If you’ve successfully scaled your business past the six-figure mark, you’ve reached a significant milestone. Yet, as your revenue grows, the business structure that served you as a lean startup may no longer be the most efficient vehicle for your success.

In 2026, many high-performing founders are discovering that staying in their “default” setup is a choice that costs them thousands of dollars in unnecessary tax leakage every single year.

Most freelancers stay in a basic LLC because it’s easy. While simplicity has its merits in the beginning, relying on it indefinitely often leads to a massive missed opportunity for wealth building. In a six-figure business, that “simplicity” isn’t free—it represents capital that could be better spent on a strategic new hire, upgrading your technology stack, or funding your retirement.

In this article

- Understanding the Self-Employment Tax Threshold

- Business Structure Comparison Between LLC vs S-Corp vs C-Corp

- Finding the Salary Sweet Spot for Maximum Savings

- Maximizing the 20% Qualified Business Income Deduction

- Protecting Your Assets by Maintaining the Corporate Veil

- Implementation Checklist & Deadlines

- Moving Toward an Optimized Structure

Understanding the Self-Employment Tax Threshold

To understand how to save money, we first have to look at how the IRS views a standard LLC. In the eyes of the tax man, you and your LLC are a “disregarded entity”—meaning you are essentially the same person. This results in 100% of your net profit being hit with a 15.3% self-employment tax to cover Social Security and Medicare.

As you scale, this math becomes painful.

- At $50,000 profit: You pay ~$7,650 in self-employment tax.

- At $150,000 profit: That bill climbs to over $21,000.

By electing S-Corp status, you fundamentally change the relationship between you and your money. You become an employee of your own business, allowing you to pay yourself a “reasonable salary” (which is taxed) while taking the remaining profit as a distribution. These distributions are exempt from that 15.3% tax, which is exactly where the five-figure savings come from.

Business Structure Comparison Between LLC vs S-Corp vs C-Corp

Selecting a structure is more than just tax optimization; it is about ensuring your legal framework aligns with your long-term strategic vision.

While the S-Corp is often the ideal choice for service-based founders, the C-Corp (or “Inc.”) remains the gold standard for those intending to scale globally or raise outside capital. In fact, approximately 95% of venture capital is directed toward C-Corps because they support the unlimited shareholders and complex stock classes that institutional investors demand.

| Feature | Standard LLC | S-Corp Election | C-Corp (Inc.) |

| Tax Filing | Personal 1040 (Schedule C) | 1120-S + K-1 | Form 1120 (Corporate) |

| Payroll Requirement | None | Mandatory W-2 salary | Mandatory for active owners |

| Self-Employment Tax | 15.3% on 100% of profit | 15.3% on salary only | None (on dividends) |

| Management Style | Flexible; Member-managed; no board required | Formal; Requires Board of Directors and Officers | Strict; Board oversight with mandatory annual minutes |

| Audit Risk | Higher; Schedule C filings often draw IRS scrutiny | Lower; Formal structure and payroll reduce “red flags” | Moderate; Professional compliance is expected |

| Primary Benefit | Maximum simplicity | Tax savings for $100k+ earners | Scalability & VC funding |

| Primary Drawback | High tax as revenue scales | Compliance & payroll costs | Potential double taxation |

Finding the Salary Sweet Spot for Maximum Savings

The biggest “catch” with an S-Corp is that you must pay yourself a “reasonable salary”. If you pay yourself $0 to avoid all taxes, the IRS will audit you; if you pay yourself your entire profit, the S-Corp becomes a useless expense. We generally look at three tiers of profit to find that “sweet spot”:

- Under $60,000 Profit: Stay as an LLC. The cost of running payroll and filing separate business returns (which can cost several thousand dollars) will eat up any small tax savings.

