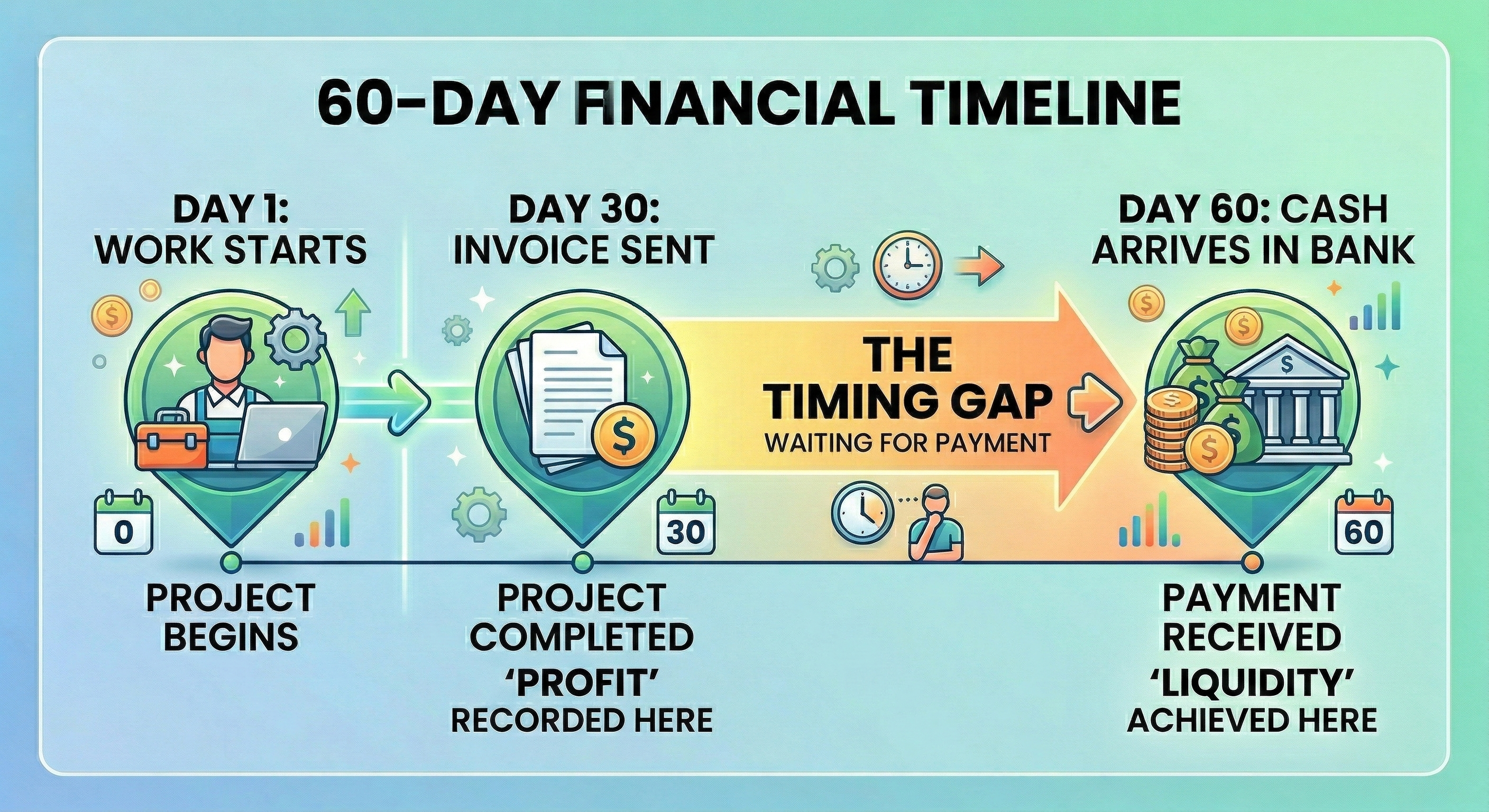

Imagine you have just finished a significant project. The client is pleased, and you have issued a professional invoice. On paper, your business is performing well.

Then you check your bank balance.

Your accounts receivable look strong. Your revenue is growing. But the actual cash available to pay software subscriptions, rent, or payroll is lower than expected — because that payment is still moving through a 30-day processing cycle.

This is one of the most common financial traps in growing businesses: strong revenue, weak liquidity.

A Cash Flow Projection exists to solve this problem.

It is not just a spreadsheet exercise. It is a forward-looking control system that shows you — weeks or months in advance — whether your business will have the liquidity to operate smoothly.

