mistake can become a financial catastrophe.

- The Copyright Oversight: A freelance web developer accidentally used a copyrighted image on a client’s high-traffic site. The resulting $150,000 settlement led to a lien against his personal property because he had no LLC to isolate the debt.

- The Technical Failure: A photographer was sued for $100,000 after a hardware failure destroyed irreplaceable wedding footage. Operating as a Sole Proprietor meant his personal savings were legally accessible to satisfy the judgment.

In both cases, an LLC would have acted as a circuit breaker, likely limiting the liability to the business’s assets rather than the freelancer’s life savings.

Evaluating Your Structure Options

Freelance Business Structures: A Quick Comparison Guide

1. The Sole Proprietorship

This is the default setting for anyone who begins working for themselves without formal filing. It is the path of least resistance, but it offers the least protection.

- The Advantage: It is simple to manage. You report your income on your personal tax return and do not need a separate business tax ID.

- The Risk: You carry 100% of the liability. Your personal assets are legally linked to any business debts or lawsuits.

2. The Limited Liability Company (LLC)

An LLC is a registered entity that exists separately from you as an individual. It is the standard for professional freelancers who want to safeguard their personal finances.

- The Advantage: It builds a protective barrier. If the business is sued, the claimant generally cannot reach your personal savings or your home.

- The Maintenance: It requires an initial state filing fee, an annual report, and a dedicated business bank account.

3. The S-Corp Election

An S-Corp is not a separate entity you register with the state, but a tax status you request from the IRS. It is the primary tool high-earning freelancers use to reduce their tax burden.

- The Advantage: Significant tax savings. Instead of paying 15.3% self-employment tax on your entire profit, you only pay it on the “salary” you draw, keeping the remaining profit FICA-free.

- The Maintenance: You must run a formal payroll, maintain more rigorous records, and file a separate corporate tax return.