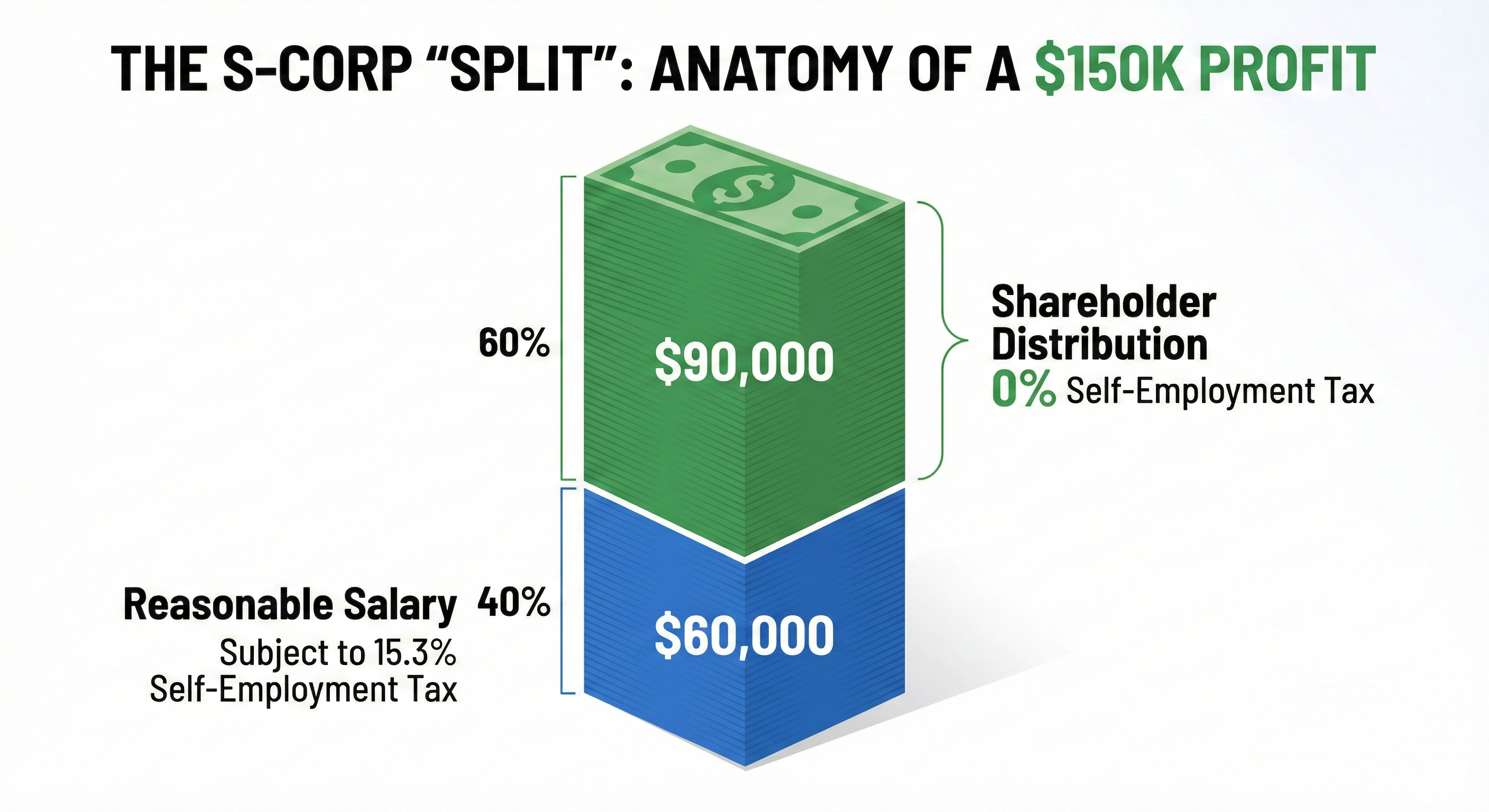

- The $80,000 – $150,000 Range: This is the prime transition zone. For instance, at a $150,000 net profit, paying yourself a $60,000 salary while taking the remaining $90,000 as a distribution can save you roughly $10,000 to $12,000 annually compared to a standard LLC.