Profit is an accounting concept. Cash is a survival metric.

Many profitable businesses do not fail because they lack clients. They fail because they run out of cash before payments arrive.

In this article

- Distinguishing between paper profit and actual cash

- Managing the essentials of cash inflow and outflow

- Forecasting your monthly closing balance

- Implementation: Your cash flow projection template

- Financial health Q&A

- From Reactive Bookkeeping to Proactive Control

Distinguishing between paper profit and actual cash

It is a common misunderstanding to assume that a “profitable” month automatically means a healthy bank account.

You can be profitable — and still be unable to pay your bills on time.

Cash Flow is the real-time movement of money into and out of your accounts.

Profit is what remains after expenses are deducted from revenue — regardless of whether the money has physically arrived.

The difference is timing.

And in business, timing determines survival.

To operate with stability, you must prioritize Liquidity. This means having sufficient cash on hand to cover recurring costs like software, rent, and taxes precisely when they are due.

Managing the essentials of cash inflow and outflow

A reliable cash flow projection is built on two categories: inflows and outflows. By tracking these accurately, you move from reacting to your finances to controlling them.

Cash Inflow (The money entering your business)

Record inflows based on when you expect the money to be available, not when you finish the work.

Confirmed Payments: Only include revenue from signed contracts or completed milestones.

The Payment Buffer: A practical best practice is to forecast payments arriving seven days later than the client’s stated due date. This accounts for bank processing times and administrative delays.

Cash Outflow (The money leaving your business)

Modern business expenses are increasingly digital and recurring.

The Technology Stack: On average, professional freelancers and small agencies now spend 12–15% of their revenue on the software and tools required to stay competitive.

The Tax Reserve: One of the most vital professional habits is allocating 25–30% of every incoming payment into a dedicated tax account. By documenting this as a mandatory “outflow” in your cash flow projection, you ensure that quarterly tax deadlines never disrupt your operations.