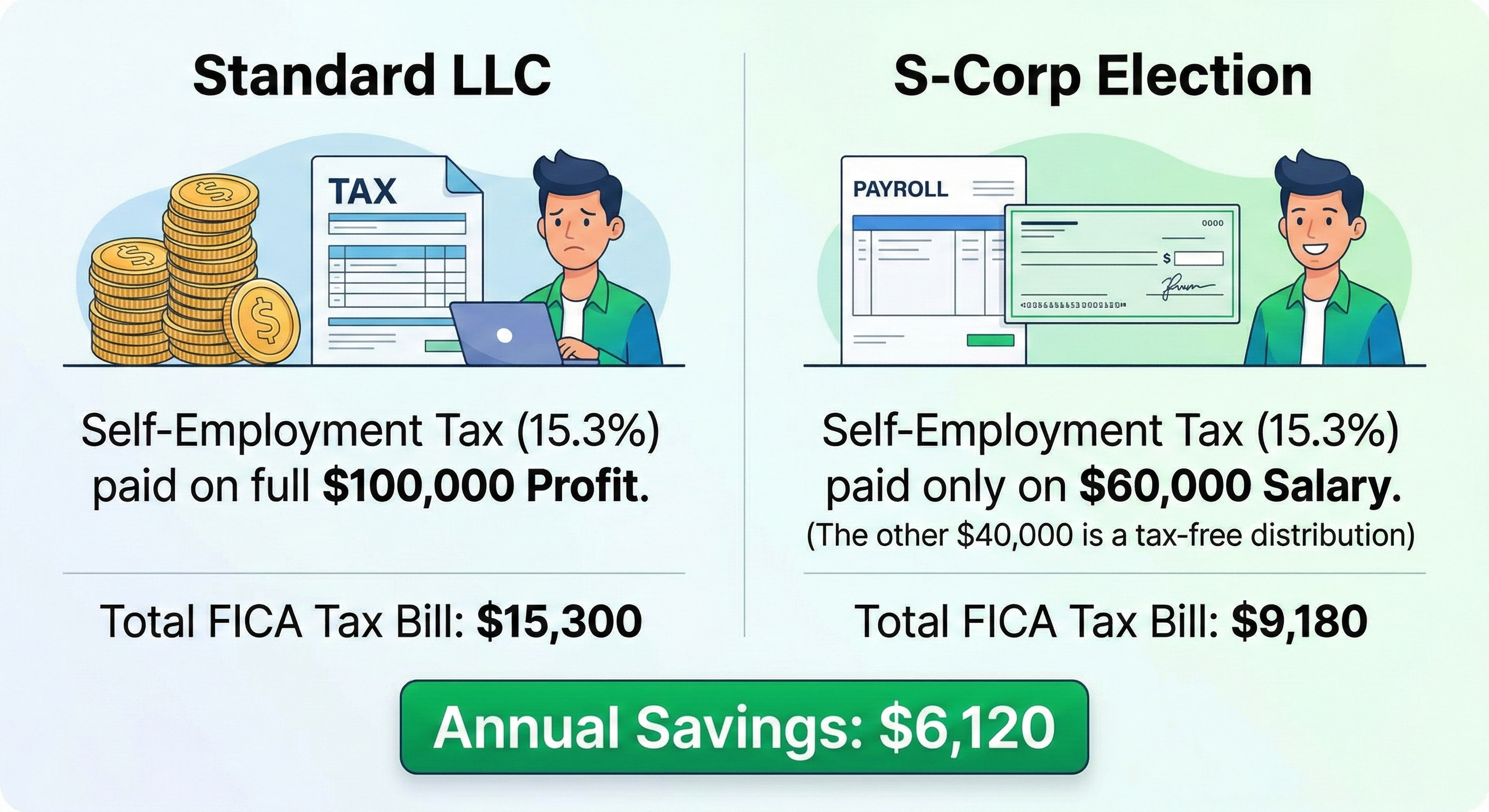

Identifying the Financial Turning Point

While the legal protection of an LLC is valuable at any stage, the tax benefits of an S-Corp become clear once you look at the math. Let’s compare the tax liability for a freelancer earning $100,000 in annual profit.

S-Corp vs. LLC: Visualizing the Tax Savings

| Structure | Self-Employment Tax (15.3%) | Total FICA Tax Bill |

| Standard LLC | Paid on the full $100,000 | $15,300 |

| S-Corp Election | Paid only on $60,000 (Salary) | $9,180 |

| Annual Tax Savings | $6,120 |

The Milestone: As a general rule, once your annual profit clears $75,000, the tax savings of an S-Corp usually outweigh the $1,500–$2,000 cost of professional accounting and payroll software. Until you reach that mark, a standard LLC provides the most efficient balance of protection and simplicity.

Maintaining Your Liability Protection

Registering an LLC is only the first step. If you treat your business account like a personal fund, a lawyer can argue in court that the business and the individual are one and the same. To keep your protection intact, adopt these three habits:

- Strictly Separate Finances: Use your business account only for business expenses. If you accidentally use your business card for a personal purchase, reimburse the company immediately and document the transaction.

- Sign Documents as an Entity: Never sign a contract with just your name. Always sign as “Your Name, Owner of [Your Business Name] LLC.” This reinforces that the agreement is with the company, not you personally.

- Keep an Annual Business Summary: Even as a solo founder, taking ten minutes each year to draft an Annual Business Summary is a vital protective measure. This simple, one-page document should list major milestones—such as signing a new lease, investing in significant equipment, or pivoting your services. In a legal dispute, this formal record serves as evidence that you are operating as a legitimate, separate business entity rather than an individual simply using a different bank account.

Common Q&A

1. Does an LLC protect me if I personally make a mistake on a project?

An LLC is not a “get out of jail free” card for professional negligence. If you are personally responsible for a major error—like accidentally deleting a client’s database—you can still be held liable. This is why the most professional approach is a “two-tier” strategy: use a Business Structure for debt and contract protection, and Professional Liability Insurance for your actual work-product.

2. I am just starting out—can I change my structure later?

Yes, and most freelancers do exactly that. It is common to start as a Sole Proprietorship for the first few months, register an LLC once contracts grow larger, and elect S-Corp status once profits stabilize above the $75,000 mark. Your legal structure should evolve alongside your income.

3. Do I need a lawyer to set this up?

For a single-member LLC, many freelancers file directly with their Secretary of State or use a registration service. However, if you have business partners or are moving toward an S-Corp, a 30-minute consultation with a CPA is a wise investment to ensure you are meeting all federal and local tax requirements.

4. How does my structure affect my ability to get a mortgage?

Lenders generally view S-Corp and LLC owners similarly as self-employed individuals. They typically look at your “net income” over the last two years. The main difference is that an S-Corp provides you with W-2s, which can sometimes make the application process feel slightly more traditional to a loan officer.

Scaling with Confidence

Choosing a business structure is essentially a trade-off between simplicity and security. As your income grows, your legal setup should evolve from the simplicity of a sole proprietorship to the robust protection and tax efficiency offered by an LLC or S-Corp. By making these decisions before you reach critical financial milestones, you ensure your business is built to safeguard your personal life today while fueling your professional growth for tomorrow.

About the Author

Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity.

With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.