- $250,000+ High Earners: At this level, you must account for the Social Security Wage Base cap (estimated at $176,100 for 2026). Once your salary hits this cap, you only pay the 2.9% Medicare tax, which changes your strategy for how much you should pull out as a W-2 wage.

Maximizing the 20% Qualified Business Income Deduction

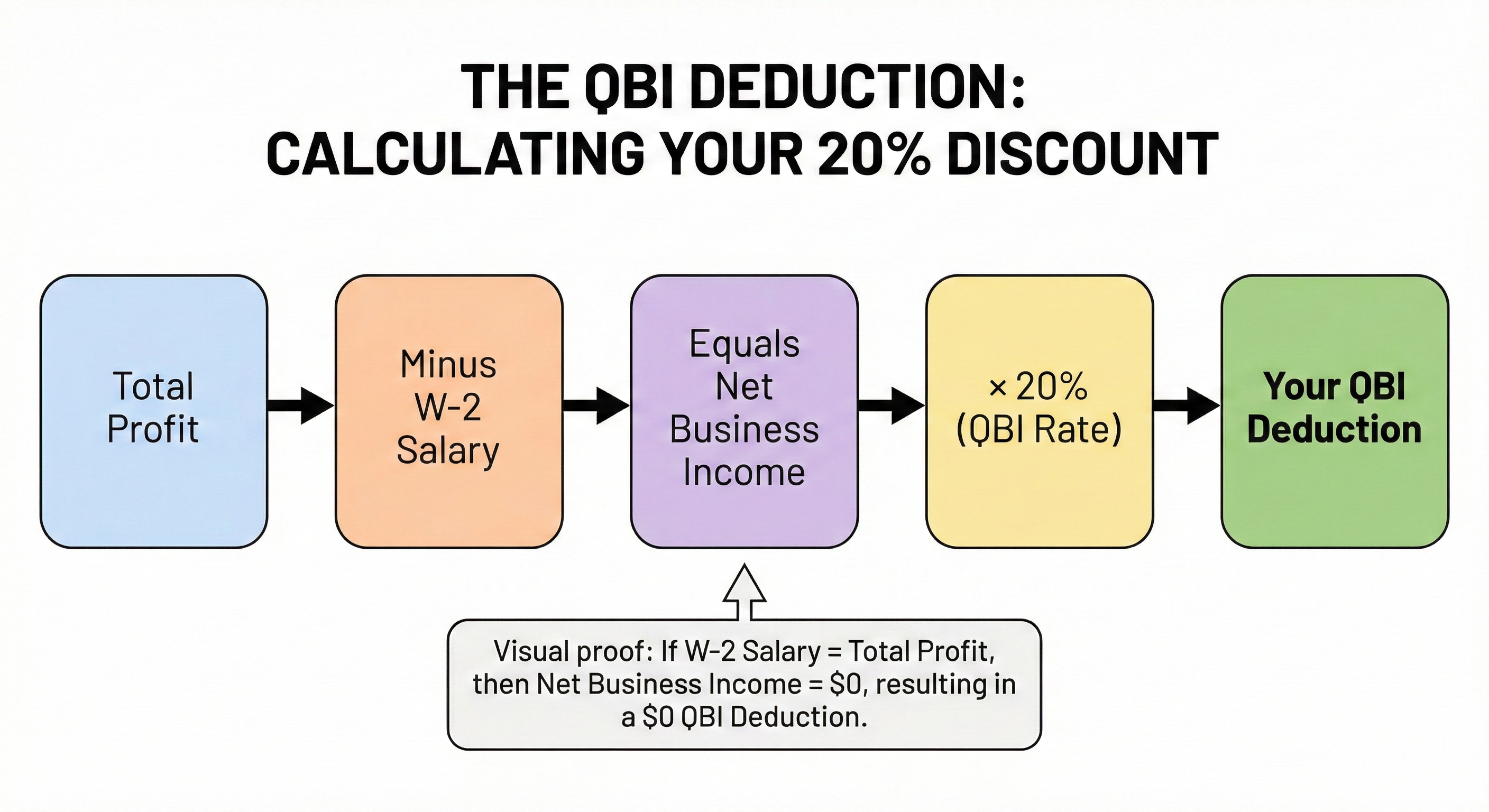

The Qualified Business Income (QBI) deduction allows many business owners to deduct up to 20% of their business income from their taxes. For S-Corp owners, this deduction is calculated on your profit after your salary is paid.

While powerful, the 20% Qualified Business Income (QBI) deduction is subject to limits once your total taxable income rises above the annual thresholds (for example, around $203,000 for single filers and $406,000 for married filing jointly, indexed for inflation). Above these levels, the deduction is gradually restricted based on the type of business you operate and how much you pay in W-2 wages or own in qualified business property.

For specified service businesses (such as consulting, legal, medical, and similar fields), the deduction phases out completely as income increases. For other businesses, the deduction can still apply but is capped using wage and property formulas. The key planning strategy is to set a salary that meets IRS “reasonable compensation” rules without unnecessarily reducing the pool of business profit that may qualify for the 20% QBI deduction.

Protecting Your Assets by Maintaining the Corporate Veil

Both LLCs and Corporations offer a layer of protection for your personal assets, shielding them from business debts and lawsuits. However, this protection depends on maintaining a clear separation between personal and business activity.

- The Corporate Veil: If you “co-mingle” funds (e.g., using your business account for personal expenses), a court may “pierce the corporate veil,” making you personally liable for business debts.

- Compliance Standards: LLCs offer more flexibility. S-Corps and C-Corps must adhere to stricter formalities, such as adopting bylaws, holding annual meetings, and maintaining detailed minutes. Neglecting these requirements can weaken your legal protection.

- Audit Profile: An S-Corp must run payroll and maintain clean financial statements. This level of structure often reduces “red flags” common with loosely tracked Schedule C filings.