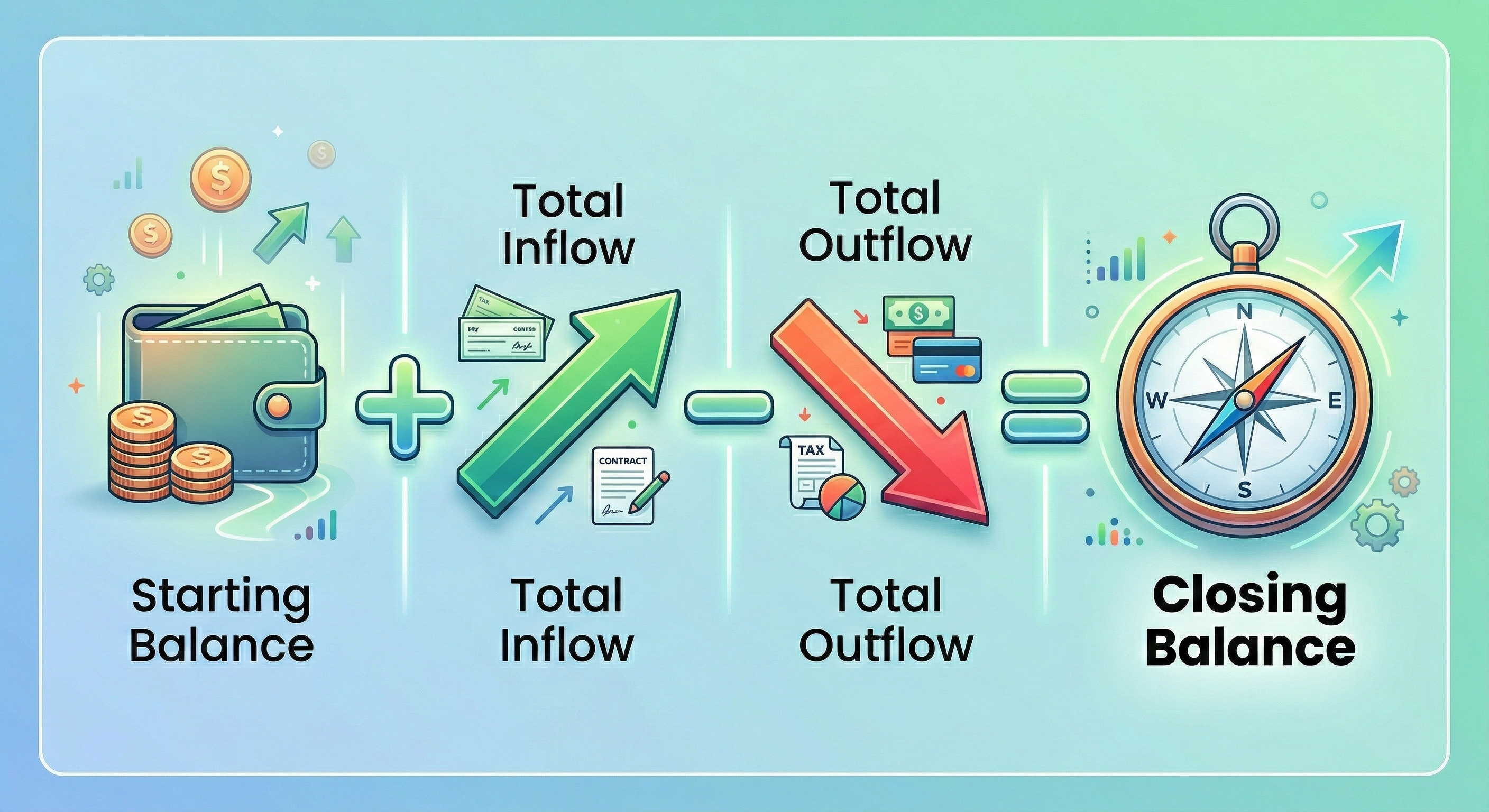

Forecasting your monthly closing balance

Once you understand your inflows and outflows, you can calculate your Closing Balance. This figure represents exactly how much cash you will have remaining at the end of the month.

Closing Balance= (Starting Balance+Total Inflow) − Total Outflow

A positive balance gives you flexibility to reinvest, build reserves, or absorb slow periods.

A negative balance is not a crisis. It is an early warning signal.

The purpose of a projection is not prediction; it is preparation.

Implementation: Your cash flow projection template

To help you move from theory to practice, we have provided a structured cash flow projection template below.

| Week | Starting Balance | Expected Inflow | Planned Outflow | Projected End Balance |

| Week 1 | $5,000 | $1,200 | ($800) | $5,400 |

| Week 2 | $5,400 | $0 | ($1,500) | $3,900 |

| Week 3 | $3,900 | $3,500 | ($400) | $7,000 |

| Week 4 | $7,000 | $500 | ($2,000) | $5,500 |

When you review this weekly, patterns begin to emerge:

- Are outflows clustered at the beginning of the month?

- Do large client payments consistently arrive late?

- Is your closing balance trending upward or compressing?

These patterns are where financial control begins.

Financial health Q&A

1. Should I include “potential” leads in my forecast?

No. To keep your projection accurate, only include projects where a contract is signed. Relying on a “potential” lead to cover fixed costs can lead to significant cash shortages.

2. How do I handle unpredictable monthly income?

Build your projection based on your “Financial Floor”—your guaranteed retainers or your lowest historical monthly earnings. Anything earned beyond that is a bonus, but your essential bills should be covered by your most conservative estimate.

3. What if my projected balance turns negative?

First, do not panic; the entire purpose of a projection is to give you time to adjust before the situation becomes an actual problem.

Review variable costs such as marketing campaigns, new equipment, or discretionary spending. These can often be deferred. At the same time, use the projection as a prompt to follow up on overdue invoices to accelerate inflow.

The earlier you see the dip, the more options you have.

4. How do I know if my business is “safe”?

Aim to maintain a “Cash Floor” that can cover at least three months of your total outflows. Running out of cash is one of the top 5 reasons small businesses fail. This provides the security to navigate project delays or seasonal dips in work without compromising your operations.

5. What hidden outflows should I watch for?

Commonly missed expenses include:

- Annual software renewals

- Domain and hosting fees

- Professional memberships

- Hardware replacements

- Transaction processing fees

Always forecast based on net cash received, not the gross amount invoiced.

From Reactive Bookkeeping to Proactive Control

Taking control of your cash flow is the most effective way to eliminate the “financial fog” that often leads to burnout. Projections move you away from the stress of wondering if a client payment will arrive in time to cover rent, allowing you to focus on the work that actually grows the business.

Resilience isn’t built by hoping for a good month; it is built by seeing a potential dip sixty days out and having the clarity to adjust your spending or follow up on invoices before it becomes a crisis. When you master your cash flow, you stop being a passenger in your business and start being the pilot.

About the Author

Isabella Jones started her career at Deloitte, where she managed tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity.

With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.