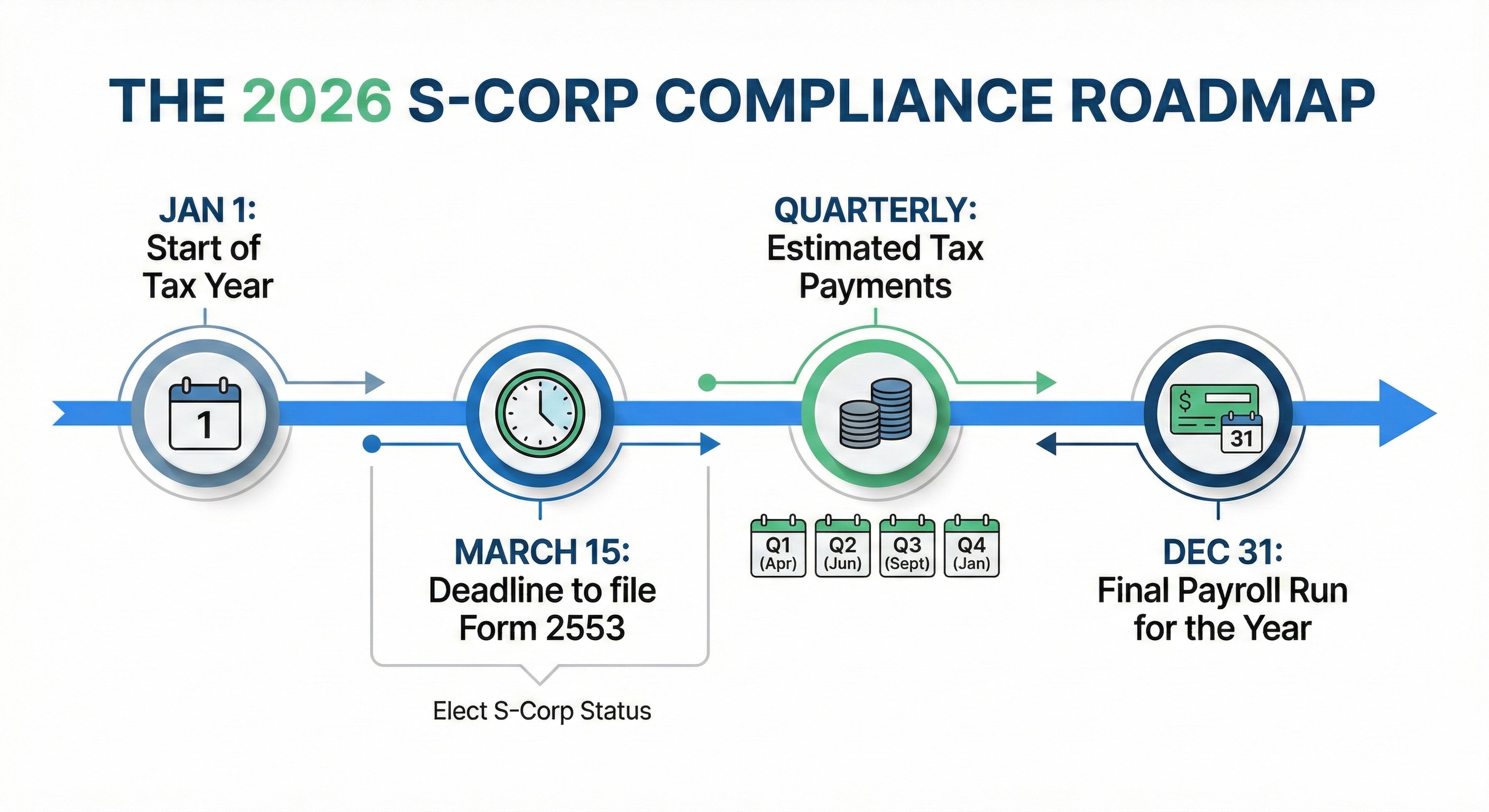

Implementation Checklist & Deadlines

Transitioning to an S-Corp requires discipline in your accounting and adherence to strict IRS timelines.

1. The March 15th Deadline

To be taxed as an S-Corp for the 2026 calendar year, you must file IRS Form 2553 by March 15, 2026. If you miss this date, your election typically won’t take effect until the following tax year, though “Late Election Relief” is sometimes available for businesses with a valid reason for the delay.

2. Formalize Your Bookkeeping

Because the S-Corp is a separate tax entity, “co-mingling” funds (using business money for personal groceries) is a significant compliance risk. You must maintain pristine records and clear separation between business and personal accounts.

3. Set Up Monthly Payroll

You cannot simply “take money out” as an S-Corp owner. You must use a payroll provider (like Gusto or Rippling) to withhold taxes from your salary and issue yourself a W-2 at the end of the year.

Moving Toward an Optimized Structure

The move from a standard LLC to an S-Corp is a sign of business maturity. It shifts your focus from simply maintaining operations to strategically optimizing for wealth. If your business is consistently netting over $100,000, continuing as a basic LLC is no longer a matter of simplicity—it’s a matter of unnecessary expense.

About the Author

Isabella Jones started her career at Deloitte, where she worked on tax compliance for some of the country’s fastest-growing companies. She later joined Fynlo as Senior Financial Strategist, bringing that experience to freelancers and small business owners who need practical financial guidance without the corporate complexity.

With an Accounting degree from Villanova University, Isabella focuses on making financial planning easier to understand and apply in day-to-day business. She works closely with freelancers and small businesses on areas like taxes, cash flow, and building more stable financial systems.